On Thursday, the Bureau of Labor Statistics (BLS) reported that Consumer Price Index (CPI) inflation came in hotter than expected, and people are scared that the Federal Reserve will now be more aggressive with their rate hikes. Personally, I believe the Fed knows that rental inflation data can lag so at this point of the rate hike cycle, they won’t act in a more aggressive fashion. Here’s why.

The extra heat of this report was primarily due to how hot shelter inflation has been coming in on the data line. I recently discussed how shelter inflation has legs in 2022 but should change in 2023 on the CPI reports. The way BLS accounts for shelter inflation has a noticeable lag to more recent data.

From BLS: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.4 percent in September on a seasonally adjusted basis after rising 0.1 percent in August, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 8.2 percent before seasonal adjustment. Increases in the shelter, food, and medical care indexes were the largest of many contributors to the monthly seasonally adjusted all items increase.

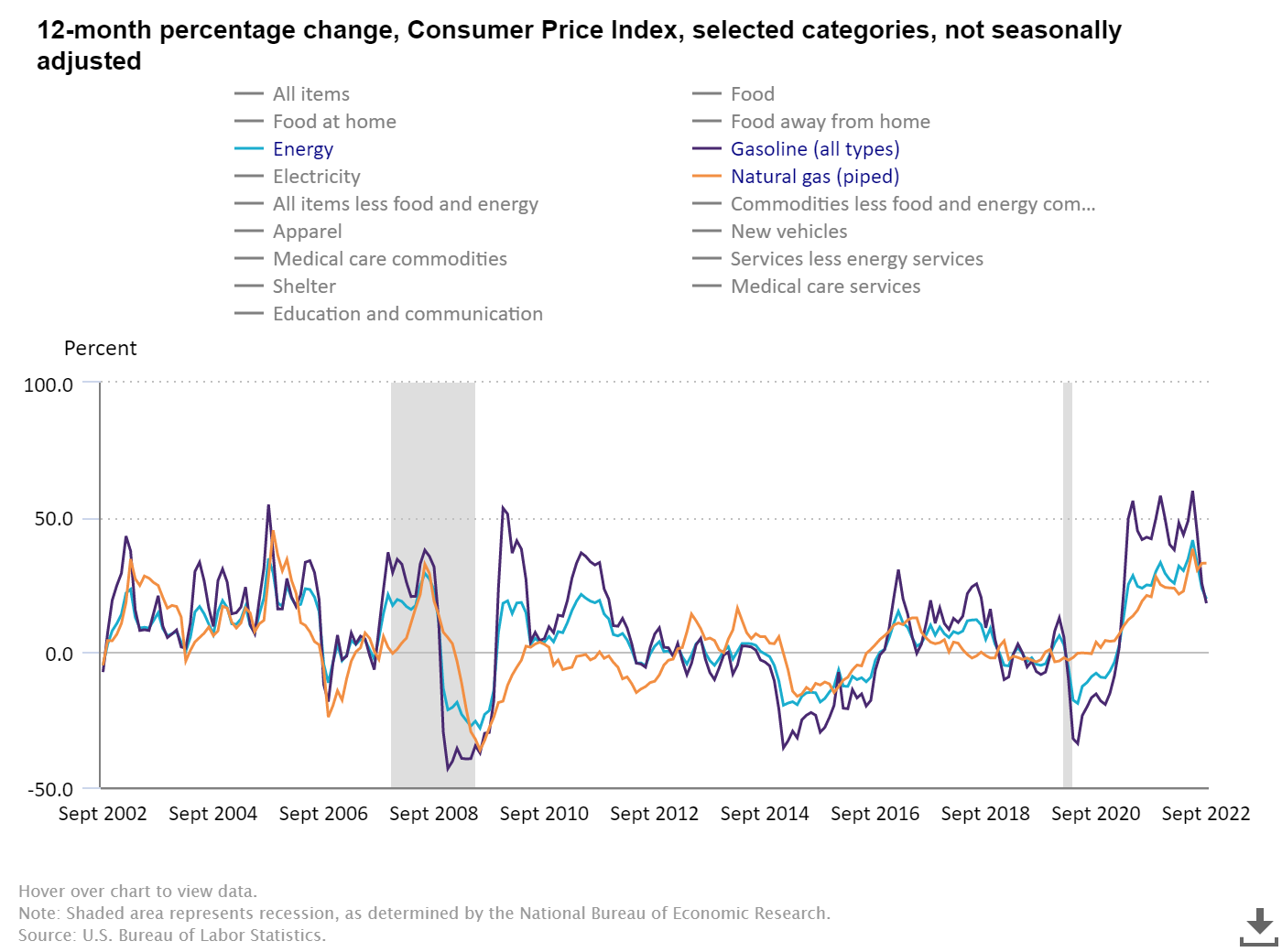

Headline inflation has been dropping recently from its peak, which is primarily due to the decline in oil and gas prices, as you can see in the chart below.

Shelter inflation has recently given core inflation the legs to stay firm and head higher. This is why we have some divergence between core inflation and headline inflation. Core Inflation excludes energy and food prices because they can be very volatile.

Shelter inflation is roughly 43% of the component of core CPI, so it’s a big deal. In the previous expansion, it was very steady, with no real break away with shelter inflation. Shelter inflation never hit 4% in the previous expansion. However, as we can see, like everything else post-COVID-19, things are different on the inflation side of the equation. The very brief pullback in shelter inflation was not only reversed but it was reversed in a historical fashion.

This should not surprise anyone because housing inflation has been the main story since 2020. Rent inflation is cooling down but it will not show up on the CPI data line until the middle of next year. Last month on CNBC, I talked about this topic and how the growth rate will cool, but it’s a 2023 story.

“Core inflation could stick over 2% faster and longer in this expansion because shelter inflation should pick up. If we do really see wage growth at the bottom end, landlords will ask for more rent.”

– Logan Mohtashami

During the summer of 2020, when shelter inflation was falling and people were saying cities are dead and rent inflation is going to fall more, I was in the camp that shelter inflation was already growing and had the potential to really grow. A lot of Americans had already gotten their jobs back and the rest were getting checks, so shelter inflation had the potential to go higher.

Back in the summer of 2020, the data line was still heading lower, but that data line lagged the current reality. It’s the exact case now as rent inflation is cooling down, but it won’t show up in the CPI data until late

My quote to The Washington Post early in 2021: “Core inflation could stick over 2% faster and longer in this expansion because shelter inflation should pick up. If we do really see wage growth at the bottom end, landlords will ask for more rent.”

Just as the S&P CoreLogic Case Shiller Home Price data lags the current market, shelter inflation lags on the CPI.

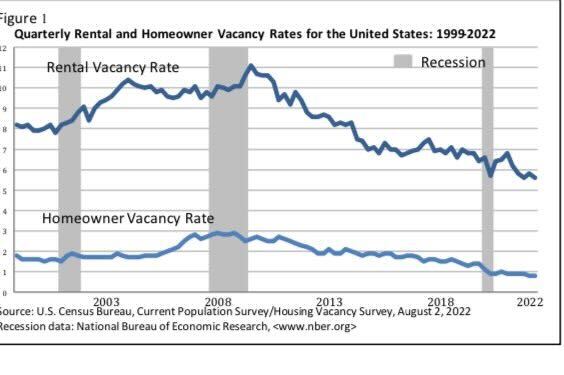

Shelter inflation is not that complicated to understand. Rental vacancy data has been falling for decades, and rent inflation has been growing. Just like home prices, we got caught in a bad place with supply so shelter inflation blasted off.

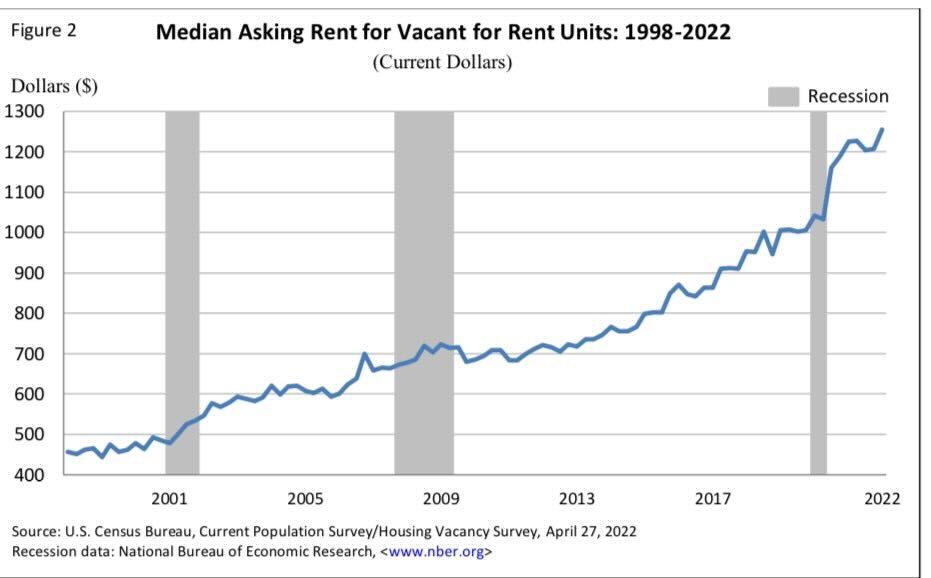

As you can see below, rent inflation took off like home prices did. Having shelter inflation go negative is rare because most Americans are always working and paying their rent on time. However, rent inflation since 2020 has been historic and it has been savagely unhealthy regarding housing inflation.

However, looking to the future, this data line should be cooling down, especially in the second half of 2023, when the comps will be hard to work from. More multifamily construction is coming online which means we will have more supply of rental units. The best way to deal with inflation is more supply. Even as wage inflation has been taking off, more supply will always cool down inflation.

Super high rent growth can’t be super hot forever because wages simply can’t keep pace with the double-digit rent growth we have seen in certain parts of the U.S. Eventually, hotter inflation data kills demand; we see this with the massive home-price gains we have seen in the U.S. post-2020; once rates broke over 4% and headed higher, demand got impacted.

Of course, homeowners who have a fixed payment and refinanced recently have increased their wages without the pain of rent inflation hitting them. This is why some people refer to a fixed mortgage payment as a hedge against inflation. Imagine all those homeowners who refinanced to mortgage rates below 4% — they’re not dealing with high rent inflation, but their wages are growing faster. Almost 65% of all Americans have mortgage rates 4% and below, so that is a significant portion of the country. And of course, more than 40% of homes in the U.S. don’t have a mortgage to deal with at all.

While inflation is still a problem and shelter inflation is in the driver’s seat on the CPI reports, I believe, for the most part, people understand that the CPI shelter data lags — it is not as hot as it looks in the data right now. However, we do need to wait until mid-2023 and toward the end of next year to see it show up in the CPI report, which can lower the growth rate of core inflation.

Financial markets initially had a very negative response to the data, and the 10-year yield shot up well above 4% in early trading on Thursday, with the markets down, only to reverse course later in the day.

We still have a long way to go to get down to the 2% inflation that the Fed is comfortable with. However, in 2023, these hot shelter prints should cool down. As more supply hits the market in the coming months, the growth rate will be brutal to maintain — we already see this in other data lines.

This is very important for the housing market because if the growth rate of the biggest driver of inflation is fading, that means the rise in mortgage rates is coming to an end and maybe we can have a more steady move lower in rates next year.