What a year 2021 has been. We started the year with many pundits saying that the U.S. economic recovery was a false story and that we were about to embark on a second housing bubble crash due to forbearance. However, not only did the U.S. economy continue to recover from the lows of April of 2020, but the 2021 economic data shows it has been one of the hottest years in many decades.

Retail sales have been off the charts, job openings are at 11 million, GDP growth picked up big time and jobless claims hit a level last seen in 1969. The housing market didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020.

The housing crash addicts in America have now been wrong for a decade. After failing from 2012-2019, they went all in during 2020 due to COVID-19, only to move the goalpost to 2021 due to forbearance. That didn’t end well for them. Now that we are just a few days away from 2022, it’s time to take a look at the positive and the negative housing stories of 2021.

The good

Keeping it simple, mother demographics is the most powerful economic force in the world. I’ve been writing for many years that years 2020-2024 would have the best housing demographics ever recorded in history. During this timeframe we have a historic one-time bump in ages 28-34 — the peak age for home buying. In fact, the reason the housing bears have such terrible track records is because they look at housing as an investment first, not the cost of shelter to a person’s capacity to own the debt. First and foremost, Americans are buying a place to live, not an investment.

With only one existing home sales report left this year, it is imperative to focus on the fact that more Americans bought homes in 2021 than 2020. These households got sub-3.5% mortgage rates, so on the mortgage rate side of the equation, it’s never been better. Also, post-2010, the loans in American are very vanilla on the debt structure side of the equation.

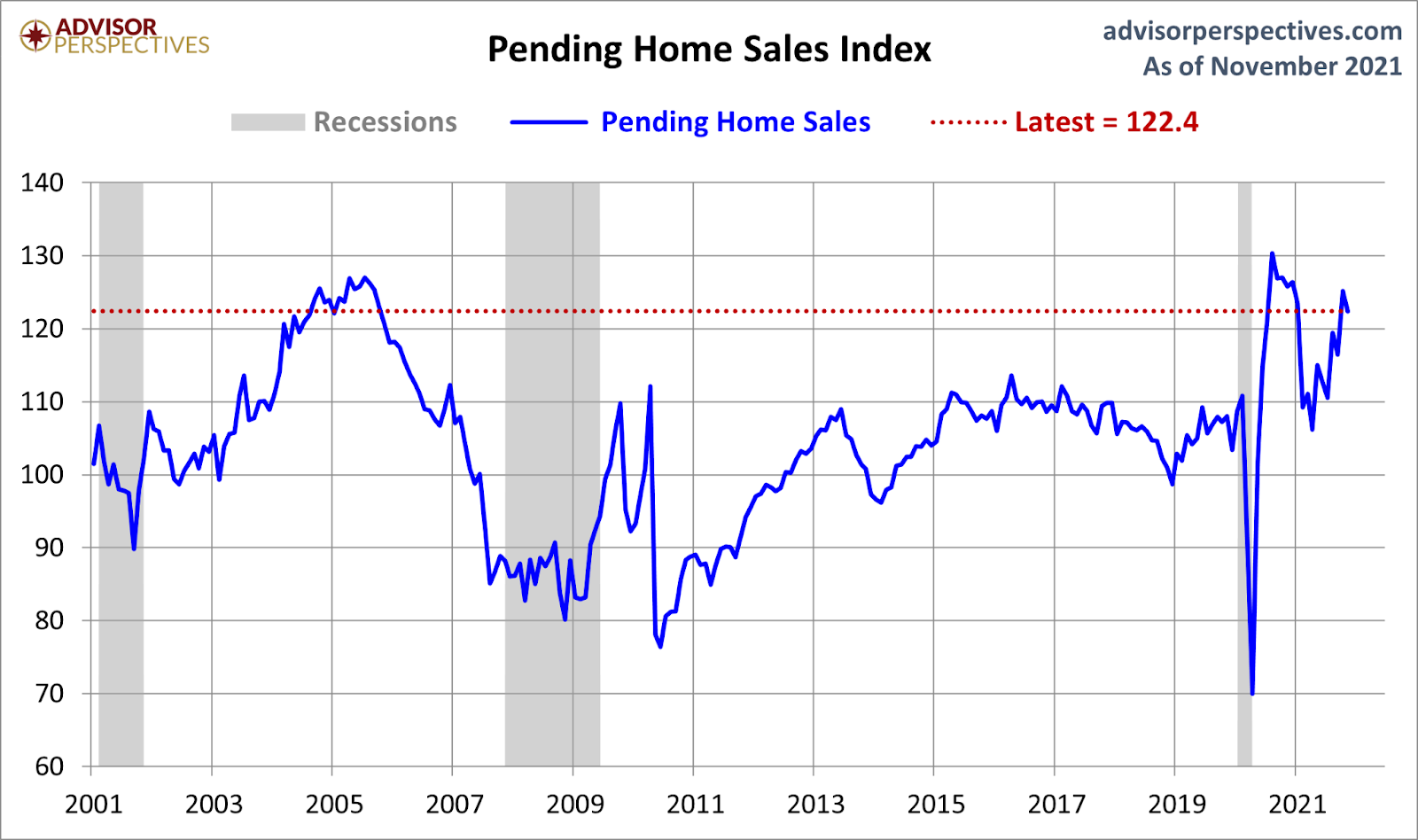

Housing demand itself is slightly outperforming what I would have expected in 2021 as existing home sales have had a few prints over 6.2 million toward the end of the year. Today, NAR‘s pending home sales report came out showing a slight decline, but the trend here is also better than what I thought it would be toward the end of the year.

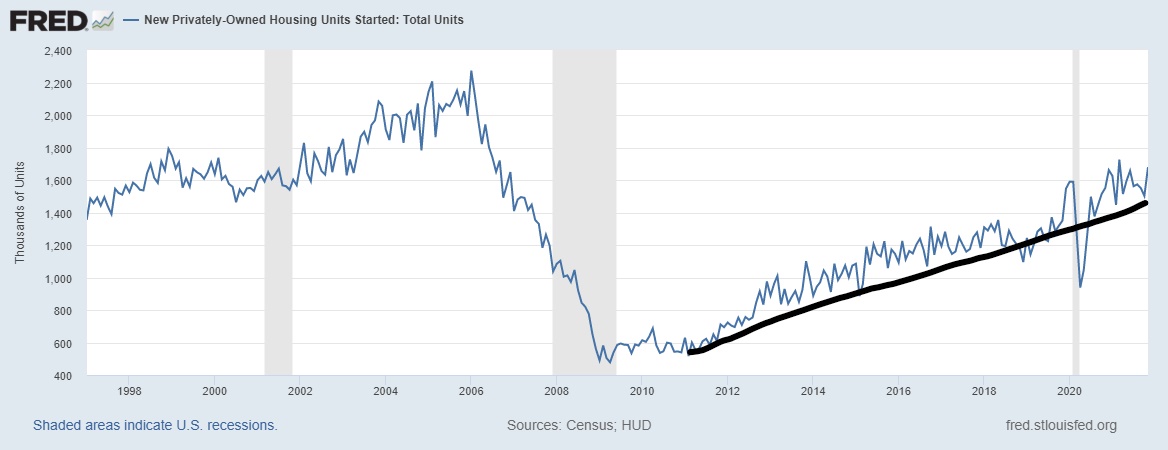

Housing permits are growing and this is a good thing for the economy and construction jobs. While I have never been a housing construction boom guy because mature economies typically don’t have a construction boom, the fact that permits are keeping their uptrend is a big positive for the United States of America.

We do have some very positive stories about the housing market in 2021, but not all is perfect, of course.

The bad

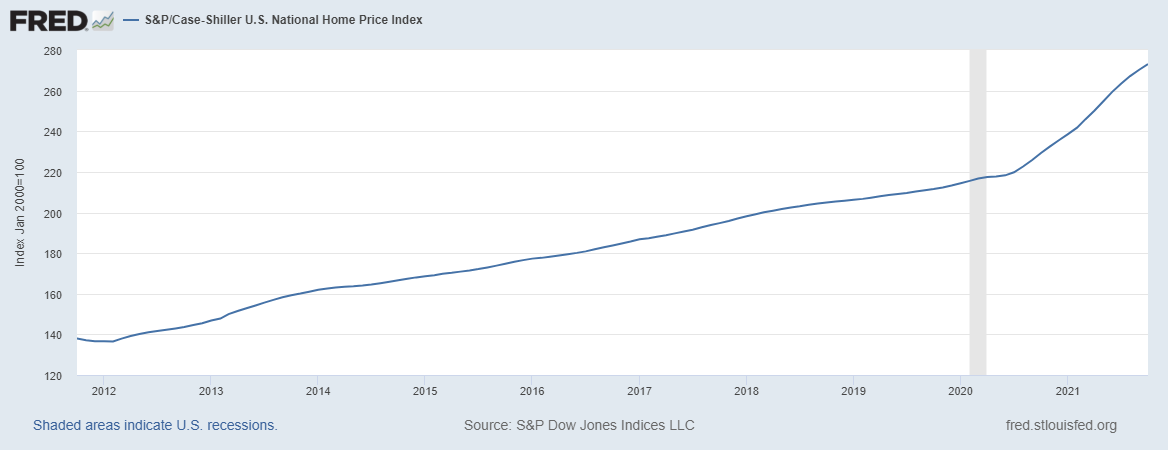

My economic models over the years showing that housing demographics would be better in the years 2020-2024 have also led me to be mindful of home-price growth taking off. Currently, home-price growth is too hot, which is why I label this the unhealthiest housing market post-2010. According to the parameters I set for this period, as long as nominal home-price growth was only 23% or less during this unique five years, then it would be manageable considering the demographic backdrop and low mortgage rates. Well, it looks like my five-year growth model has been taken out in two years.

Not the best of news as we start year three of that time period with a solid possibility of new all-time lows in inventory this spring.

While I do believe the rate of home-price growth is cooling off — since data from the S&P CoreLogic Case Shiller Home Price Index lags — the market is still seeing home-price growth above my five-year price model, so wishing for less price growth in 2022 is a must for me. Simply put, the days on market are still too low, which creates unhealthy price growth, too much bidding action for homes, and a lot of stress in the home-buying process.

Another aspect that doesn’t get enough attention because it’s a hard look in the mirror: We all get greedy when we have pricing power — it’s the nature of the beast. Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers. Since housing is a shelter cost — everyone needs a home to live in — it’s much different than buying a stock. As we can see below, the builders are maximizing their pricing power. Even with all the labor and material costs they have had to deal with since the pandemic started, they had a stellar year with their profit margins.

Yes, the housing market has done well during 2020 and 2021, but it has come at a price and with rental inflation kicking into another gear, the cost of shelter rising is a theme for 2022.

The excellent

Wait, isn’t it “The Good, the Bad and the Ugly?” Not in my western 2021 world! We write history on our own terms and we do have some excellent news.

Going into 2021, the big question mark was what would happen with forbearance. Now, for me, it wasn’t such a big question mark. I was so confident that forbearance wasn’t going to be the doomsday event that many American and housing bears were rooting for during this pandemic that I coined the term forbearance crash bros in the summer of 2020. This was in honor of all the trolling, non-economic people on the internet calling for housing to crash when clearly none of these people had any clue about the housing market or the credit debt structures of homeowners post-2010. I documented my work with many articles, which can be found here.

Forbearance went from near 5 million at the start of the crisis to under 882,000 today, with many more Americans getting off this program. What an excellent data line to have in 2021: the housing data that collapsed wasn’t housing demand or prices but forbearance itself!

The Freddie Mac and Fannie Mae forbearance delinquency percentage is about to break under 0.50%, yes 0.50%. It was truly one of the more successful government programs because all these homeowners were legit and they had the capacity to own the debt before COVID-19 and after. Beyond the success of just the forbearance program is the state of the American homeowner today. A big part of my work is based on the principle that homeowners now have a fixed low long-term debt cost as their wages rise every year. What this means is that their cash flow gets better each year.

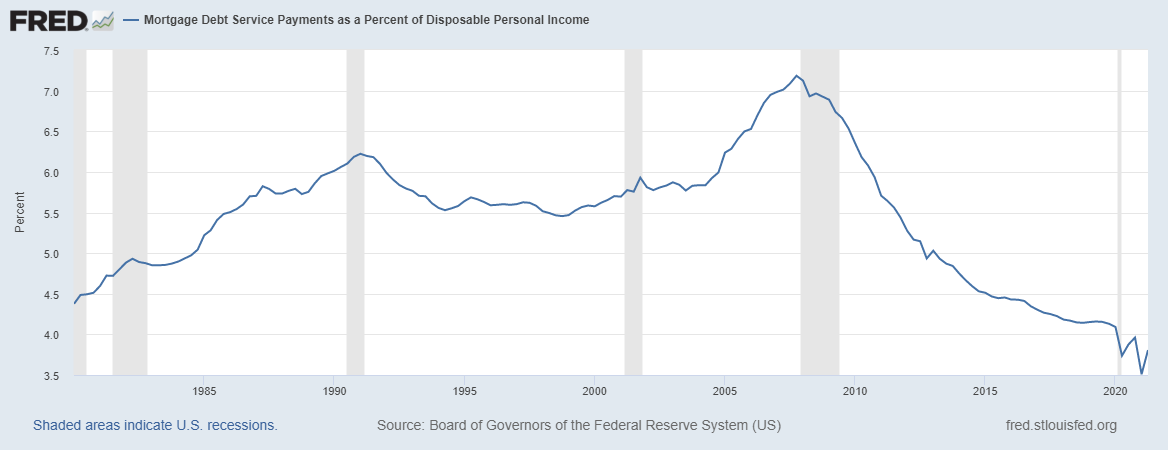

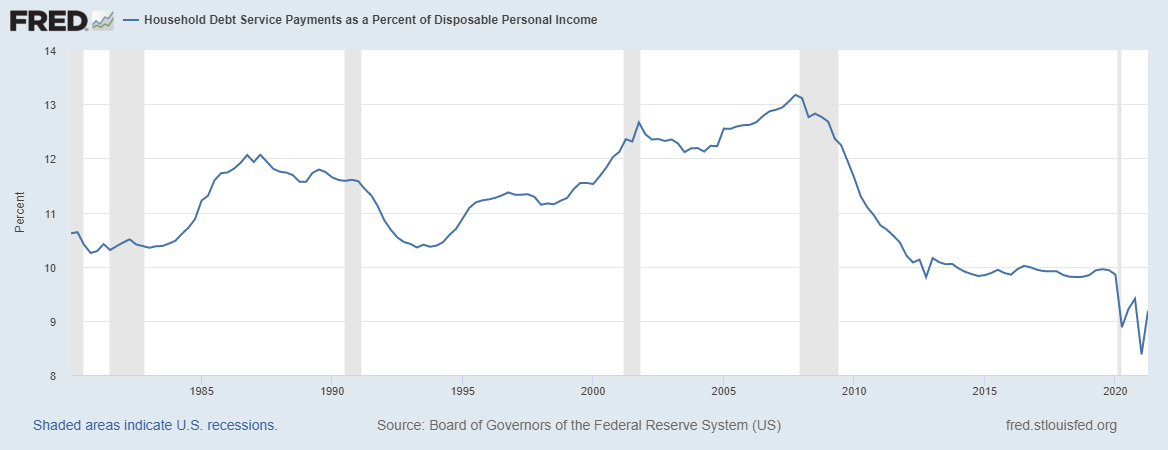

On top of all of that, many Americans refinanced their homes, which made them look even better on paper. Mortgage debt service payments as a percent of disposable personal income are near all-time lows.

Since mortgage debt is the biggest consumer debt we have in America, household debt payments look just as good.

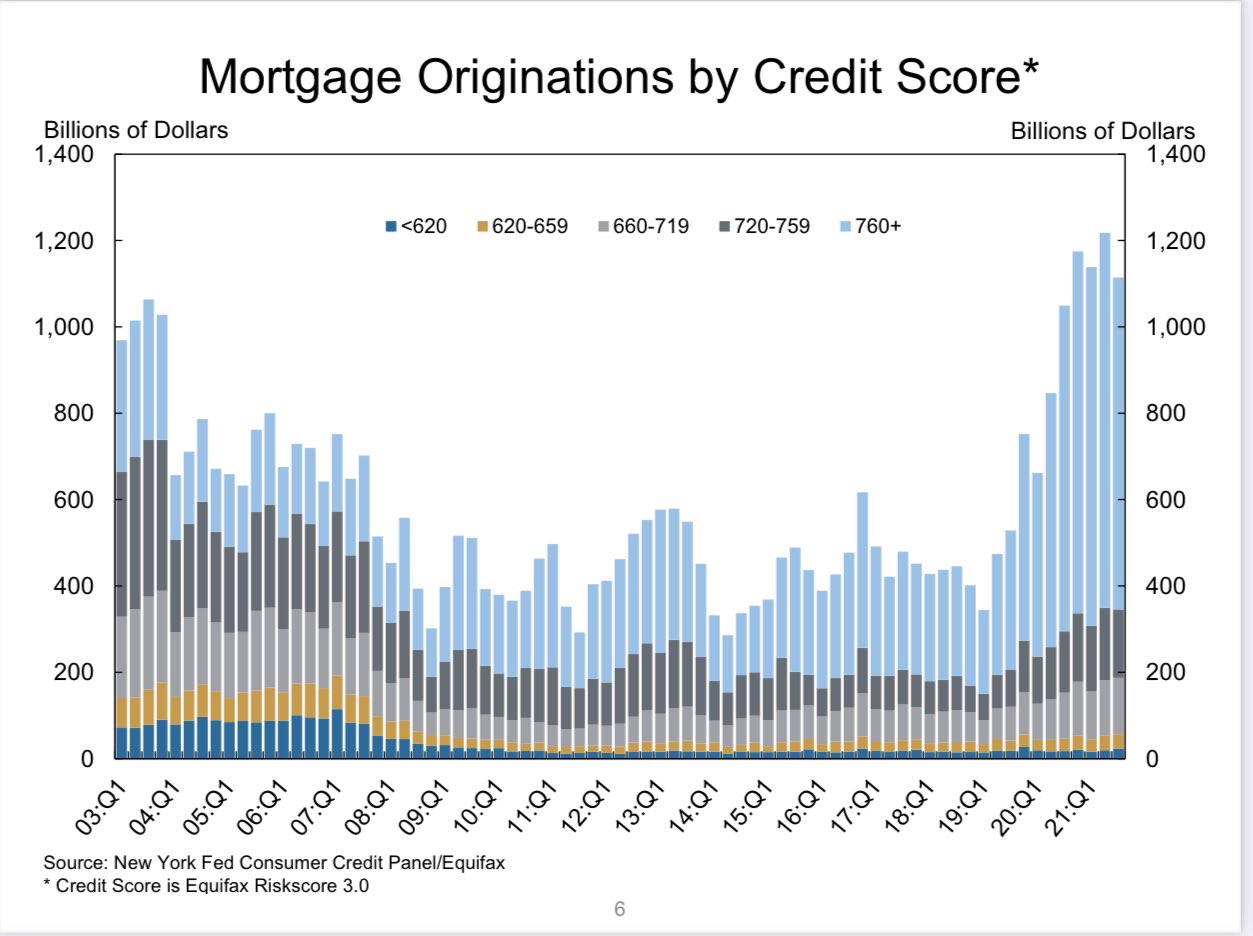

This has led to much better cash flow, so FICO scores have exploded higher and the best part of this all is that we have no exotic loan debt structures in the system. This means all homeowners are legit and those who are cashing out on their homes are all good as well.

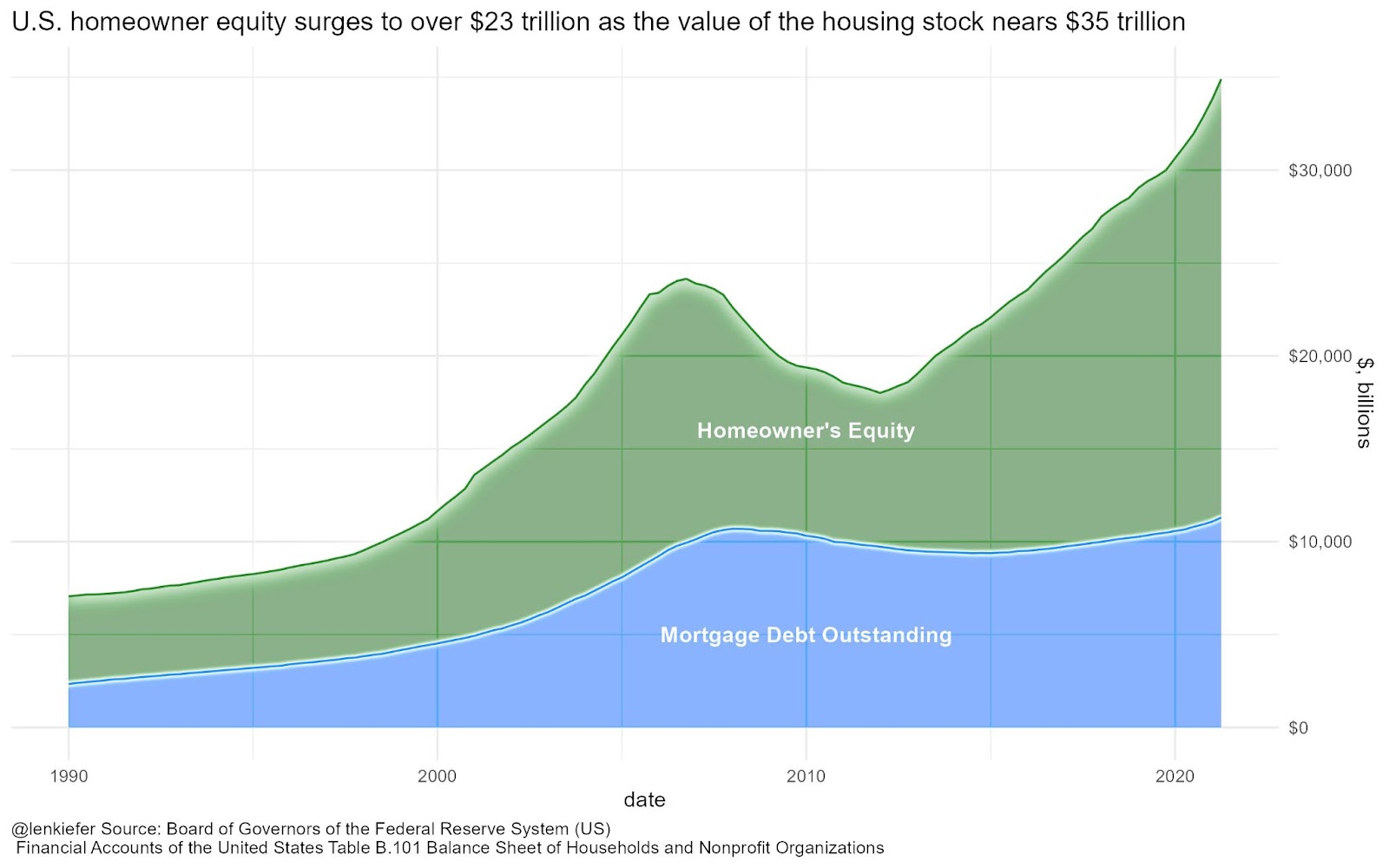

On top of all that, the nested equity position of American homeowners has never looked better.

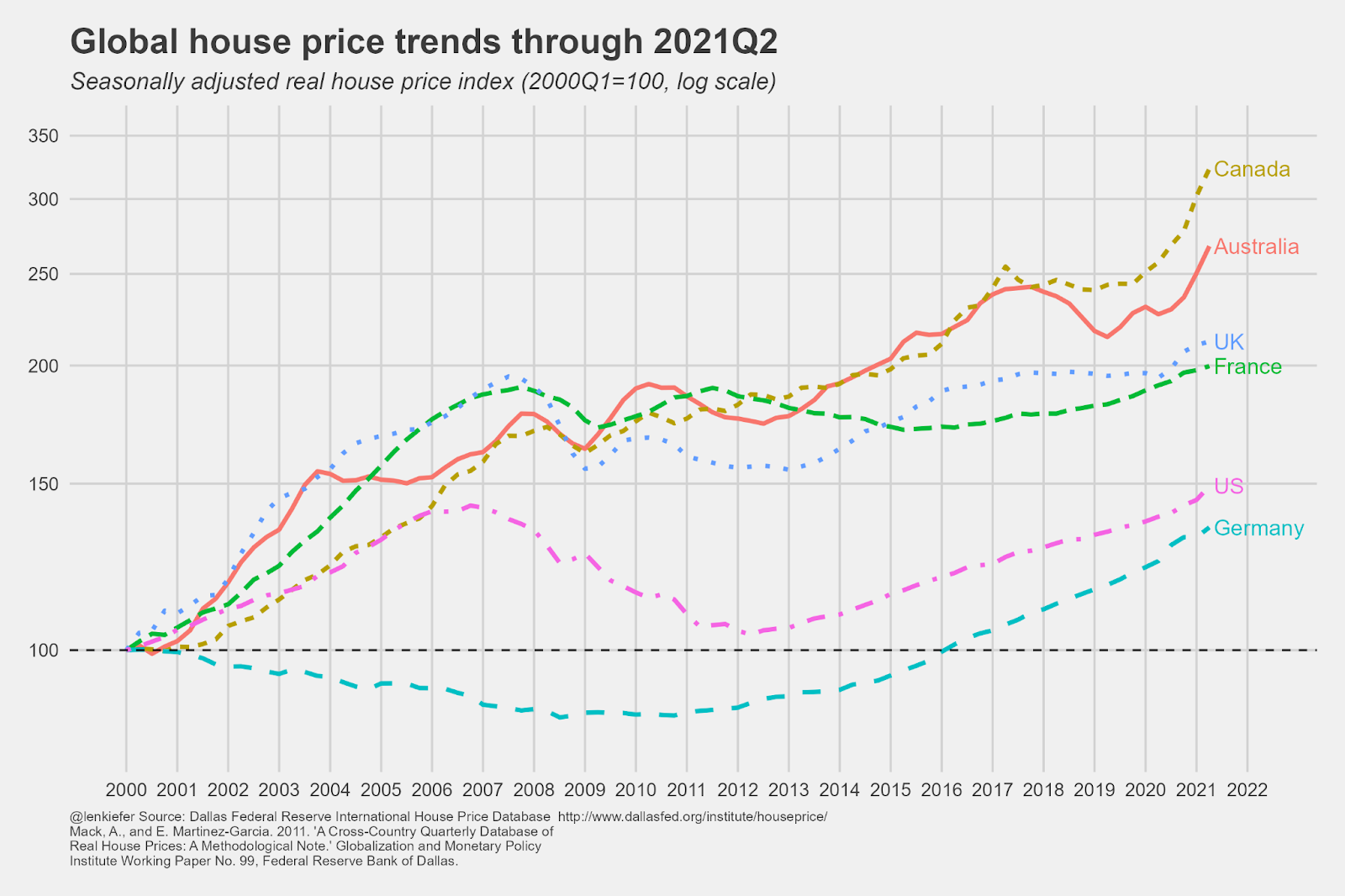

Two of my favorite charts from Freddie Mac Chief Economist Len Kiefer also show the public how home-price growth in the U.S. has not been as hot as in other countries, but the nested equity position is so much better now than the peak of the housing bubble years. This is a critical fact to remember: when adjusting to inflation, mortgage debt expansion is still negative compared to the peak of the housing bubble years. Since housing tenure is now over 11 years, the built-in equity position is much higher today without a massive credit boom like what we saw from 2002-2005. In short, we made American mortgage debt great again!

Credit and debt profiles are so critical to our economy and it was great to see how it all paid off during this crisis and how it can shape the future as well.

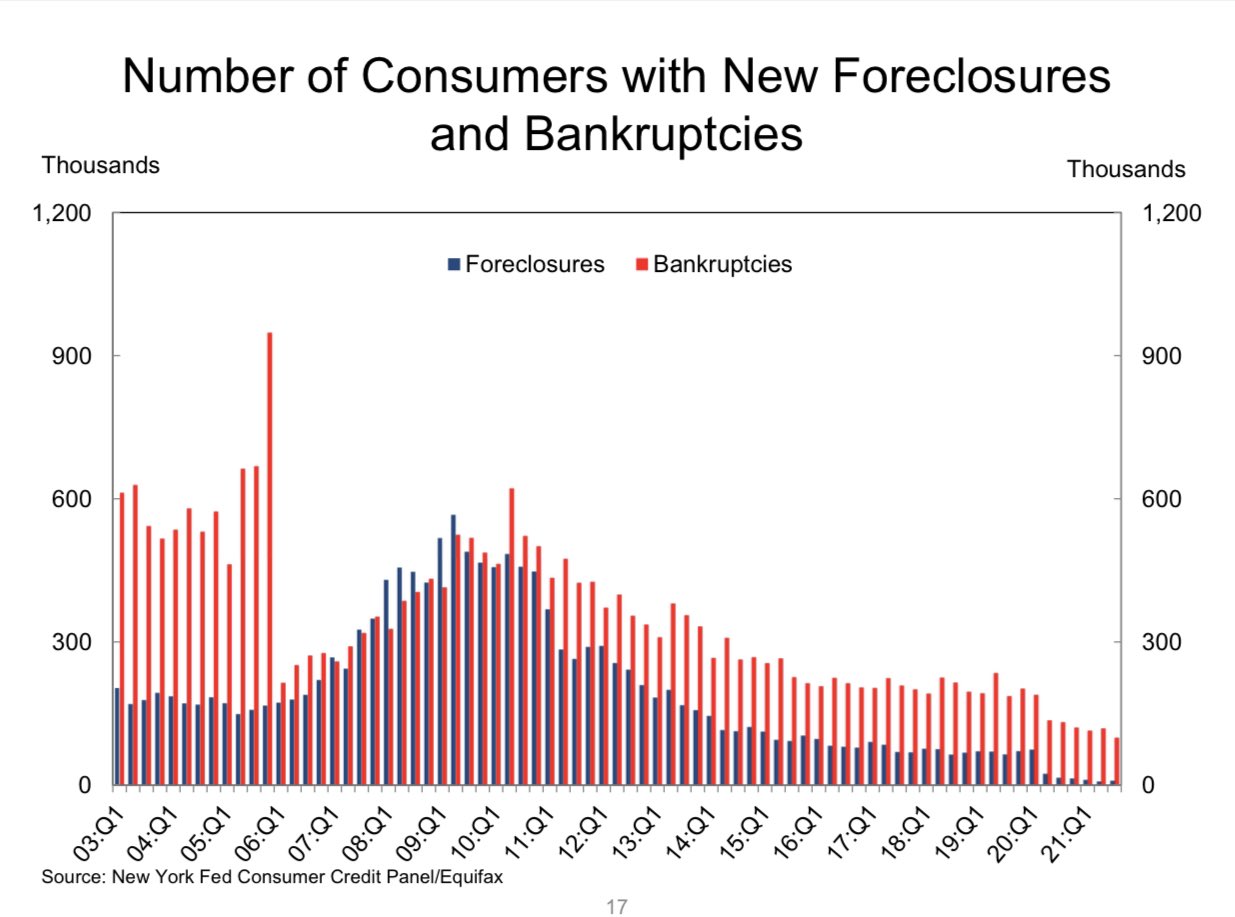

All in all, 2021 was a good year for the housing market. Nothing can be perfect, of course, but we would rather be working from pre-cycle highs in demand, falling forbearance data, and an expanding economy versus what we saw from 2005-2011 where home sales were falling, prices were falling, people had negative equity, and bankruptcies and foreclosures were rising.

In fact, our issues today are first-world problems compared to the past. Sometimes we need to take a long look at where we came from to where we are today and appreciate that the United States of America and its people just had the greatest economic recovery ever, which very few saw coming. Now it’s time to move on to 2022 and what’s in store for the year ahead. Read my 2022 housing and economic forecast here and rest assured: we will get through 2022 one data line at a time.