When Federal Reserve Chairman Jerome Powell talked about a housing reset in June, it sent shockwaves around the country because it sounded so ominous. In the most recent FOMC meeting, held last week, Powell finally clarified what he meant by that term and what a housing reset means to the Fed. However, a housing reset isn’t the only pressing issue — we now also have to think about a worldwide global recession.

To put it as simply as I can, the strength of the U.S. dollar is causing too much pain worldwide, and traditionally something breaks when this happens. China is in a mess, Europe has an energy crisis, and the wild card of Russia’s war in Ukraine is still unresolved, all while the Fed is aggressively hiking rates. Savagely unhealthy is no longer just a term for the U.S. housing market — it now applies to the world economy.

As I noted during my recent podcast on HousingWire, things are getting sloppy in the markets, and when chaos happens, you can’t ever be sure how bad the damage is going to be. Over the weekend, Raphael Bostic, president of the Federal Reserve Bank of Atlanta, said, “We are going to do all that we can at the Federal Reserve to avoid deep, deep pain.” It’s never a good thing when you have to qualify pain like that.

What a housing reset means

Let’s take Chairman Powell’s words from the FOMC’s Q&A session on Sept. 21 and discuss what a housing reset means.

Powell: So when I say reset, I’m not looking at a particular, specific set of data or anything…

This isn’t true (just look at his next statement, below) — he really wants the bidding wars to end, and for total inventory to grow and regain balance. I can understand this mindset. As you can see below on the NAR total inventory chart, we didn’t have a seasonal push in inventory in 2020, which left us vulnerable to price growth that was above the historical norm.

Powell: What I’m really saying is that we’ve had a time of a red-hot housing market, all over the country, where famously houses were selling to the first buyer at 10% above the ask, before even seeing the house…

As you can see, Powell quickly outlines precisely what he doesn’t want to see: massive bidding wars for housing. He wants to see balance. This is something I have talked about on HousingWire for some time. We lost balance in the housing market, and an unhealthy housing market became savagely unhealthy in 2022.

Powell: So, there was a big imbalance between supply and demand and housing prices were going up at an unsustainably fast level. So the deceleration in housing prices that we’re seeing should help bring sort of prices more closely in line with rents and other housing market fundamentals, and that’s a good thing.

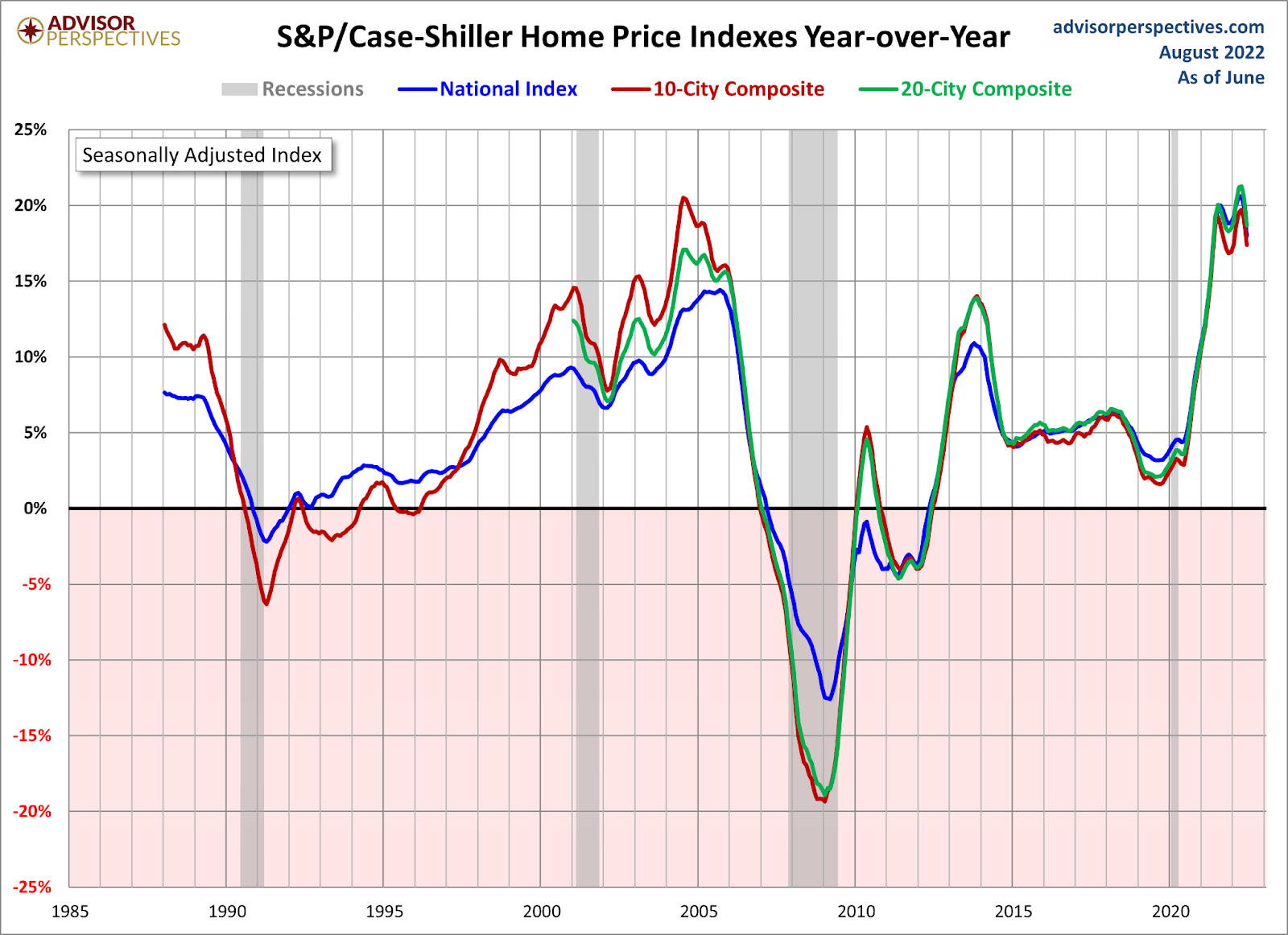

Home-price growth was way too hot to start the year, and home prices falling is sticky unless you have a massive increase in supply and forced selling. Home price growth in 2022 is cooling down from 2021 levels, but it will still be positive and higher than I would like to see. The S&P/CoreLogic Case Shiller Index is coming out this week; this data line lags the current market, but expect a cool down in price growth data here.

Powell: For the longer term, what we need is supply and demand to get better aligned so that housing prices go up at a reasonable level, at a reasonable pace, and that people can afford houses again, and I think we, so we probably in the housing market have to go through a correction to get back to that place.

Now my personal working thesis is that the housing market can functionally work once total Inventory data can get between 1.52 – 1.93 million. Once we hit the top-end number of 1.93 million, I can remove the savagely unhealthy theme. Any parts of the U.S. already into the 2019 inventory range are already out of the savagely unhealthy housing market because they have choices.

While this isn’t a 2022 story for national inventory levels, the last report of the NAR showed a decline from 1.31 million to 1.28 million levels. We are still going to start 2023 in a better place with inventory than what we started 2022 in.

Powell: There are also longer run issues though with the housing market. As you know, we’re, it’s difficult to find lots now close enough to cities and things like that, so builders are having a hard time getting zoning and lots, and workers and materials, and things like that. But from a sort of business cycle standpoint, this difficult correction should put the housing market back into better balance.

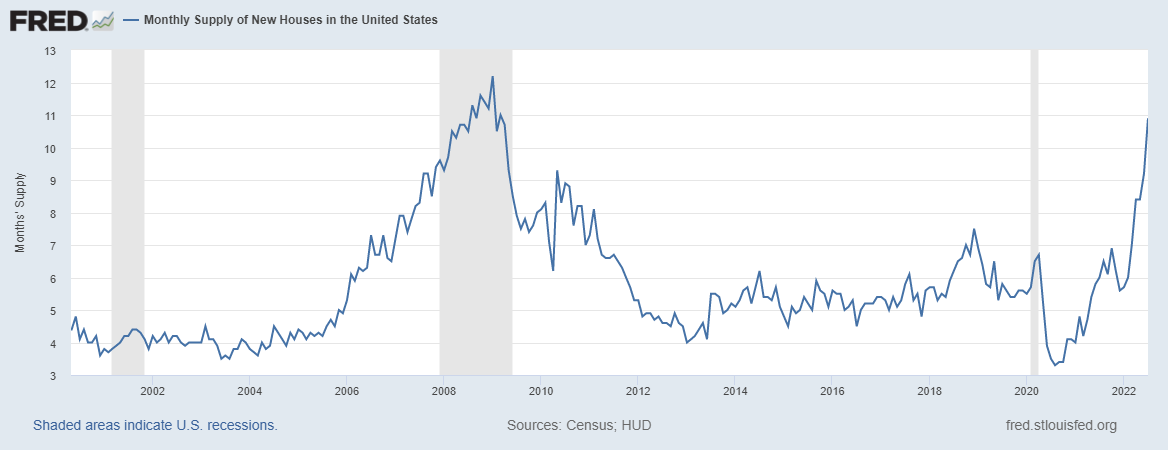

This is almost useless; the housing market has already gone into a recession, and the builders are done building anything new until they get rid of the excess supply they already have. New home sales are coming this week, and the monthly supply data is too big to have any new construction being built.

We have 10.9 months of housing supply with 9.84 months in construction. The builders will take their time finishing these homes and ensuring they sell them at a price that is useful for their business model.

Powell: I think that shelter inflation is going to remain high for some time. We’re looking for it to come down, but it’s not exactly clear when that will happen. So, it may take some time, so I think hope for the best, plan for the worst. So I think on shelter inflation you’ve just got to assume that it’s going to remain pretty high for a while.

Some data lines show that the growth rate is cooling off. The CPI shelter inflation data will show this in 2023, not this year. The Fed knows this. Here is a clip of my take on CNBC on this subject. Look for shelter inflation data to cool down in 2023.

That was my take on the housing reset/housing correction, or whatever the Fed calls it next. We need more supply and growth rate of pricing to cool. Powell also talked about the MBS market. When asked whether housing market conditions might affect the Fed’s plans for MBS, Powell answered:

POWELL: So we, what we said, as you know, was that we would consider that once balance, runoff is well underway. I would say it’s not something we’re considering right now and not something I expect to be considering in the near term. It’s just, it’s something I think we will turn to but that time, the time for turning to it has not come and is not close.

In code, this means rates are already up a lot, so we don’t feel the need to sell MBS. Don’t overthink this one; they know they’re wreaking havoc on housing and don’t need rates to go much higher than they’re today. When rates fell back to 5%, they were very upset about that. Some Fed speakers talked about selling MBS to scare the market into higher rates. I believe they’re happy with where the rates are at.

The effect on world markets

Now, let’s consider the effect of the Fed’s rate hike on the world markets. With the dollar getting stronger and stronger, world markets are falling into chaos mode. This traditionally isn’t a good thing, but it’s the world we live in. Remember, the Fed wants higher unemployment; they believe that is the most effective way to deal with inflation and the growth rate of wages.

With my six recession red flags up and global economies and markets in chaos, I will say the Fed is making sure that we do see higher unemployment here and around the world. The way the world markets are reacting shows me that the Fed has lost some control here, which wasn’t the case in the past few months.

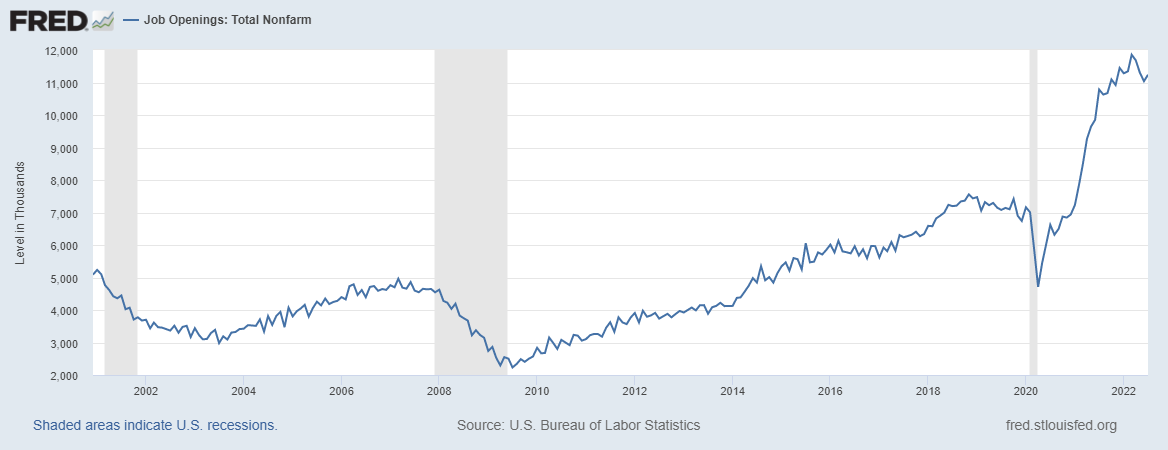

Will they adjust to this current reality and stay the course? Time will tell. However, for me, the Fed’s focus is getting people unemployed as soon as possible, so the data lines to track now are job openings, which are still over 11 million.

Jobless claims came in at 213,000, an extreme low historically. These two data lines are what the Fed is focusing on, and as long as they’re healthy, they will continue to push the higher unemployment rate to bring down wage inflation and inflation in general. This is despite the havoc created by stronger dollar around the world.

With the dollar getting stronger, we are exporting inflation at a time when the world is also fighting inflation. This is what we call a double whammy. It’s great for those people who want to vacation in London now, however, the financial markets around the world are stressed as financial conditions are getting tighter.

This question was asked to Powell:

Neil Irwin: Thanks, Neil Irwin with Axios. A number of commentators have come to the view, including over at the World Bank, that simultaneous global tightening around the world is, creates a risk of a global recession that’s worse than is necessary to bring inflation down. How do you see that risk? How do you think of coordination with your fellow central bankers? And is there much risk of overdoing it on a global level?

Powell: So we, actually my colleagues and I, a number of my FOMC colleagues and I just got back from a, one of our frequent trips to Basel, Switzerland, to meet with other senior central bank officials from around the world. We are in pretty regular contact, and we exchange, of course we all serve a domestic mandate, domestic objectives, in our case the dual mandate, maximum employment, price stability, but we regularly discuss what we’re seeing in terms of our own economy and international spillovers, and it’s a very ongoing, constant kind of a process.

So we are very aware of what’s going on in other economies around the world and what that means for us, and vice versa. Our, the forecast that we put together, that our staff puts together, and that we put together on our own, always take all of that, try to take all of that into account. I mean I can’t say that we do it perfectly, but it’s not as if we don’t think about the policy decisions, monetary policy and otherwise, the economic developments that are taking place in major economies that can have an effect on the U.S. economy, that is very much baked into our own forecast and our own understanding of the U.S. economy, as best we can. It won’t be perfect.

So, I don’t see, it’s hard to talk about collaboration in a world where people have very different levels of interests rates. If you remember, there were coordinated cuts and raises and things like that at various times but really, really we’re all, we’re in very different situations. But I will tell you, our contact is more or less ongoing and it’s not coordination but there’s a lot of information sharing and we all I think, are informed by what other important economies, economies that are important to the United States, are doing.

As you can read above, Powell tries to assure people that the Fed does talk to their counterparts all around the world and are keeping up on things. After the Fed’s press meeting, the pound collapsed to all-time lows over the weekend and the markets have gotten much worse after the Fed meetings. If we are to hold Powell to his word, the Fed has to be on the phone with their counterparts to see what can be done to try to calm markets down.

When mortgage rates fell recently from 6.25% to 5%, bond yields fell and stocks rallied. The Federal Reserve was upset about this outcome because it made financial conditions easier and gave some hope on the economy. This isn’t what the Federal Reserve wants, so they pushed a campaign out to talk the markets down and get people on board that a recession is needed to cool down inflation, which means higher rates for longer.

Now that the U.S. housing market and other economies across the globe are feeling the pain, the Fed is getting its wish by pushing us closer and closer to a recession to join the world economies in a downturn.

In my local Washington D.C. metropolitan market I’m starting to get calls from potential 2023 sellers wondering if they should list right away. They’re worried about rated going up and priced falling off a ledge. With inventory still very low I don’t see big price drops ahead but definitely more days on market. For brokers more inventory would be a very welcome result of these rate hikes. We need more units to churn out some sales in 2023.