Jobs week cleared up the skies for the Federal Reserve members, who are smiling — big time — after a series of data lines gave them what they wanted: a softer labor market!

While the labor market isn’t breaking, it has become more pliant in the data lines the Fed focuses on. After Friday’s jobs report, which had some one-time variables, we can say that the economy is heading into an area where the Fed will feel much more comfortable, and we should not have any more rate hikes.

We need to focus on this week’s data to better understand the labor market. First, let’s take a look at Friday’s jobs report.

From BLS: Total nonfarm payroll employment increased by 187,000 in August, and the unemployment rate rose to 3.8 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in health care, leisure and hospitality, social assistance, and construction. Employment in transportation and warehousing declined.

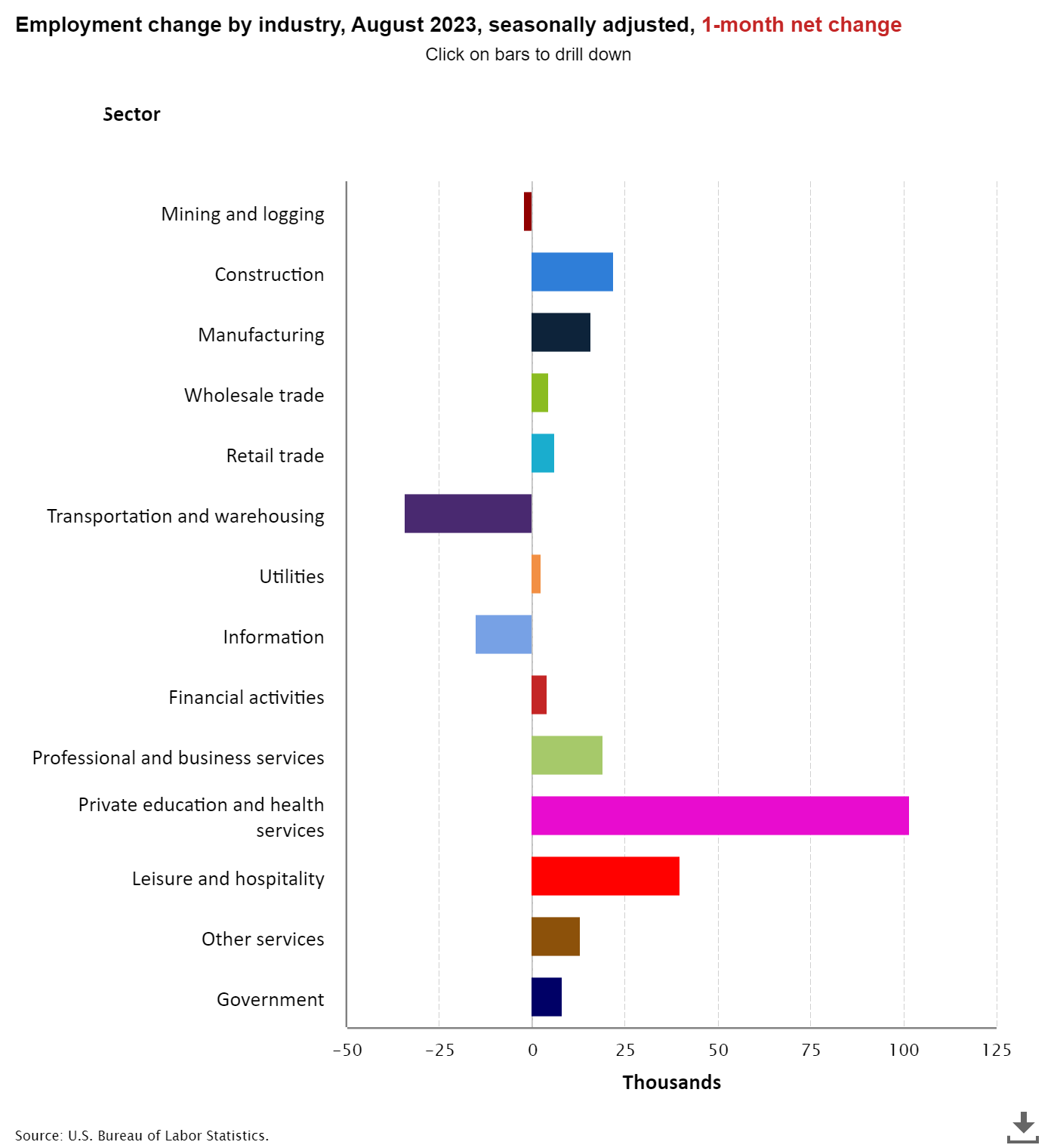

The headline number beat estimates but had negative revisions in the previous months; we had a big jump in the labor force, which was the biggest reason the unemployment rate ticked up higher. We also had some one-time variables as one trucking company filing for bankruptcy, and the actors’ strike, which hit the data this month. Here is the breakdown of the jobs gained and lost:

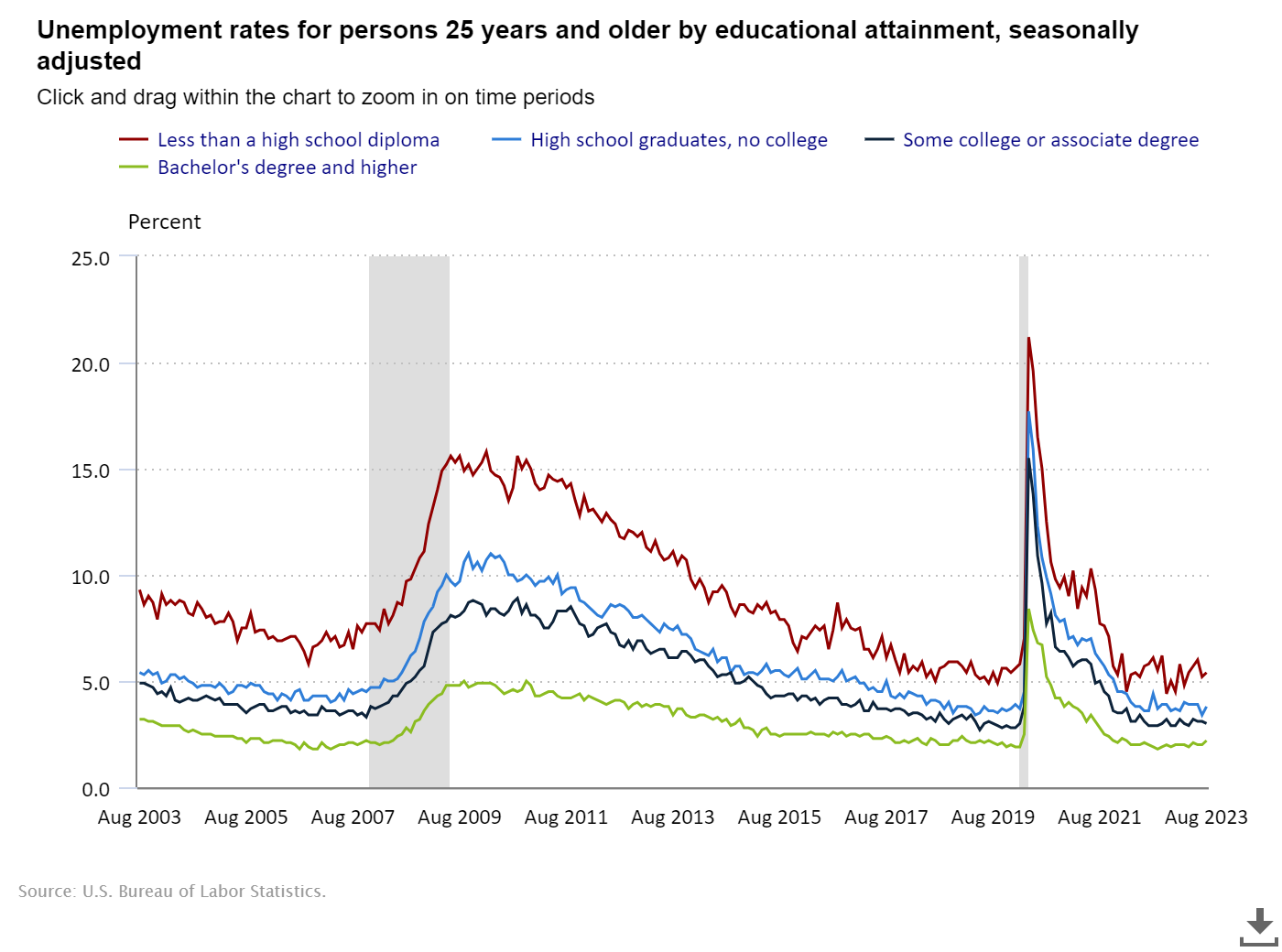

In this job report, the unemployment rate for education levels:

- Less than a high school diploma: 5.4% from 5.2%

- High school graduate and no college: 3.8% from 3.4%

- Some college or associate degree: 3.0%

- Bachelor’s degree or higher: 2.2% from 2.0%.

The key to the unemployment rate jumping was a big move in the labor force, especially from ages 55 plus in this report.

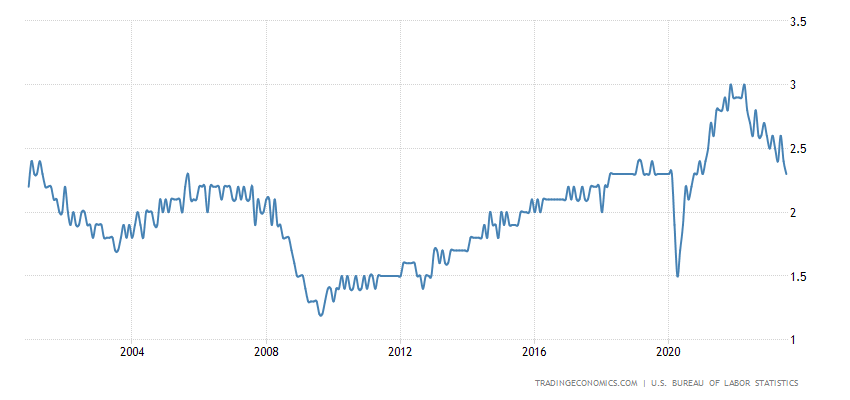

The Federal Reserve’s fear of wages spiraling out of control like we saw in the 1970s wasn’t a valid concern. As the growth rate of inflation fades, so should their fear on this topic. Wage growth has been slowing down since January of 2022. It might still be too hot for the Federal Reserve, but anyone who isn’t blind can see it’s not spiraling out of control. As the chart below shows, average hourly wage growth data is slowing down from a hot level.

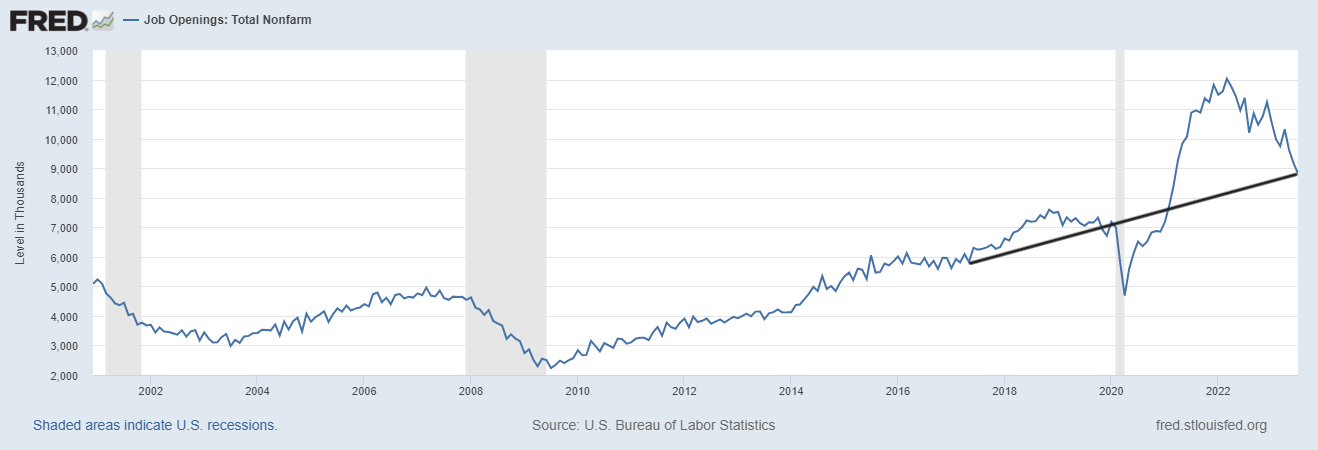

Job openings

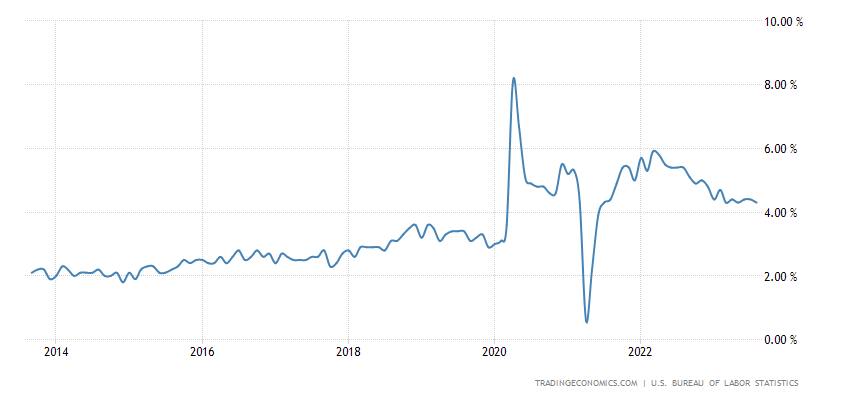

The job openings data is one of the Fed’s favorite labor market indicators: They use it to talk about how tight the labor market is. I believe the Fed members want to see the job openings data return toward 7 million so they have to be very pleased with the job openings falling below 9 million this week. As we can see in the chart below, the labor market isn’t as tight as it used to be.

Quits rate

Another great data line for the Fed this week is that the quits rate has returned to pre-COVID-19 levels. With fewer people quitting for better-paying jobs, this makes the Fed much happier, especially in the lower-wage service sector, because people making more money on the low end isn’t something the Fed will tolerate. As Fed members have said recently, they want to see labor softness in the service sector.

This was an epic jobs week because the Fed can say that they’re really making progress on attacking the labor market. Once you get a trend in labor data, it’s tough to reverse course quickly, especially as the Fed is in restrictive territory with their rates. Let’s not forget that the student loan debt payments are about to go online, which means less disposable income in the economy. The 10-year yield is slightly below my peak forecast for 2023 of 4.25%, sitting currently at 4.18%.

The things to focus on for the next 12 months are: the Fed is in restrictive territory with rates, student loan debt payments are about to start again and the labor market is getting less tight. When I say Fed members are happy about this week, it’s an understatement. They are very excited that the economy has a lot of variables that will attack the labor market.