Today’s Locked Mortgage Rates

While other mortgage rates sites show rates being quoted to borrowers with top credit profiles, the HousingWire Mortgage Rates Center shows actual locked rates with borrowers of all credit profiles.

Current Mortgage Rates Today: Jan. 29, 2024

30-year fixed mortgage rate: 6.687%Mortgage pricing should be slightly lower today as the 10-year yield has fallen somewhat. Unless the spreads are bad today, pricing should be better. We have a big week — jobs and the Fed!

–Logan Mohtashami, HousingWire Lead Analyst

Mortgage Rates Videos

January 29, 2024

January 26, 2024

January 25, 2024

January 24, 2024

Top Stories

Subscribe to Mortgage Rates

Receive updates when we release new Mortgage Rates content.

Polly Content Library

HousingWire Spotlight: Mortgage Mavericks, The People of Polly

Dive into the lives of Polly’s executive team in this 4 episode docuseries. Inspired by ESPN’s 30 for 30, these four short episodes explore the personal journeys, career-defining moments, and unique purpose driving the leaders shaping the future of housing.

Long Island to Leadership: Jackie Studdert’s Vision for the Future of Mortgages

Jackie Studdert’s journey from Long Island to leadership in the mortgage industry. Learn about her role at Polly, her passion for data analytics, and her vision for innovation, mentorship, and improving customer experiences in the mortgage sector.

Post-acquisition tech, capital markets and origination strategies with Rob Pieklo and Adam Carmel

On the Power House podcast, Clayton sat down with Robert Pieklo, COO of American Financial Resources (AFR) and Adam Carmel, Founder & CEO of Polly to talk about current mortgage market dynamics and growth strategies amid changing rates. They also discuss prioritizing the customer experience, effectively scaling your operations, and how to develop an adaptable product mix as we go into 2025 and beyond.

Nimble pricing engines can give LOs an advantage

Today’s unique market requires flexibility and a pricing engine that empowers lenders and their loan officers to put the right loan products in front of borrowers. HousingWire spoke with Parvesh Sahi, chief revenue officer of Polly, about the importance of having the right PPE and strategic pillars that facilitate LO success.

How one company is leading the charge to the digital evolution

HousingWire’s Editor-in-Chief Sarah Wheeler sits down with the Founder and CEO at Polly, Adam Carmel to discuss how technology can help manage margins and overall profitability and how companies can take a change-friendly stance on technology integrations in 2024.

Closer to the peak than the trough with Polly CEO Adam Carmel

On this episode, HW Media CEO Clayton Collins interviewed Adam Carmel, the founder and CEO of Polly. In this live interview at HousingWire Annual in Austin, TX, Clayton and Adam discuss mortgage pricing, capital markets, and the data that provides a glimpse into what to expect ahead.

How mortgage tech vendor options benefit lenders

HousingWire recently spoke with Adam Carmel, founder and CEO of Polly, about the benefit of vendor options in a historically gridlocked tech ecosystem.

Mortgage Rates News

Lower mortgage rates attracting more homebuyers

An often misguided premise I see on social media is that lower mortgage rates are doing nothing for housing demand. That’s ok — very few people are looking at the data with

Housing inventory falls as mortgage rates drop

Have we seen the peak in housing inventory for 2024? The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the ec

Housing demand rises as inventory falls

Even with mortgage rates higher this year than last, housing demand is up. It’s time to track the spring housing data.

Mortgage rates tick up ahead of FOMC meeting

Mortgage rates stabilized in the past week but remain close to the narrow range observed since the start of this month.

Demand for mortgages picks up: MBA

Mortgage demand continued to increase last week as some buyers acted early to lock in a house before the spring buying season.

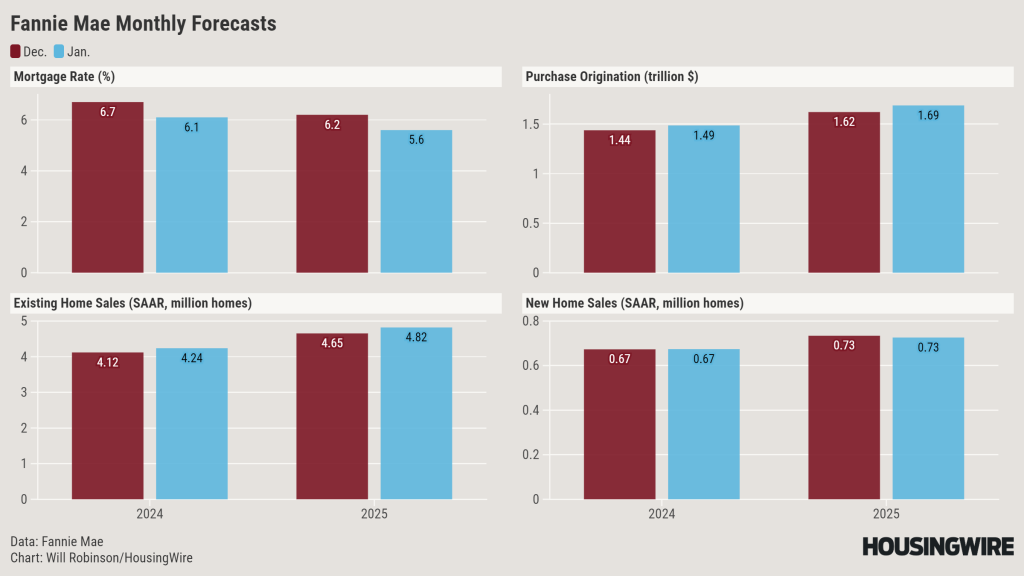

DataDigest: Fannie Mae’s market view gets rosier, but traders get more skeptical

Fannie Mae's latest monthly forecast predicts much lower mortgage rates than its December forecast — and thus more home sales and mortgage originations.

Mortgage rates, inventory and demand rise as price cuts fall

Housing inventory, new listing data and mortgage rates are all rising, but the price cut data percentages are falling.

Mortgage rates dip to 6.6% to mark the lowest level since May 2023

Mortgage rates declined to 6.6% this week to mark their lowest level since May 2023, welcome news for homebuyers who have been waiting on the sidelines.

Featured White Papers

How investing in a variety of servicing technologies streamlines operational efficiencies

Dec 21, 2023As servicers contend with a possible increase in delinquencies, one of their biggest concerns is the cost of compliance. Staying compliant can be costly, and technology can certainly assist in those efforts. Among technological acceleration, how can servicers be sure that they are selecting the right servicing technology partners and tools? They must look at […]

Frequently Asked Questions

-

What determines mortgage rates?

Mortgage rates are influenced by a number of important factors, but the primary driver is movements in the 10-year Treasury bond yield. Mortgage rates can also be influenced by inflationary pressures, macroeconomic conditions, Federal Reserve policy and housing market conditions. However, Treasury bonds and mortgage rates have tended to track each other’s movements since 1971.

The 10-year yield is driven by economic factors like GDP growth, the job market, consumer prices and inflation expectations. Inflation eats into consumers’ borrowing power. Mortgage pricing tends to spike in times of high inflation because lenders have to set rates at a level where they can still profit on loans they originate while accounting for consumers’ deflated purchasing power.

The mortgage-backed securities (MBS) market is where the business risk of originating mortgages resides. If there is more risk to the mortgage rate market, the spreads widen, causing higher rates than normal in relation to the 10-year Treasury yield. The lower the risk, the smaller the spread in rates.

A borrower’s credit score, history, down payment amount and financial profile also determine what mortgage rate offers they will get. If a borrower has a high debt-to-income ratio — meaning the amount of debt they’re paying on credit cards, auto loans, student loans and other types of loans takes up a significant portion of their gross monthly income — then lenders consider them a higher borrowing risk. As a result, they will offset that risk by charging a higher mortgage rate in case the borrower defaults on the mortgage. Similarly, the lower a borrower’s credit score or down payment amount, the higher their mortgage rate will be due to their enhanced default risk.

-

How do mortgage rates affect the housing market?

Few things affect the real estate market more than the rise and fall of interest rates, which has a ripple effect that directly influences everything from buyer behavior to market trends.

Lower interest rates make mortgages more accessible, paving the way for more buyers into the market and potentially resulting in increased demand and higher prices. Rising interest rates, however, mean higher mortgage payments, and can dampen buyer enthusiasm or affordability, slow down sales or lead to dropping home prices.

-

What is the Federal Reserve's role in determining mortgage rates?

The Federal Reserve doesn’t directly set mortgage rates, however, it sets benchmark federal funds rates that impact shorter-term forms of consumer borrowing, such as home equity lines of credit, or HELOCs. The federal funds rate is heavily influenced by economic trends and news and tends to move in the same direction with mortgage rates, but in a much slower fashion. Sometimes, the federal funds rate leads while mortgage rates follow, and vice versa. And, in some instances, they can move in opposite directions.

-

When will mortgage rates go down?

Federal Reserve Chairman Jerome Powell announced that the Fed anticipates making three 25 basis point rate cuts in 2024, a sign that a new phase in monetary policy is approaching.

NAR Chief Economist Lawrence Yun expects the first rate cut to come in the late spring of 2024. He forecasts mortgage rates to come down to the mid-6% range, for an average of 6.3% in 2024. Different factors will help bring rates down. First, rent-price growth will ease in the official data, which will help cool consumer price inflation. Additionally, the spread between the 10-year Treasury yield and mortgage rates will narrow, he said.

According to Yun, job growth will be the most determinant factor driving housing demand in the long term, while mortgage rate changes will drive demand in the short term.

-

How do you communicate rate changes to borrowers?

First, try not to get too deep into the weeds on inflation data and the details of why pricing may have improved. Clients are relying on their broker or LO’s expertise to help them navigate through the process, rather than trying to dig into the specifics of inflation and rate data themselves. The goal is to help them take advantage of the best loan scenario possible by predicting and explaining to them how pricing may change in the future.

“We find it best to always make the phone calls; whether they’re good phone calls or hard phone calls,” mortgage broker Jake Skovgard said.

For clients that are on the brink of getting an offer accepted or those who have just gotten an offer accepted, make sure you have a direct conversation about locking their loans and their rates in before doing so. Some clients may choose to heed advice and some may choose to float their locks and not lock it in yet in anticipation or hope for better pricing.

“It can be a gamble if you do that, which is why I just try and indicate my best advice to the client,” he said.

-

What will mortgage rates be in 2024?

The spread between the 10-year yield and mortgage rates can get better in 2024, which means mortgage rates could be 0.625% to 1% lower this year. For example, mortgage rates would be under 6% today if the spreads were normal. Instead, they closed 2023 at 6.67%. If the spreads get anywhere back to normal and the 10-year yield gets to the lower end of the range in 2024, we can have sub-5 % mortgage rates in 2024.

With the Fed no longer in hiking mode, any economic weakness on the labor side is a better backdrop to send mortgage rates lower. Unlike 2023, this year there are more positive variables that could send mortgage rates lower rather than higher.