Mortgage rates inched up from last week, but still declining in three of the past four weeks, according to Freddie Mac’s latest Primary Mortgage Market survey. The shifts in average mortgage rates is slight, the experts say.

“After a sharp run-up in the early part of 2018, rates have stabilized over the last three months, with only a modest uptick since March,” Freddie Mac Chief Economist Sam Khater noted in the report. “However, existing-home sales have hit a wall, declining in six of the last nine months on a year-over-year basis.”

The National Association of Realtors reported that existing home sales fell back for the second consecutive month in May, due to a general lack of inventory.

“Closings were down in a majority of the country last month and declined on an annual basis in each major region,” NAR Chief Economist Lawrence Yun said. “Incredibly low supply continues to be the primary impediment to more sales, but there’s no question the combination of higher prices and mortgage rates are pinching the budgets of prospective buyers, and ultimately keeping some from reaching the market.”

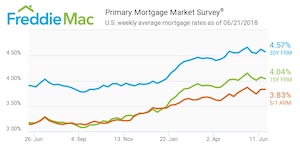

(Source: Freddie Mac)

According to the report, the 30-year fixed-rate mortgage averaged 4.57% for the week ending June 21, 2018, down from 4.62% last week, and up from 3.9% last year.

The 15-year FRM rose to an average 4.04% this week, down from 4.07 % last week and up from 3.17% in 2017.

The five-year Treasury-indexed hybrid adjustable-rate mortgage remained unchanged from last week at an average 3.83%, up from this time last year when it was 3.14%.

“This indicates that persistently low supply levels, and not this year’s climb in mortgage rates, are handcuffing sales – especially at the lower end of the market. Home shoppers can’t buy inventory that doesn’t exist,” Khater said.