The years 2020-2024 will have the best housing market demographics ever recorded in U.S. history, with the lowest mortgage rates recorded in history. When you have these two titans acting in unison, it can potentially accelerate real home prices in an unhealthy way.

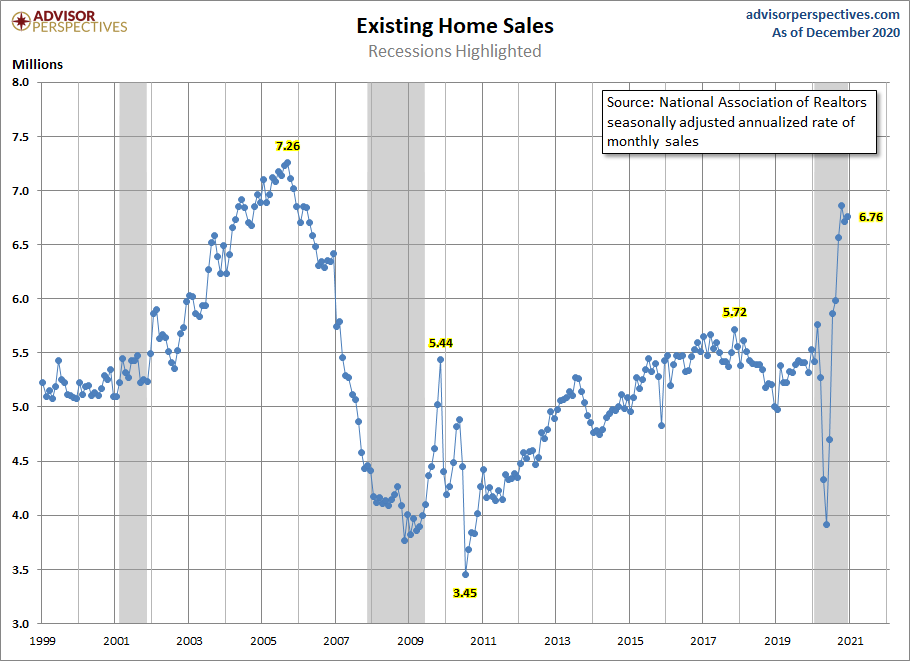

In 2020, the year of COVID-19, existing home sales ended at a respectable 5,640,000. That is roughly only 130,000 higher than the levels we saw in 2017. But sales should have ended the year more in the range of 5,710,000-5,840,000 if we stayed true to the trend line we had established by February 2020, before the COVID crash. We were and still are playing catch up to the lost demand during the COVID-19 shutdown period.

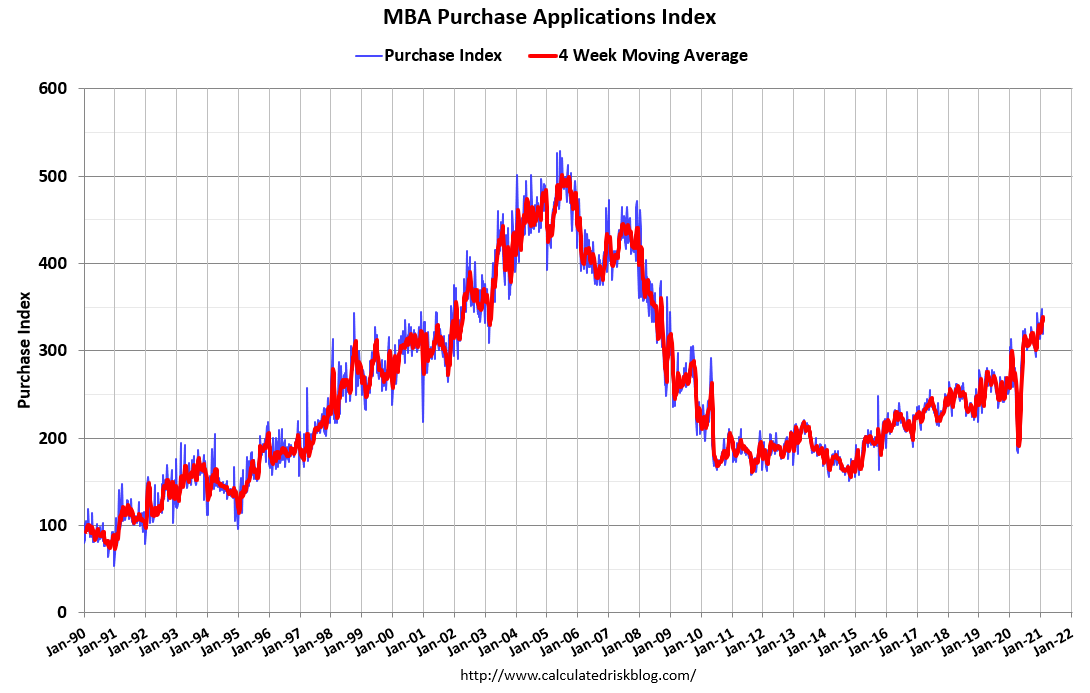

Purchase applications give a right direction trend 30-90 days ahead, and they are now averaging 12.8% year-over-year growth from last year. This is a tad better than I expected.

So far this year, the weekly Mortgage Bankers Association purchase application data compared to last year looks like this: +3%; +10%; +15%; +16%; +16%; +17%. That is still growing a bit better than the peak rate of growth I was looking for at 11% before March 18 arrived, and all economic data went haywire crazy on year-over-year comps.

The last existing home sales print came in at 6,760,000; we are about to get another report this coming Friday. We are not trending at this sales level today, and I expect sales to moderate more toward the 6.2 million level or lower. However, my fear for the years 2020-2024 is that the built-in demographic demand would cause real home prices to grow too fast. We are seeing the early stages of this take hold.

Because we still have reasonable lending standards, there are limits to how much sales can grow. This means in 2021, we will not see a catastrophic bad debt speculative boom in sales like we had in the bubble peak year of 2005, which had a tad over 7 million total existing-home sales. Today, the hotter-than-comfortable price gains are simply a function of supply and demand. Housing tenure from 1985-2007 was running at five years — now we are at 10 years.

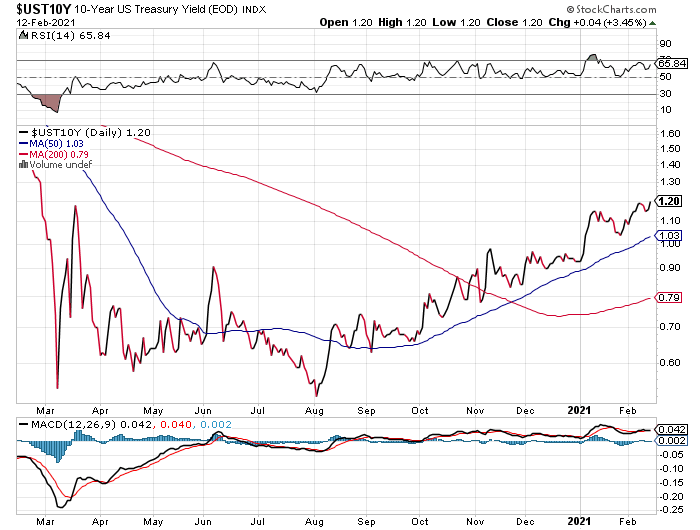

We have had periods of dislocated home-price growth in the previous expansion. In 2013, home prices were growing way too fast. Mortgage rates went higher, to over 4%, and quickly resolved the problem. When mortgage rates rose, demand declined, and inventory rose.

In 2014, purchase applications were down negative 20% year over year on trend, but home prices didn’t decline; they just cooled down from their torrid pace. In 2017, real home prices started kicking up again until increased mortgage rates of 4.75% to 5% caused real home price growth to go negative in 2019. I wrote that the negative real home price growth was very healthy for the housing market, even though nominal home prices didn’t decline again.

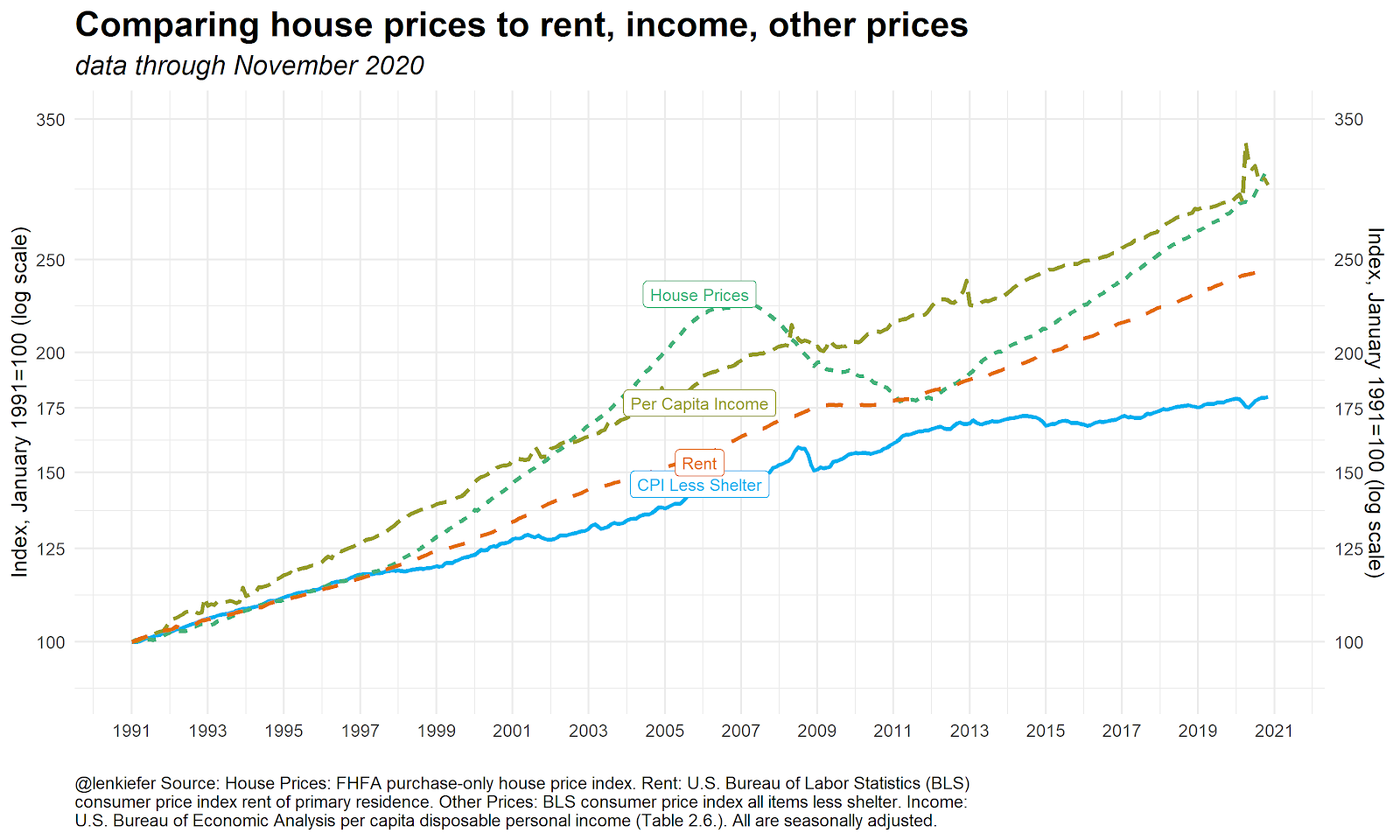

For 2021, we need to root for a repeat of what happened in 2013-2014 and 2018-2019. Home prices have caught up to per capita income, just like what we saw in 2002. However, mortgage rates are lower today, and demographics better. I feared this could be the case and it’s part of why I wrote the Chaos Theory for HousingWire back on Feb 3, 2020. I wrote that if COVID-19 hit us, stocks, the economy, and bond yields would fall, and this means mortgage rates would go down with it.

Mortgage rates are staying lower for a more extended period due to this one-time shock of COVID-19. These lower mortgage rates are running into the best housing demographics ever — see the chart below from the great Len Kiefer from Freddie Mac.

Hopefully, as we get closer to spring, we will get the expected traditional inventory rise, which will cool home price growth. If we do not see the typical seasonal boost in stock, then higher mortgage rates will be the only factor left to balance the market. The bond market is working its way higher, which should take rates higher with time.

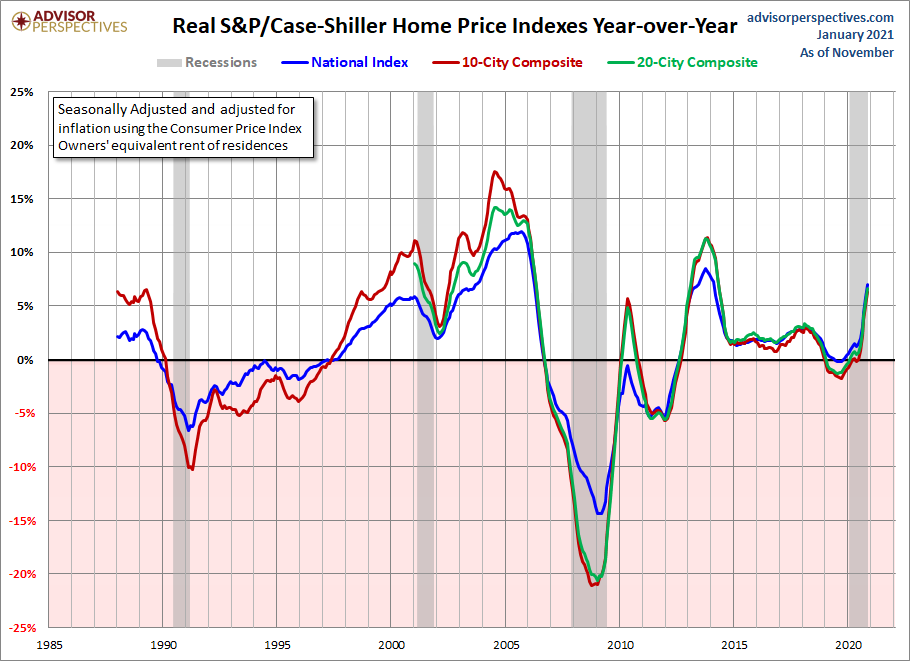

We need mortgage rates to rise to slow down rampant price growth. Once nominal home price growth goes above 4.6%, it is a bit too much for my taste, and we are at running at 9.5% per the S&P CoreLogic Case Shiller index, which is lagging current data now.

Three ideas are being floated to help the 2021 housing market are the home buyer tax credit, forbearance extension, and a possible write-down of $10,000 – $50,000 of student loan debt.

Considering what we know about the current housing market, I can confidently say that a homebuyer tax credit would just be adding fuel to the fire and not the best idea under the current housing market. We already have stable demand, low inventory, and price growth that is hotter than is healthy for the market. Why use government assistance to boost demand and pour gasoline on this fire? Or maybe you don’t think we have better ways to help housing?

The best economic sector in the world with rates this low doesn’t need government assistance.

A similar argument can be made against the student loan debt write down. There are some excellent reasons to write down student debt, but doing this to help the housing market isn’t one of them. It is utter nonsense to say that college-educated Americans who finish their education are so economically debilitated that they can’t buy homes. If this were the case, purchase applications would not be rising since 2014. I discussed this topic already and provided my plan for the student loan debt situation here.

Again, wouldn’t fiscal support be better spent elsewhere, like renter support, rather than throwing money at a sector that is already too hot?

With regards to forbearance, the FHFA recently granted another extension to their programs. Don’t expect the government to push people off forbearance this year. While I support extending forbearance until the job number get back to February 2020 levels, pre-COVID, we can’t count on the ending of forbearance to free up inventory in 2021.

The take-home message for housing in 2021 is that demand is stable, leading to unhealthy price growth – but not anywhere close to the extent that we saw in 2005. We don’t have a speculative home buyer market on bad structured debt loans. Home sales ended 2020 at 5,640,000, and purchase application data only recently broke past the index’s 300 level.

Per capita income and home prices have finally caught up with each other, but we don’t have speculation demand that could create a gap between home prices and per capita income like we saw in 2005. Demographics are better now, and mortgage rates are lower. But home price growth is an issue, and higher mortgage rates will be a good thing to cool this down.

We have a lot on our plate for the rest of the year – with JOB ONE being getting all Americans vaccinated so we can walk the earth freely again and have some fun! I’m already planning my next Las Vegas trip. It’s going to be epic.