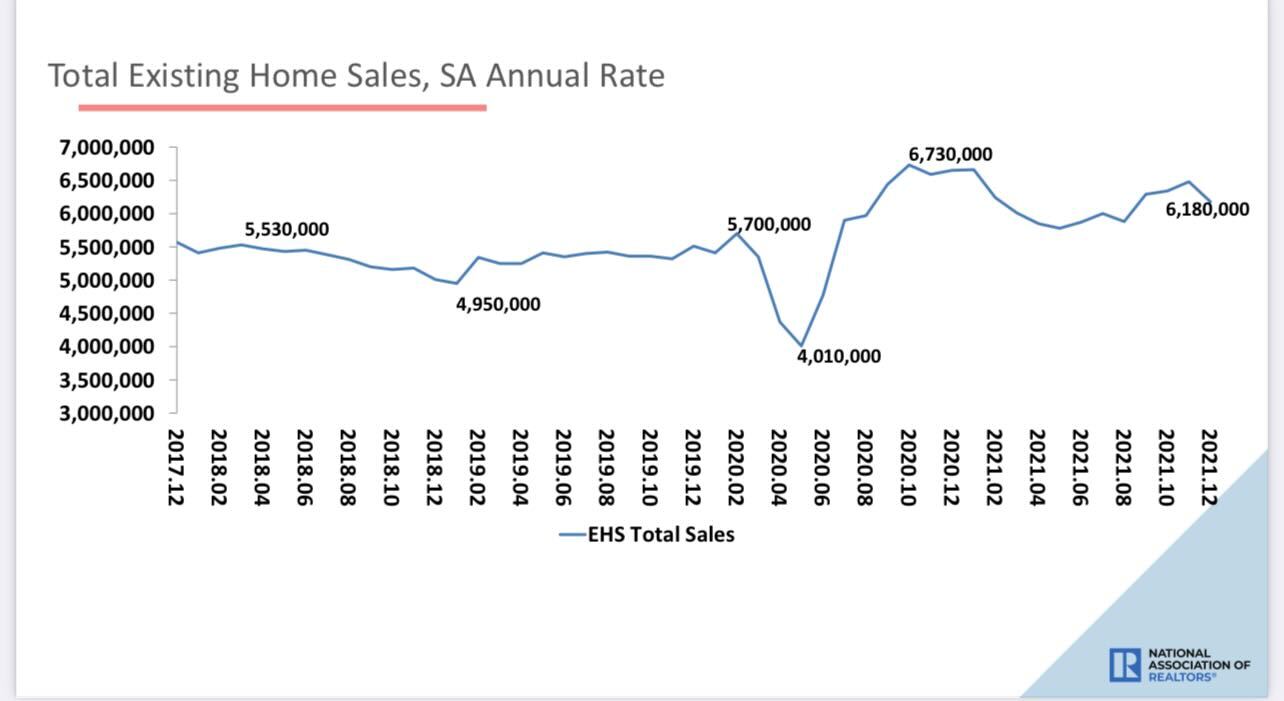

The National Association of Realtors reported that existing home sales for December came in as a miss of estimates at 6.18 million. This number is in line with my sales range for 2021 of 5.84 million to 6.2 million, but a tad higher than my existing home sales range for 2022, which is between 5.74 million and 6.16 million.

From NAR:

In the last few months of the year, existing home sales have been outperforming my sales ranges noticeably, and I talked about how sales could moderate, but mortgage demand ended 2021 on a solid note.

As I have stressed for many years, years 2020-2024 would differ from what we saw from 2008-2019 due to demographics. More Americans bought homes in 2020 and 2021 than any single year from 2008 to 2019, which looks normal. I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. However, total home sales — new and existing — during 2020-2024 should be 6.2 million and higher, and so far, two out of five years have checked that box. This is something that couldn’t have happened from 2008 to 2019.

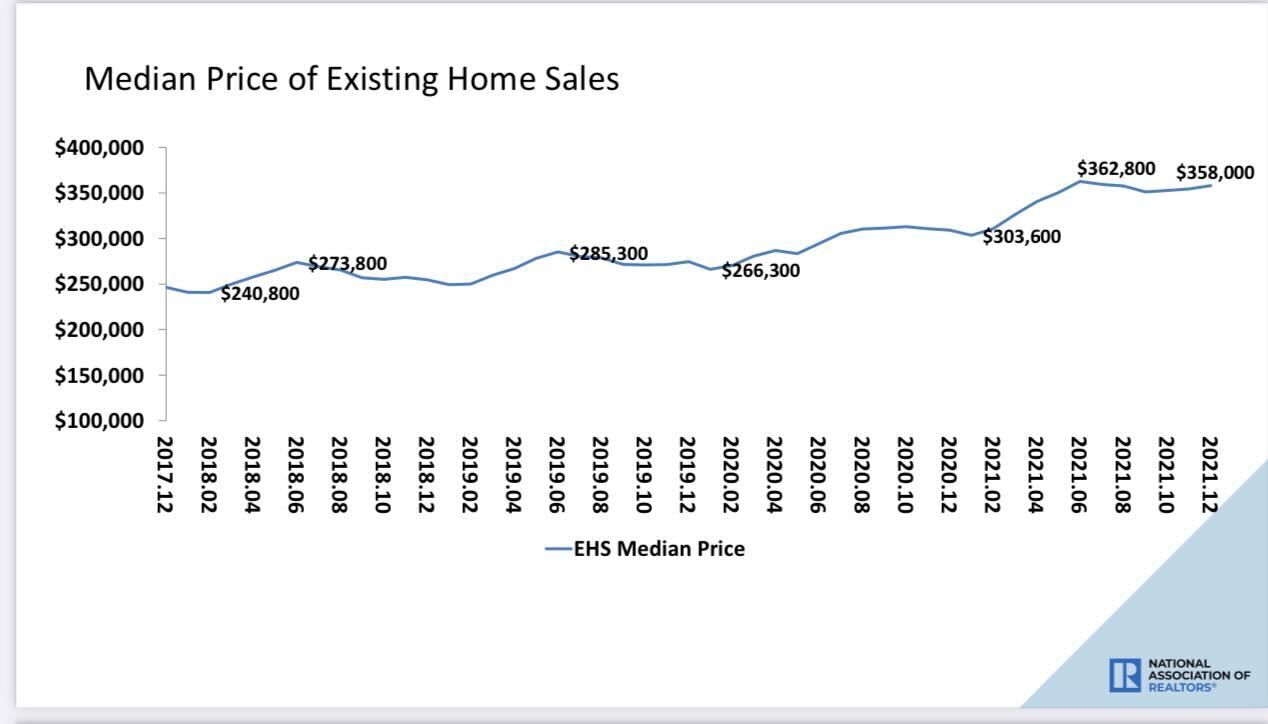

The only thing that can drive total home sales below 6.2 million is if home prices accelerate above my five-year cumulative growth rate of 23% and mortgage rates rise. The downside for housing is that my five-year price growth model has been broken in just two years. I stressed early in 2021 that people should have been more concerned about home prices overheating in 2021 than a forbearance market crash.

Still, we live in a society where professional doomsday grifting is how adults want to be remembered. The housing bubble boys of 2012-2020 turned into the forbearance crash bros of 2021 and have been nothing but an epic disaster in their forecast, which has now ended with the lost decade of bad housing calls.

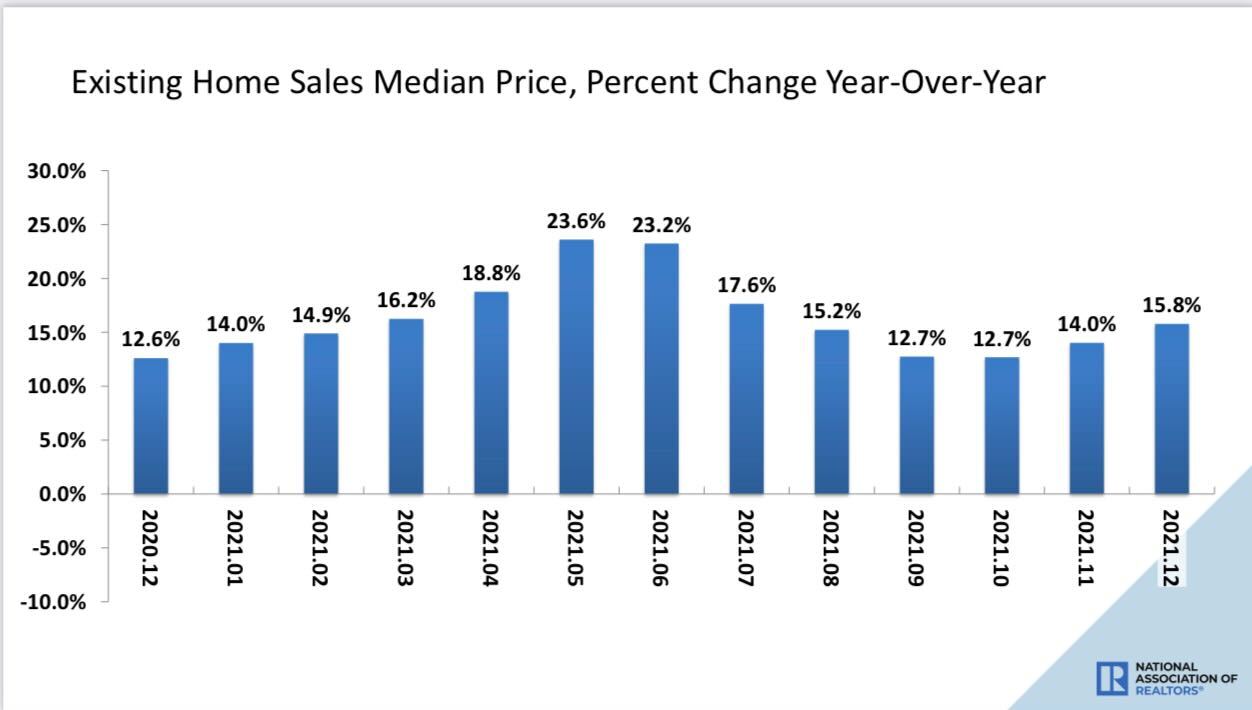

The concern in 2021 should have always been priced overheating, not crashing back to 2012 levels. As you can see below from the charts the NAR has provided, the housing crash of 2021 never occurred. The exact opposite did, however.

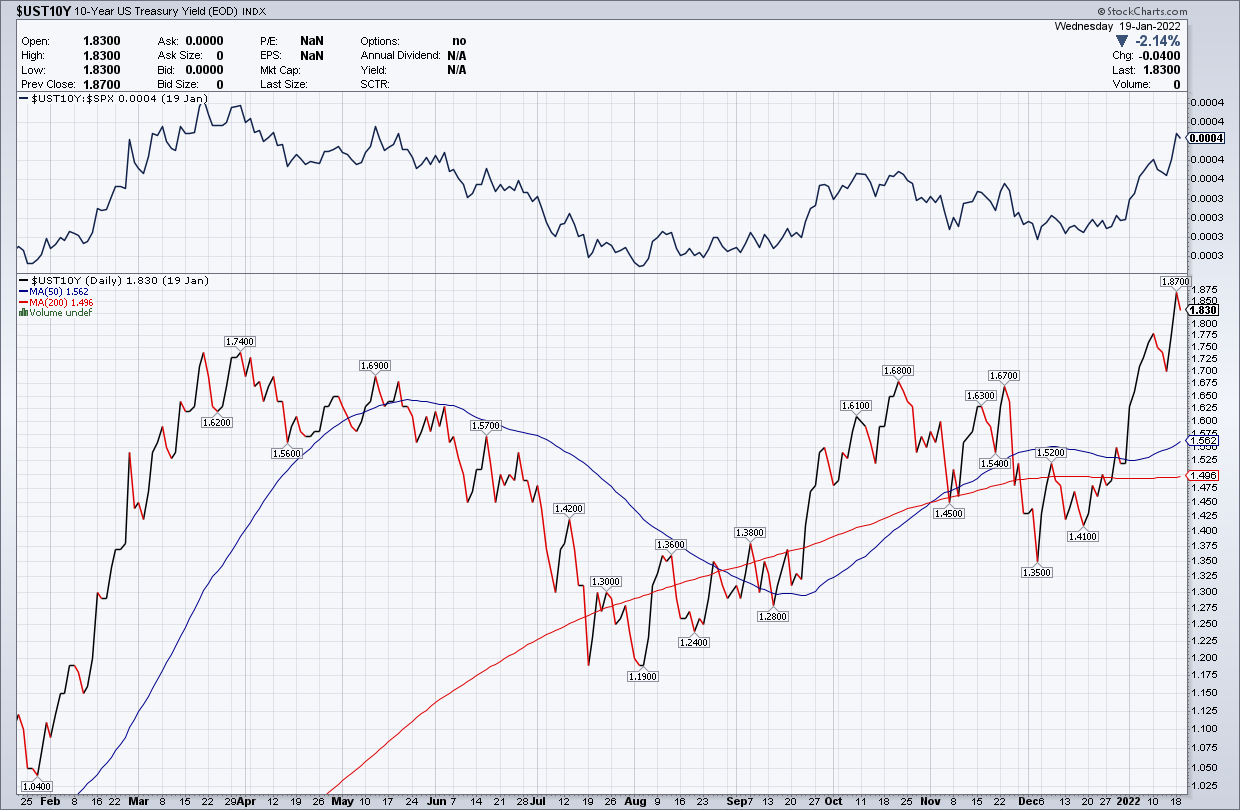

When people ask why it seems like I’m rooting for higher rates, the truth is that I believe in balance, and once the balance breaks above a trend, the faster it gets back to trend, the better. In 2021, I didn’t discuss the possibility of my crucial level on the 10-year yield breaking above 1.94%. Instead, I focused more on the range mentioned on April 7, 2020 as part of the America’s back recovery model of 1.33%-1.60%, which for the most part was created.

However, 2022 is different, and if global yields can rise together, we have a shot at breaking over 1.94% and sending mortgage rates over 4%. However, still today, even with the hottest economic and inflation data in decades, the 10-year yield as of this minute is at 1.83%.

In my 2022 forecast, my range for the 10-year yield was 0.62%-1.94%, similar to 2021. Accordingly, my upper-end range for mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. As I noted then: “This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981.

“We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.”

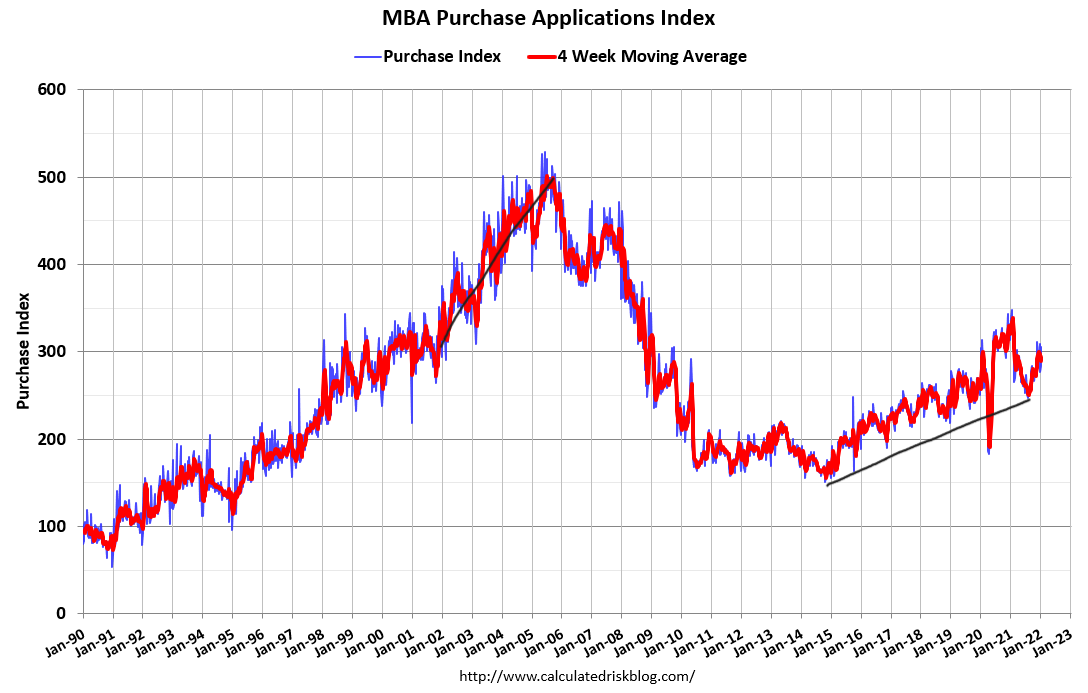

As we are getting closer and closer to the spring selling season, we are at fresh new all-time lows in inventory and mortgage rates, and the unemployment rate is below 4% still. Yikes!

Purchase application data is a very seasonal data line and the bulk of the activity in this data are really from the second week of January to the first week of May. Typically volumes always fall after May. So far, demand is stable and stable demand means it’s unlikely we will see inventory rising at a high velocity.

Remember that we still have COVID-19 comps to deal with until mid-February, so the year-over-year data needs context. Many untrained housing people were pushing for a second-half crash in 2021 due to the purchase application data being negative year over year, which means they made no COVID-19 adjustments due to the high comps in 2020. This is a terrible rookie mistake. Demand picked up toward the end of the year and inventory collapsed.

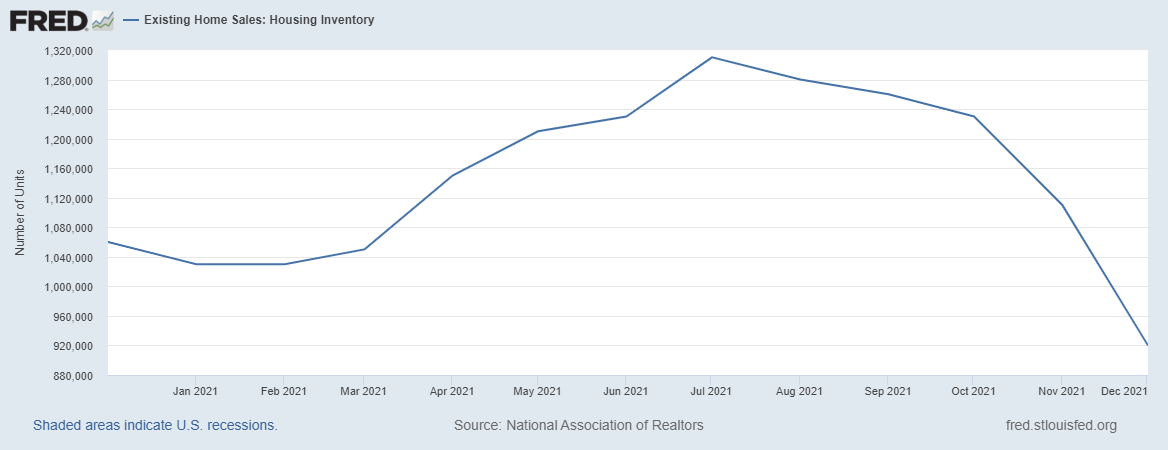

Now, total inventory levels will rise as they do every spring and summer, just as they fade in the fall and winter. The fundamental goal is to get total inventory levels between 1.52 – 1.93 million to stabilize the market. I know this is historically low inventory, but the market won’t have the prices gains as we have seen in 2020 and 2021. As we can see, we didn’t come close to creating that range in 2021, and now we are at all-time lows in inventory at 920,000 for a country where the total population is running over 322 million today.

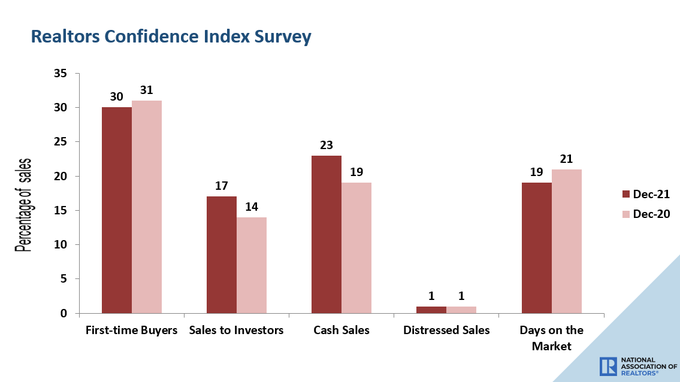

The real goal is to get the days on the market to grow. Preferably 30 days or more creates balance. As you can see below, we are far from that type of housing market.

From NAR Research: First-time buyers were responsible for 30% of sales in December; Individual investors purchased 17% of homes; All-cash sales accounted for 23% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 19 days.

From NAR Research: Unsold inventory sits at a 1.8-month supply at current sales pace, down from 2.1 months in November and from 1.9 months in December 2020.

As we can see below, the monthly supply — just like the total inventory — has collapsed. For spring and summer, this number will rise like it usually does.

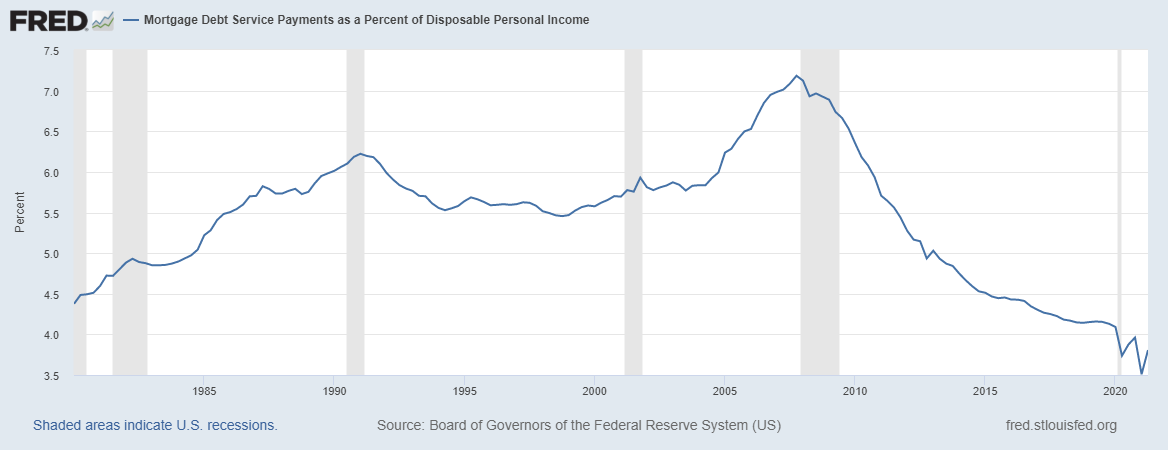

All in all, 2021 ended the year positively with demand but a terrible note on inventory. I hate that I keep saying that this is the most unhealthy housing market post-2010. However, it’s due to first-world problems: Americans create households, get married, have kids, and buy single-family homes. Americans can move up and down with the nested equity they built over the years, and all American homeowners have a fixed low debt payment cost long term to go along with their rising wages.

Our most outstanding bearish Americans are also housing crashing addicts for some dark reason. I believe that the reason they’re so angry is that people dating, having sex, getting married, having kids, and buying a home just doesn’t reflect the awful America they tend to promote. Valentine’s Day is less than a month away, and I think about the same talking points I use when I have spoken at events over the years: Americans date, mate, get married, and 3.5 years after marriage, they tend to have kids. Housing was always a 2020-2024 story, as currently our most prominent demographic patch in America are ages 28-34.