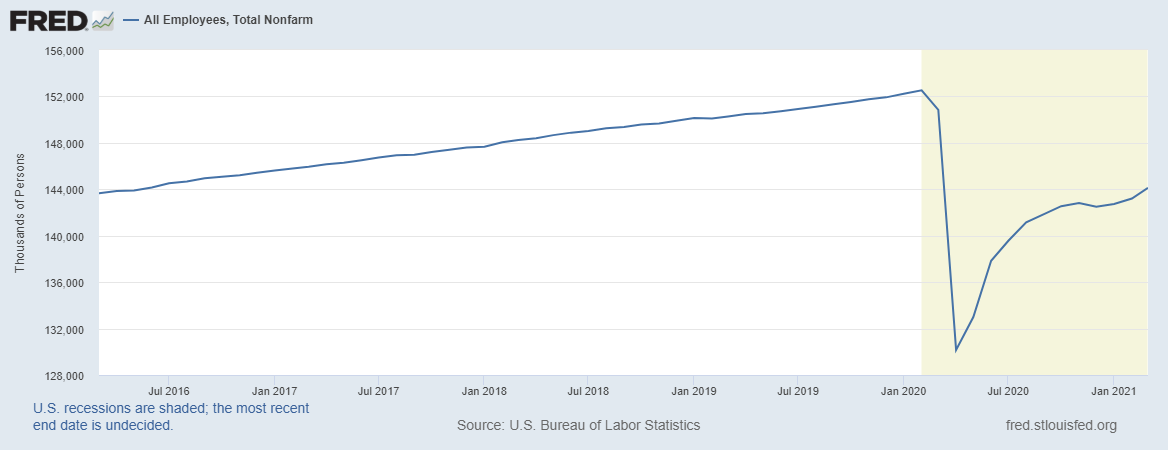

Last Friday, the Bureau of Labor Statistics reported that 916,000 jobs were created in March, and the previous month’s revisions came in positive.

This very bullish jobs report is good news for everyone except those whose livelihoods depend on forecasting doom and gloom for the U.S. economy. Among these fear-mongering ne’er-do-wells are the Forbearance Crash Bros. In 2020, I thought the housing bubble boys would win the dubious award for the most significant historical whiff of the 21st century. Then I gave them the new name of the Forbearance Crash Bros because, like most crash cult groups in America, they moved the goal post to next year.

In short, their theory went like this: The massive job losses due to COVID meant millions of mortgage holders could not make their payments. Mortgage forbearance programs allowed these borrowers to postpone mortgage payments for 12 and now 15 months. At the end of the forbearance, however, those millions of homeowners who took advantage of these programs would once again be responsible for their mortgage payments, whether or not they had been able to secure employment.

According to their theory, this could mean that millions of homeowners would simultaneously need to distress-sell or foreclose on their homes. This would drive prices down for an epic housing bubble crash across the country due to the flood of new inventory during a time when Americans couldn’t buy homes because nobody was working or making any money.

It could have happened like that in a different universe where demographics, mortgage rates, and the fact we had over 130 million people working during the worst month of COVID-19 didn’t exist.

The thing is, they didn’t have to be so wrong. A lot of the math, facts, and data that dispels their malarkey is widely available. This isn’t the 1500s when you need to dispatch horses to get information from other civilizations. Just go to the internet and read the Census data and other data trends instead of trolling the United States of America.

Here’s where they got it wrong:

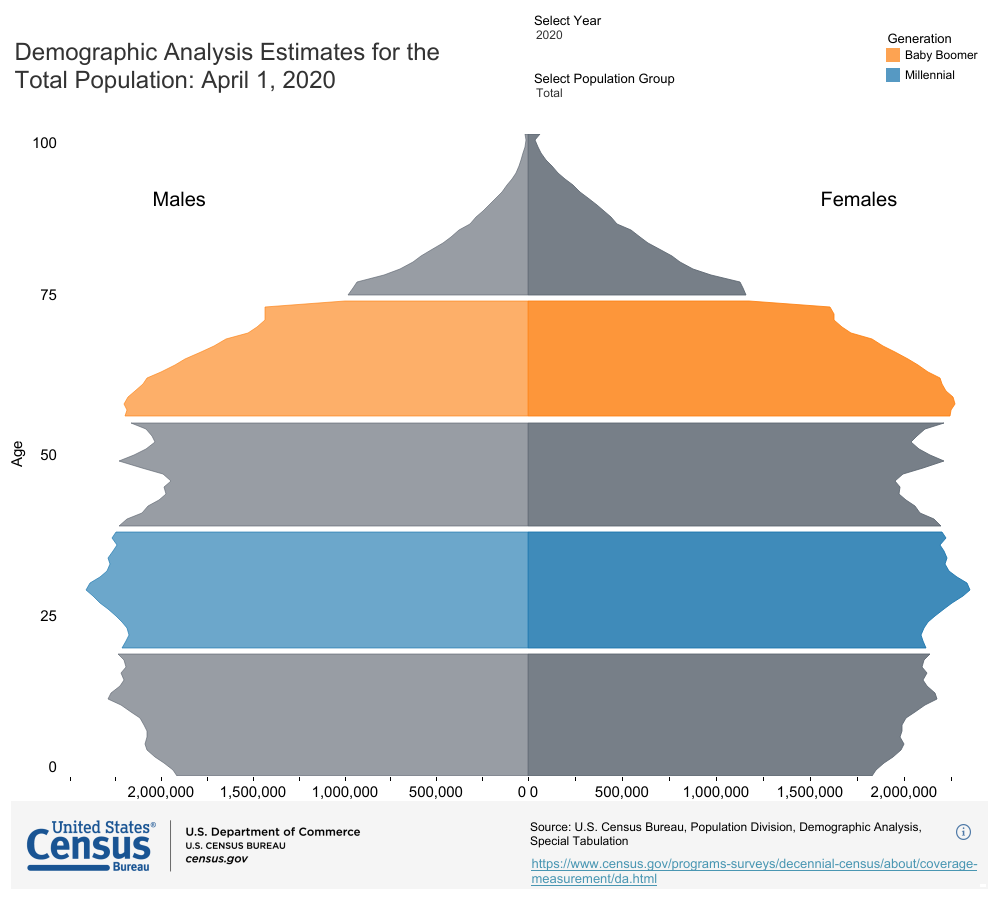

1. The years 2020-2024 have the best housing demographics ever recorded in U.S. history.

The U.S. has a vast number of folks ages 26 to 32 entering the median age of the first-time homebuyer: 33. We have demand built into our demographics for the years 2020-2024. Right now, in 2021, there are 32,458,118 people aged 27-33.

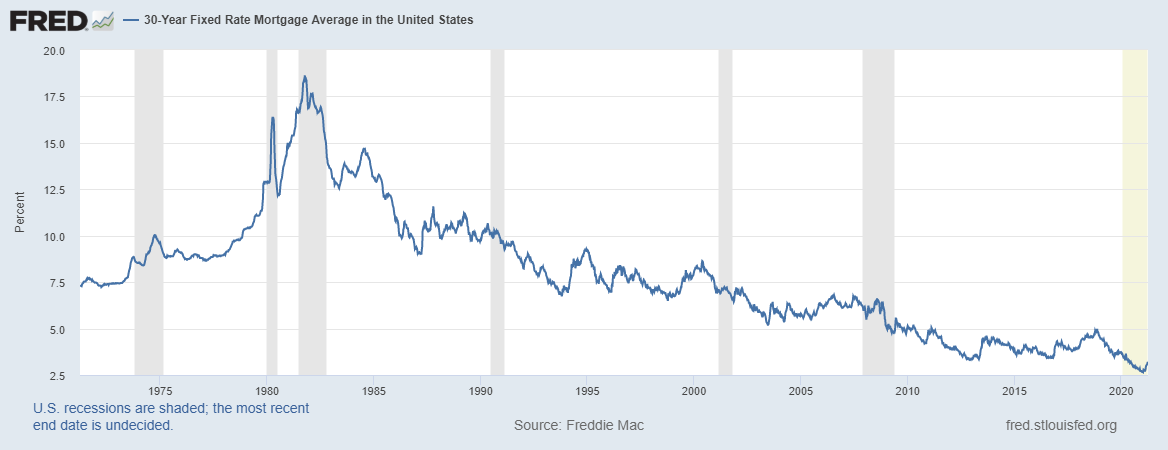

2. Mortgage rates are at the lowest levels ever recorded in history.

The downtrend since 1981 has been intact, and what COVID-19 did was send rates lower than they would have without the brief COVID-19 recession.

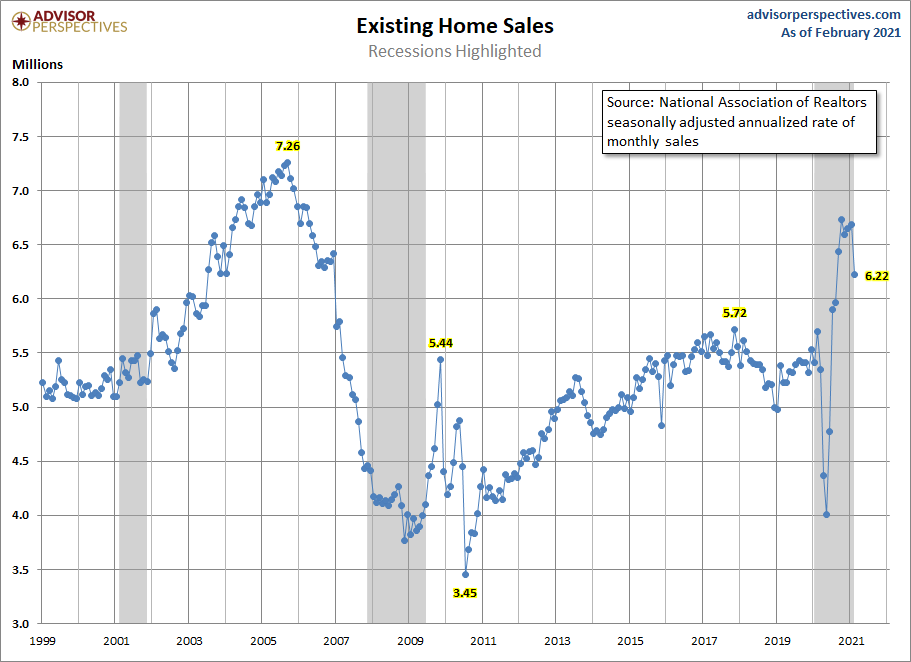

3. The housing market in the previous expansion had the weakest recovery ever recorded in history.

This means we are not working from an overheated demand cycle, where speculation demand was rampant. Even with the COVID-19 parabolic rebound in the second half of 2020, existing-home sales data ended 2020 at 5,640,000.

This amount is only 130,000 more homes bought than 2017 levels. 2019 levels were only at 5,340,000, and sales were flat compared to 2018 levels which had to contend with mortgage rates at 4.75%-5%.

4. For the U.S. housing market to crash at this point, we would need sales to decline to a level much lower than the worst levels following the housing bubble burst at a faster clip.

As I have stressed for some time now, it’s scarce to have any existing home sales prints under 4 million post-1996. Now we have the best housing demographic patch ever with the lowest mortgage rates. Do you see how crazy their crash call was! Currently, we have the problem that I feared the most: home prices are growing too hot.

But wait. There’s more:

5. Homeowner loan profiles since 2010 have been excellent.

These mortgage holders had fixed low debt costs in a climate of rising wages. Because we are no longer plagued with exotic loan debt structures, homeowners qualify for their loans with their incomes and financial assets. They had better financials to deal with a stressful event like COVID-19 than the mortgage holders of the early to mid-2000s.

6. Almost all homeowners have some level of nested equity, especially buyers from 2010-2017.

They purchased their homes with a down payment and built equity by increasing home prices and paying down the principal. The average housing tenure is at a long 10 years, so nested equity is built in.

Those who purchased in 2018 and 2019 with a low down payment have less nested equity, but their numbers are not such that they can crash the housing market even if they are forced to sell their homes in stress or even a foreclosure. If you hear any stories of foreclosures increasing, most likely they’re all backlogged foreclosure homes that finally got into the system from years ago.

7. Jobs are coming back.

This last jobs report should look like the final nail in the coffin for our doomsayers. Even if a homeowner is in a forbearance program, they can make their mortgage payment once they return to employment or even some form of income close to when they purchased the home. Some families do need dual income support to be able to own the debt. This is why the job gains from last year and this year will make a big difference.

When unemployment rates skyrocketed due to COVID-19, many people thought unemployment would stay high for a long time. As long as the virus was active and people weren’t vaccinated, unemployment would continue to be our most significant economic problem.

But since January, when we started vaccinating, jobs have been coming back. January’s jobs report came in at 49,000 and has been revised higher to 233,000. At that time, I called it “The Calm Before The Jobs Storm.”

We are now on the cusp of the second wave of job growth, and we are still early in the vaccination process. If your business can be open, hire the workers now while some unemployed folks are still left!

I now believe that I was too bearish in my prediction that we would need to wait until August 31 or thereabouts to feel like we were out of the Covid tunnel. I now think by July we will have enough of the population vaccinated that we can get back to the February 2020 total employment by September 2022 or sooner.

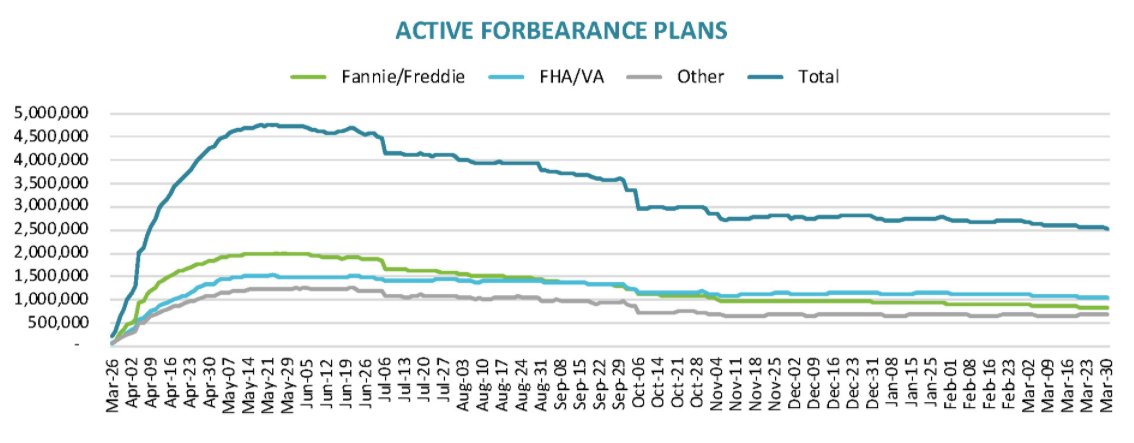

In the latest report from Black Knight, we saw 2,540,000 mortgage holders were in a forbearance program. However, I don’t think that is the number of mortgage holders in current financial stress. I believe that number is lower. Remember, some folks got into a forbearance program just because they could.

The Forbearance Crash Bros needed the initial numbers to get toward 10 million to 15 million — the same levels during the housing bubble crash years of loans in delinquencies. The exact opposite has happened; the numbers went lower as they should have, and we are already out of the recession with jobs about to have their second wave of growth.

We can expect a lag between the improving jobs data and numbers falling in the forbearance programs. Many households need dual incomes to afford the mortgage payment. Those households will need to wait until both homeowners gain full employment before they are comfortable in getting out of the forbearance program. So there is some risk out there.

The other factor that is important to remember when thinking about the risks to the housing market posed by forbearance is that many of the people who are still unemployed and getting government disaster relief dollars are renters. It is sad to say that those most affected by the economic chaos caused by COVID were those lower on the economic scale. Those with incomes over $60,000 per year have mostly regained employment or never lost it.

We are on the verge of getting all the jobs back and then creating an extra 2 to 3 million jobs for the lost year due to COVID-19. When the economy does reopen in full force, the 8.4 million Americans who remain unemployed due to COVID-19 will gain employment. We are also on the verge of an economic victory for the United States of America and a spectacular fail for the country’s housing crash forecasters.

The reality is that we are just in a much better place than we were last April. Back then, on April 7, 2020, I wrote my America is Back economic recovery model and these words will always stick with me until death.

I wrote:

“I believe the months of April and May are going to tell an epic story of America’s start in defeating this virus. If we do this right and document the cause and effect of our efforts, future generations will be able to look to this period in time for how to handle a global pandemic.

“My faith in America winning has never let me down because I always believe in my people and country. I can tell you now; this virus isn’t changing my view on that.”

Guess what, Forbearance crash bros — you lost, America won!

This is a great post that I expect will age well.

🇺🇸💪🏽📈🔥