Citing the extraordinary circumstances that the country is facing with the ongoing spread of the coronavirus, the Federal Housing Finance Agency announced Monday that it is directing Fannie Mae and Freddie Mac to ease their standards for both property appraisals and verification of employment.

The moves are part of a growing effort to “facilitate liquidity in the mortgage market during the coronavirus national emergency,” the FHFA said in an announcement.

According to the FHFA, Fannie Mae and Freddie Mac will use “appraisal alternatives to reduce the need for appraisers to inspect the interior of a home for eligible mortgages.” The issue of appraisers needing to inspect homes as part of the mortgage process has been a mounting concern as the virus has continued to spread throughout the nation.

Considering that new research shows that the virus can live for “several hours to days in aerosols and on surfaces,” appraisers entering homes to inspect may lead to increased spread of the virus. Beyond that, cities and even entire states are going into lockdowns, thereby prohibiting appraisers from traveling to houses to inspect them.

As a result, the FHFA has directed the GSEs to begin using both drive-by appraisals and desktop appraisals in certain circumstances to ensure that the mortgage process is not held up due to appraisal issues. “Effective immediately, we are allowing temporary flexibilities to our appraisal inspection and reporting requirements,” Fannie Mae said in an announcement sent to lenders Monday morning.

“We will accept an alternative to the traditional appraisal required under Selling Guide Chapter B4-1, Appraisal Requirements, when an interior inspection is not feasible because of COVID-19 concerns,” Fannie Mae continued. “We will allow either a desktop appraisal or an exterior-only inspection appraisal in lieu of the interior and exterior inspection appraisal (i.e., traditional appraisal).”

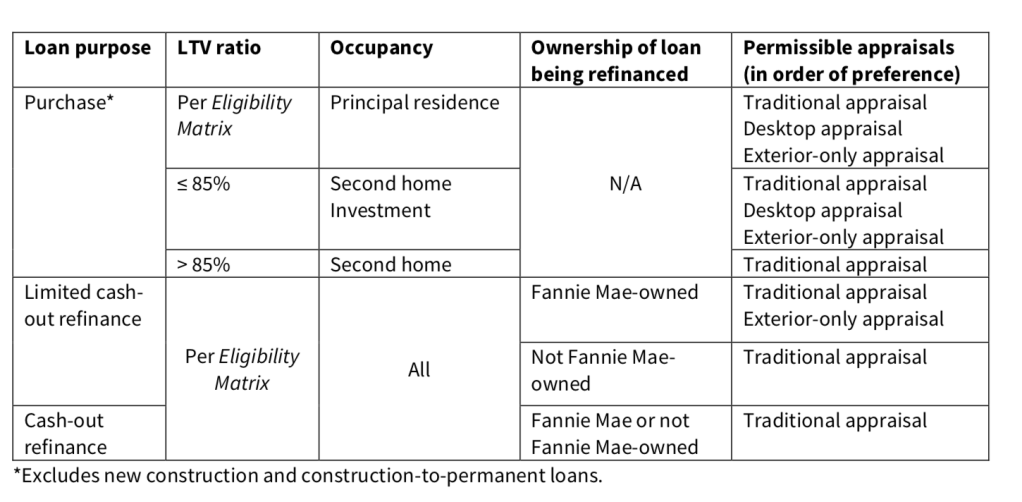

It should be noted that the change to the GSEs’ appraisal policies mostly affects purchase mortgages. For a more detailed breakdown of the policies, click here.

According to the bulletin, the preferred appraisal method is still the traditional appraisal. If that is not available, the GSEs prefer a desktop appraisal, where the appraiser doesn’t inspect the property or comparable sales. Instead, the appraiser relies on public records, multiple listing service information, and other third-party data sources to identify the property characteristics.

If a traditional or desktop appraisal is unable to be performed, an exterior-only inspection is allowed in certain circumstances. In all cases, the use of appraisal alternatives is available only on certain loans. See the graphic below for details on what loans are eligible for an appraisal alternative.

Beyond that, the FHFA notes that employment verification is becoming increasingly more difficult as many businesses have either shut down entirely or are running with skeleton crews as a result of the virus. To that end, the GSEs will accept alternative forms of employment verification, including a recent paystub, to ensure lending can continue.

Specifically, the FHFA states that “in the event lenders cannot obtain verbal verification of the borrower’s employment before loan closing, the Enterprises will allow lenders to obtain verification via an e-mail from the employer, a recent year-to-date paystub from the borrower, or a bank statement showing a recent payroll deposit.”

And here, from Fannie Mae’s bulletin, is more detail on how each of those forms of verification of employment will work:

- Written VOE: The Selling Guide permits the lender to obtain a written VOE confirming the borrower’s current employment status within the same timeframe as the verbal VOE requirements. An email directly from the employer’s work email address that identifies the name and title of the verifier and the borrower’s name and current employment status may be used in lieu of a verbal VOE. In addition, the lender may obtain the VOE after loan closing, up to the time of loan delivery (though we strongly encourage getting the verbal VOE before the note date).

- Paystub: The lender may obtain a year-to-date paystub from the pay period that immediately precedes the note date.

- Bank statements: The lender can provide bank statements (or other alternative documentation as permitted by Selling Guide B3-4.2-01) evidencing the payroll deposit from the pay period that immediately precedes the note date.

The FHFA notes that lenders should “continue to utilize sound underwriting judgment to ensure these alternatives are appropriate to the borrower’s circumstances.”

Both the adjusted appraisal and employment verification standards are in effect through May 17, 2020, according to the FHFA.

For more information on the appraisal alternatives, click here.

And for more information on the employment verification alternatives, click here.

[Update: This article is updated to reflect the timeline for the appraisal and employment verification standards.]