What does it mean to get a positive job report with all the talk about a recession, which ramped up starting in January 2022? Let’s look at the U.S. jobs and economic numbers as five of my six recession red flags are up today.

The June data shows that we added another 372,000 jobs as we get closer to the employment numbers before COVID-19. We did have 74,000 negative revisions to the previous reports, however, the internals of this jobs report is the most interesting aspect. Let’s take a look together.

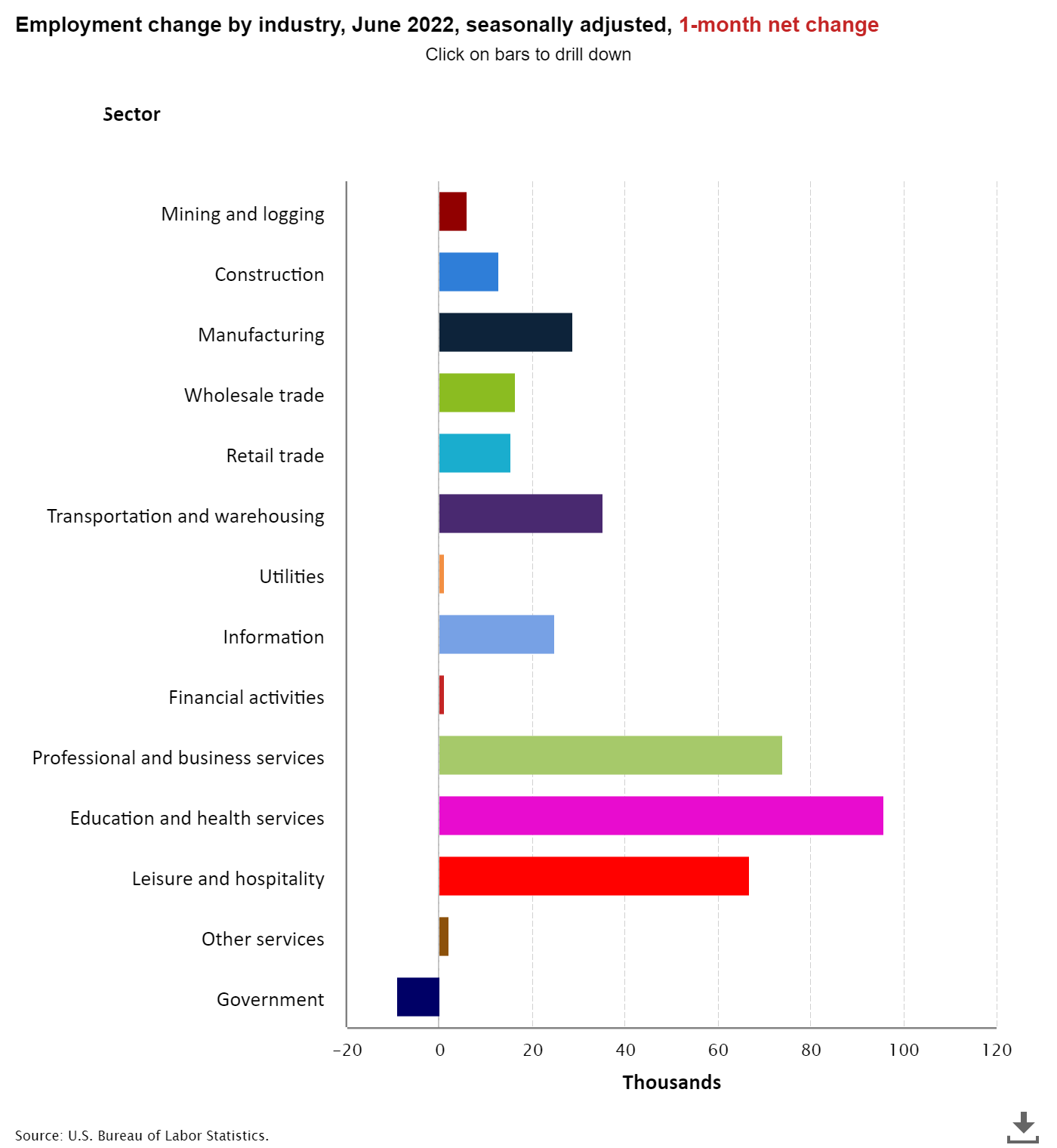

From the Bureau of Labor Statistics: Total nonfarm payroll employment rose by 372,000 in June, and the unemployment rate remained at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in professional and business services, leisure and hospitality, and health care.

The unemployment rate for men and women ages 20 and over is 3.3%.

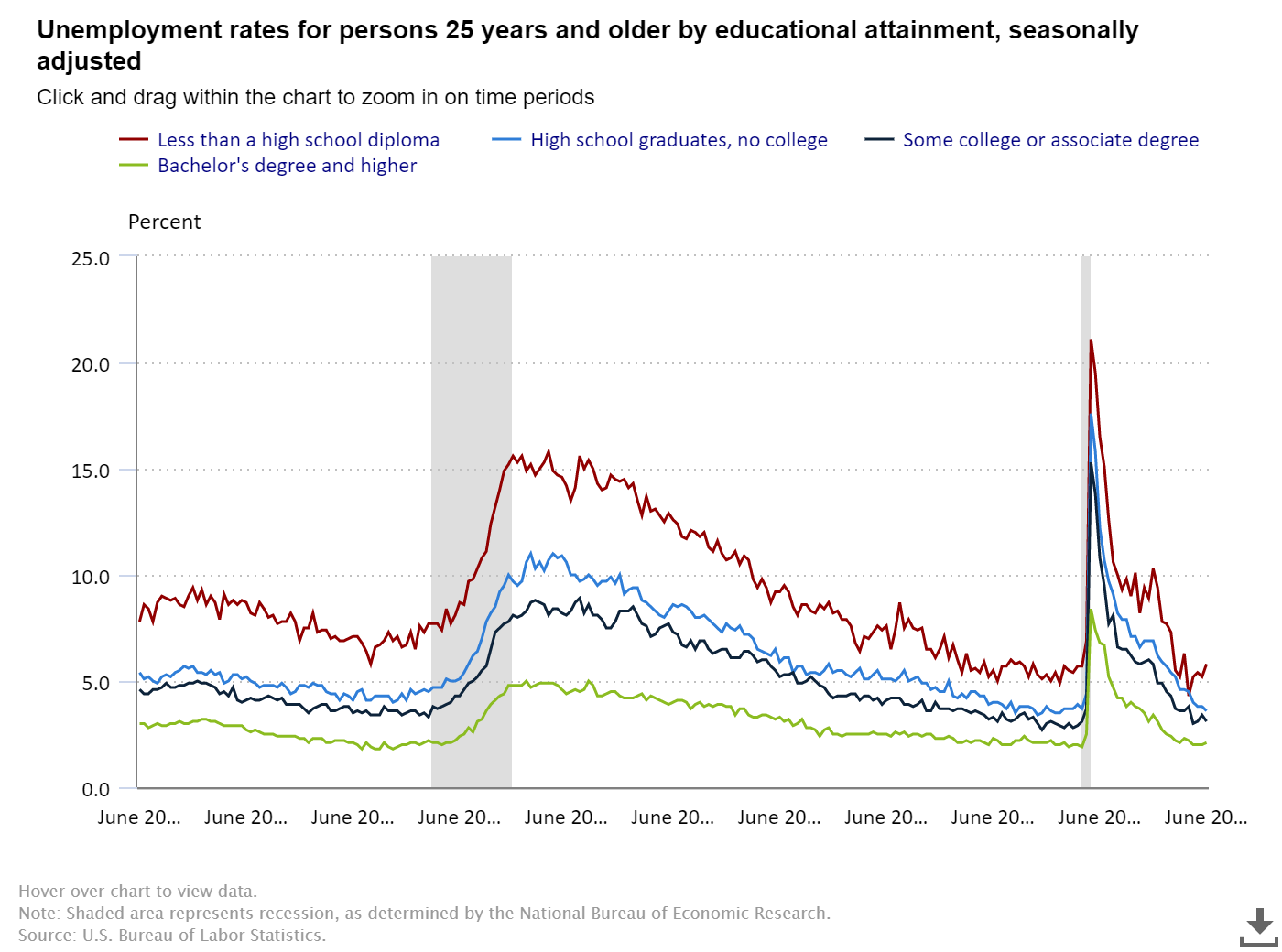

A tighter labor market is a good thing; this means people with less educational backgrounds can get employed as we have many jobs that don’t require a college education. The unemployment rate did tick up for those with less than a high school diploma in this report.

Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older:

—Less than a high school diploma: 5.8%.

—High school graduate and no college: 3.6%

—Some college or associate degree: 3.1%

—Bachelor’s degree and higher: 2.1%

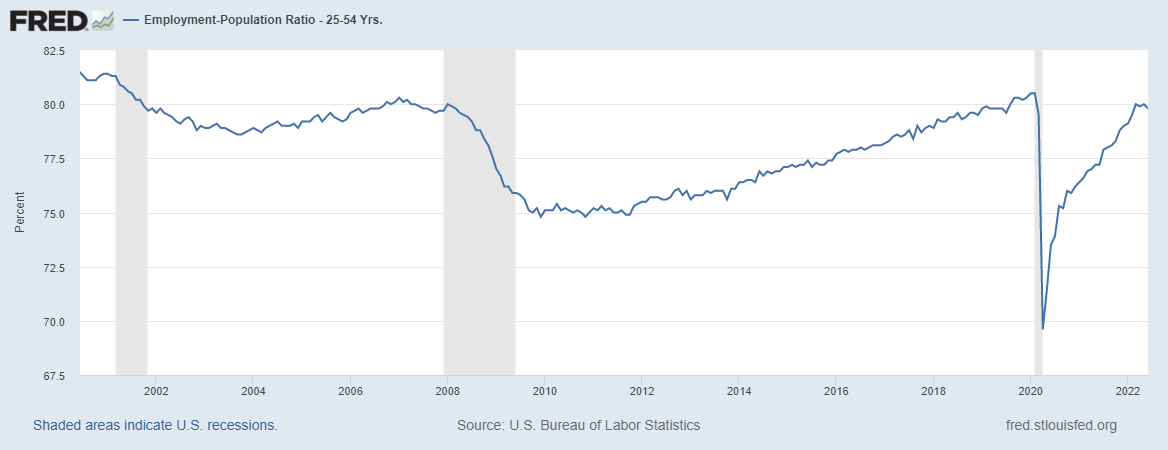

During a job recovery, the data line I love to track is the employment-to-population data for the prime-age workforce, ages 25-54. That’s the proper working-age workforce. The employment-to-population percentage did fall in this report. It’s currently at 79.8% and the pre-COVID-19 level was 80.5%. This is something I am keeping an eye on for the future. As an analyst, the rate of change of a trend is always crucial.

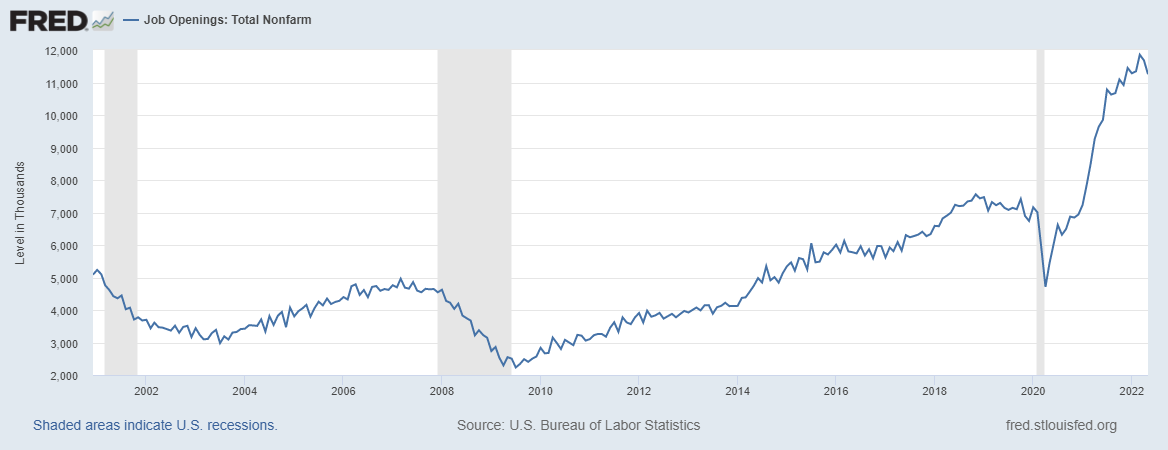

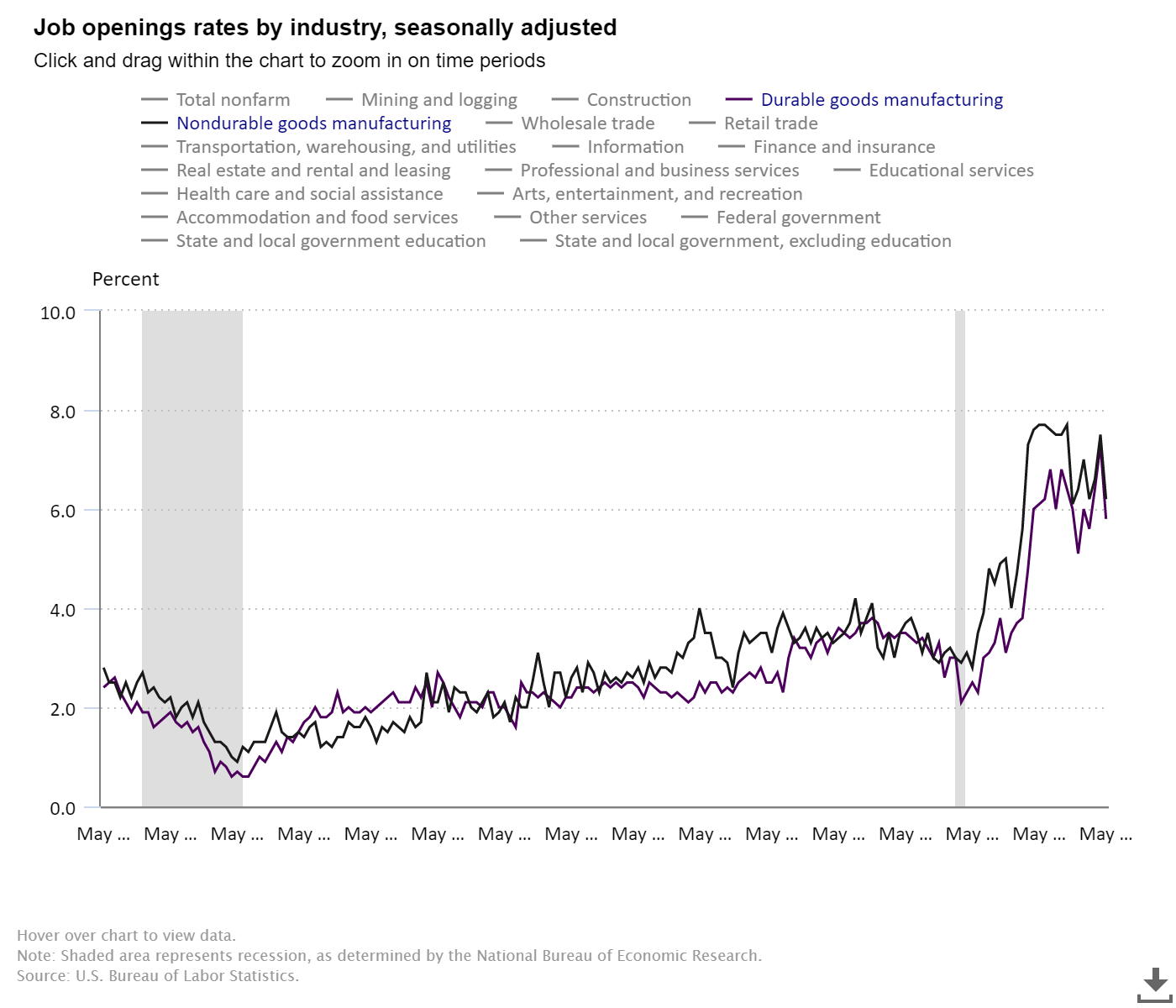

As the COVID-19 recovery got more robust, the internal labor market dynamics have been very positive for a while now, as we had a lot of job openings that needed to be filled. In fact, over a year ago, when we had a jobs report that missed estimates, I stressed early in this recovery that job openings would get to 10 million, which nobody, not even the people who work at the BLS, thought was possible.

Today, job openings are at 11.254 million, and this data line also had a noticeable decline. Remember, the rate of change is usually essential if it becomes a trend.

Total jobs data

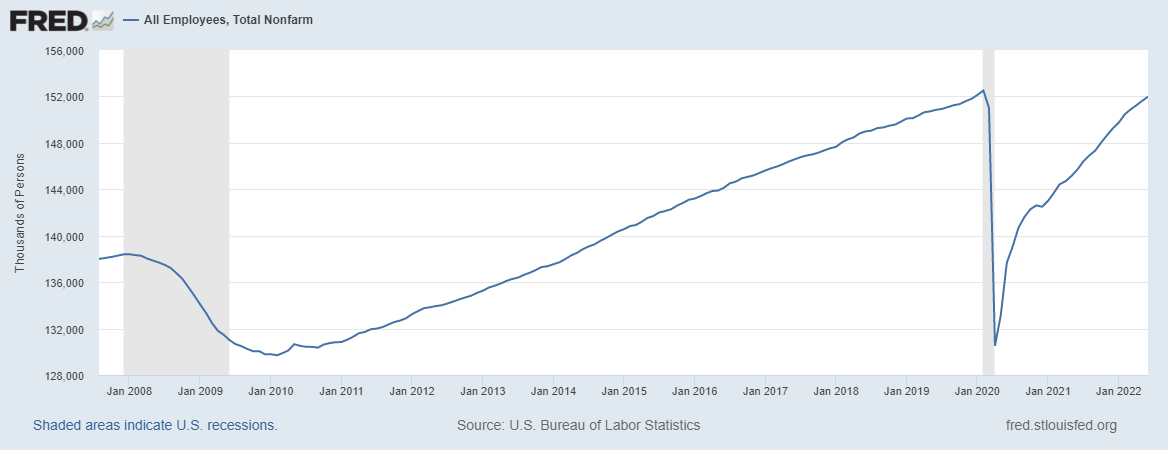

Even though I retired my America is Back Recovery model on Dec. 9, 2020, I knew getting all the jobs back that were lost to COVID-19 would take some time. Even though the recovery was the fastest ever, getting all the labor back from a global pandemic and having an aging society wasn’t as fast as some had hoped. However, I was confident we should get it all job back by September of 2022.

—Feb 2020: 152,504,000 jobs

—July 2022: 151,980,000 jobs

That leaves us with just 524,000 jobs left to make up over the next three months, which means we need to average adding 174,666 jobs per month. And the unemployment rate currently stands at 3.6%.

Looking at the jobs data and which sector added jobs in March, construction and manufacturing jobs came in positively, and we only lost jobs in the government.

Job openings in construction and manufacturing have picked up recently. Even though manufacturing job openings did slip in the last job openings data, it is still historically high. However, keep an eye out for the rate of change in labor data.

Recession red flag watch

Where are we in the economic cycle? Five of my six recession red flags are up, so until they are all up, I don’t use the word recession.

Let’s review them in order, as my model is based on an economic progression model, which isn’t the most exciting way to look at economics. However, economics done right should be boring. Here are the recession red flags:

1. The unemployment rate hits 4%. This is a progression red flag, meaning the economic expansion is more mature.

2. The Federal Reserve starts to raise rates. Another progression red flag; expansion is more mature.

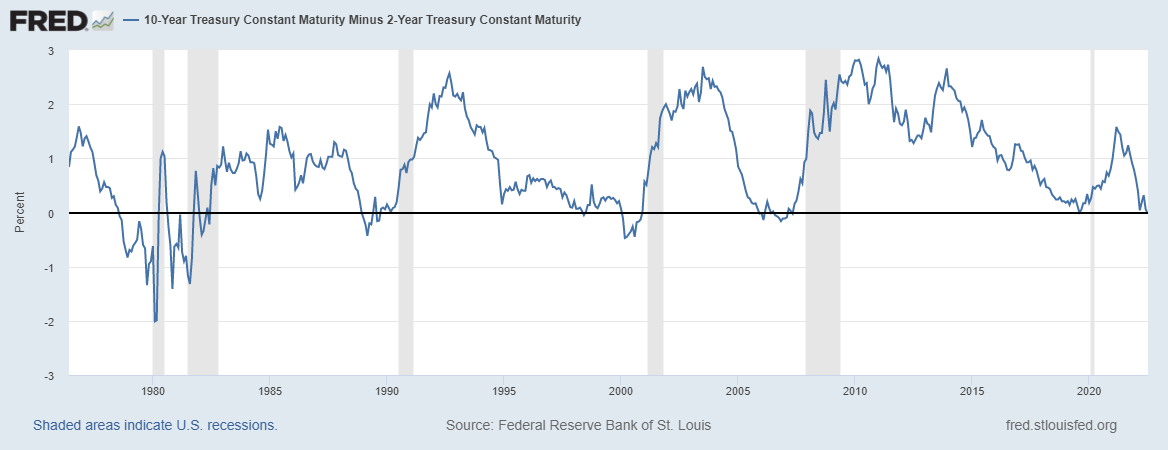

3. The inverted yield curve. This is more of a market-driven bond yield red flag. I had been on an inverted yield curve watch since Thanksgiving of 2021. This is when the two-year yield and 10-year yield slap high fives and say hi to each other. It’s another progression red flag, the more mature stage of the economy.

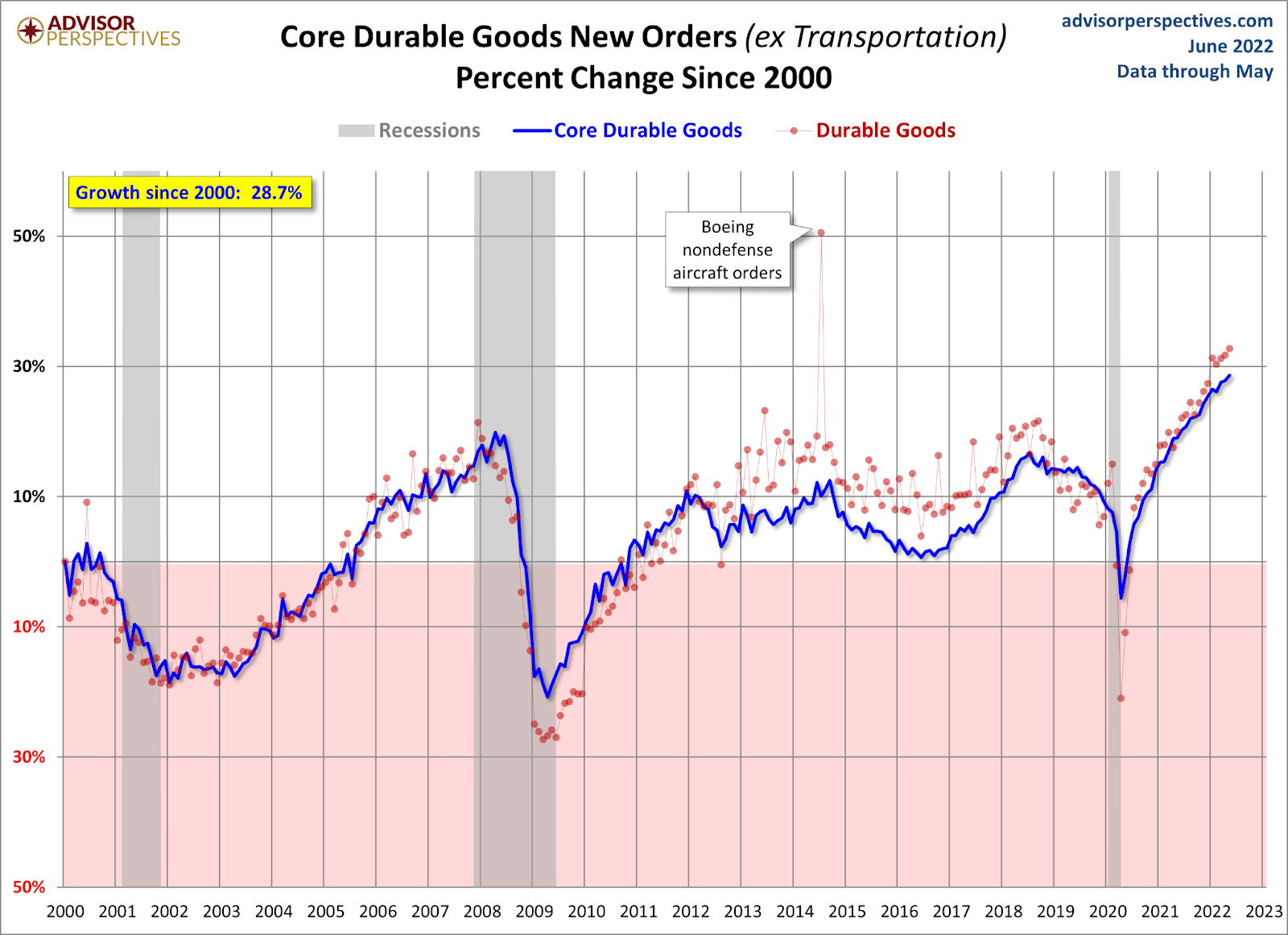

4. Find the overheating economic sector where demand can’t be sustained. Once that demand comes back to normal, people will be laid off. We see this in the durable goods data. A few companies are laying people off or putting into place a hiring freeze.

5. New home sales, housing starts, and permits fall into a recession. Once mortgage rates rise, the new home sales sector does get hit harder than the existing home sales market. The homebuilder confidence index is falling noticeably, and while we never had the housing build-up in credit and sales that we saw in 2005, the builders will slow housing production down with higher rates. I raised my fifth recession red flag in the month of June.

Builders Confidence Index:

The final recession red flag!

6. Leading economic index declines 4-6 months before a recession. Historically, the Leading Economic Index fades into every recession outside a one-time huge economic shock like COVID-19. So far, it’s been declining for two months, slowly. However, you can connect the dots on this in the future months if you know the components of this index.

As the economic cycle matures, we must look at the economy differently. I believe progression economic models are more valuable than screaming the word recession. I am a big believer in the rate-of-change data: even if the data looks solid historically, we need to be mindful of inflection points in each economic cycle. This is why since the summer of 2020 I talked about how the housing market can change once the 10-year yield breaks over 1.94%, meaning 4% plus mortgage rates.

Once all six recession red flags are up, my talking points will be different, but hopefully, this economic model is easy for you to understand: math, facts, and data. Never forget, you always want to be the detective, not the troll.

Update: This article was updated July 9 to reflect revised job numbers for February 2020 by the Bureau of Labor Statistics.