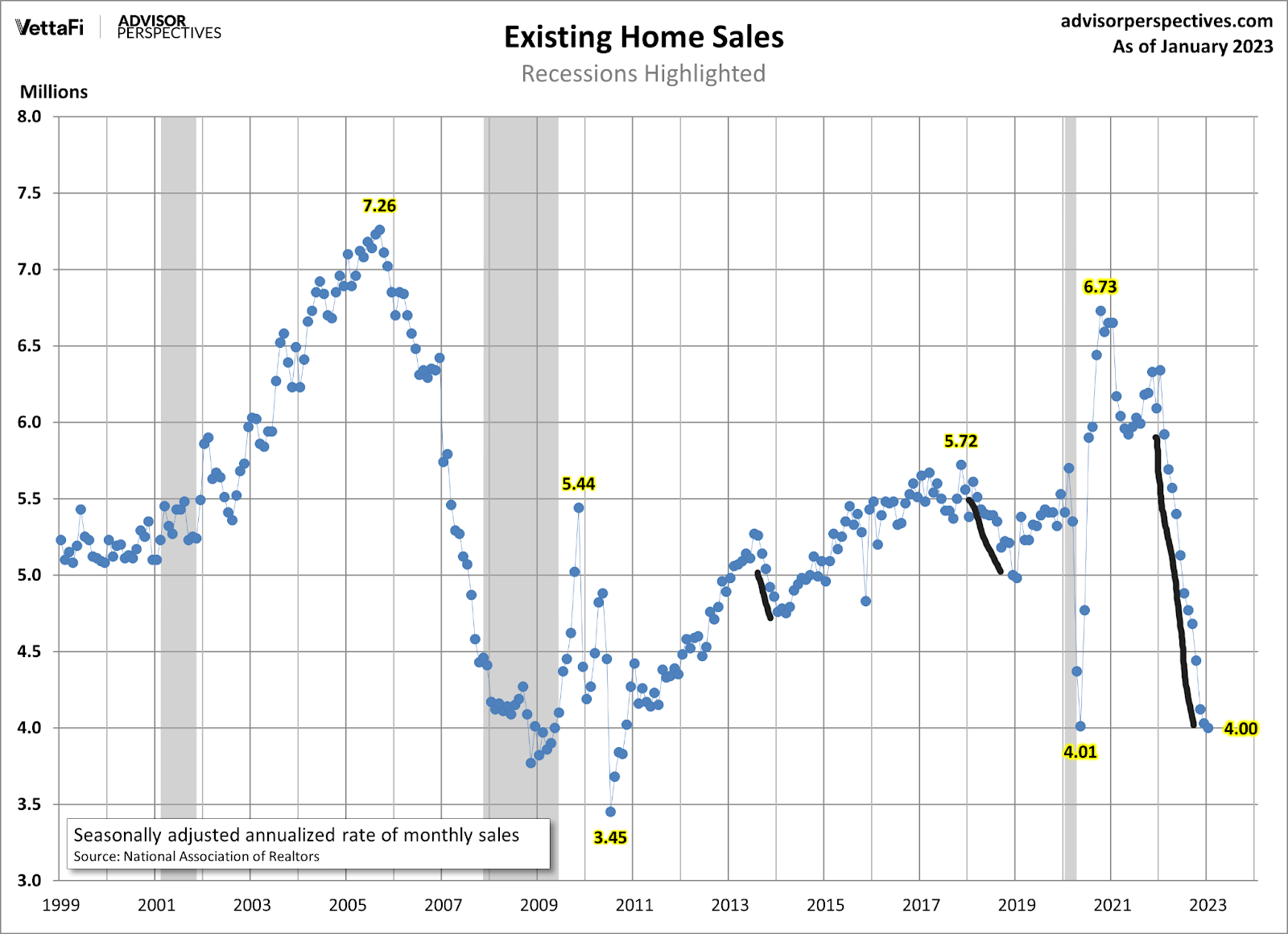

Last June, the Federal Reserve said it wanted a housing reset, which meant it wanted higher mortgage rates to destroy the housing market. This facilitated the biggest decline in existing home sales for a single year that we will ever see in modern-day history due to the high level of sales in January of 2022.

On Tuesday, the Federal Reserve achieved its primary goal; the days on the market are now above 30 days, which was the most important data line to get housing back to somewhat normal. Of course, this put the housing market into a recession on June 16, 2022.

I am a happy camper because last year, the housing market was savagely unhealthy with days on the market in the teens, and now we are back to a normal level over 30 days. We can’t have a functioning housing market with days on the market below 20 days.

Two terrible things could explain why the days on the market are below 20 days. No. 1, a massive credit housing bubble in demand, which will pop eventually. Of course, we don’t have that now. However, the second is that inventory is simply too low, with too many people chasing too few homes, which means too many bidding wars. We are not having bidding wars like we saw when the days on the market were below 20 days.

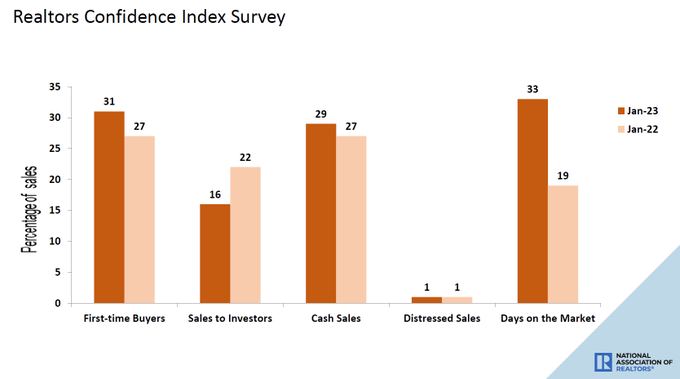

NAR Research: First-time buyers were responsible for 31% of sales in January; Individual investors purchased 16% of homes; All-cash sales accounted for 29% of transactions; Distressed sales represented 1% of sales; Properties typically remained on the market for 33 days.

My concern for 2020-2024 has been that inventory levels could break to all-time lows, which means even if sales were trending similar to the previous expansion, we simply have too many people chasing too few homes. The bidding wars you heard about this year weren’t because of record-breaking demand but because active listings are still near all-time lows. The total inventory today is still under 1 million at 980,000.

Inventory is higher this year than last, but I will jump for joy again if we can just hit 1.52 million. This would give the housing market a buffer in supply, just in case mortgage rates fall again. This didn’t happen this year, so we hear stories of bidding wars again early on in parts of the U.S. that don’t have inventory near 2019 levels.

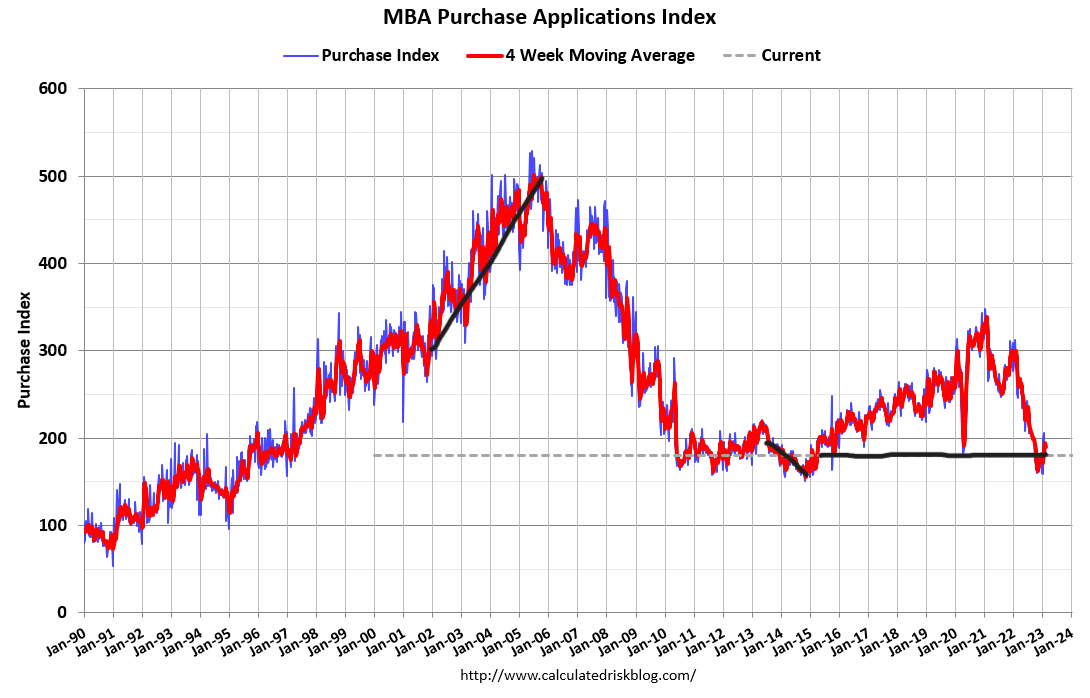

This is why last week on CNBC, I cautioned people to be mindful when discussing housing booming again. Forward-looking purchase apps have risen from a waterfall dive, and we have seen the data stabilize. We will bounce from this level, but context matters.

This is why we created the Housing Market Tracker: data moves very fast, and now that mortgage rates have spiked up again, we need to track to see how much damage higher rates do to demand.

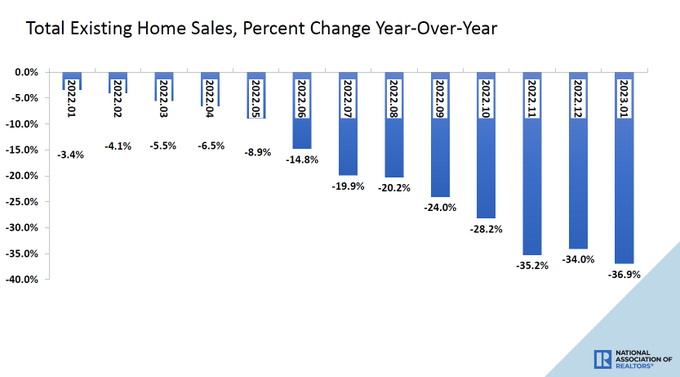

NAR: Total existing-home sales: completed transactions that include single-family homes, townhomes, condominiums and co-ops, slid 0.7% from December 2022 to a seasonally adjusted annual rate of 4.00 million in January. Year-over-year, sales retreated 36.9% (down from 6.34 million in January 2022).

“Home sales are bottoming out,” said NAR Chief Economist Lawrence Yun. “Prices vary depending on a market’s affordability, with lower-priced regions witnessing modest growth and more expensive regions experiencing declines.”

One of the forward-looking data line points I’ve discussed since Nov. 9 is that housing demand improved with purchase apps, so the worst sales declines are over. However, the sales data won’t show that improvement until February or March of this year, which means the January and February existing home sales reports.

Purchase application data is forward-looking 30-90 days, so it takes some time for better demand to hit the existing home sales report. However, it’s clear that the big major declines we saw in sales in the 2nd half of 2022 have settled down

Of course, this means we need to track forward-looking data, as higher mortgage rates should slow the housing market. The housing market can still be very frustrating to buyers and sellers because mortgage rates can move fast up or down. Since the end of June last year, when rates went above 6%, new listing data has declined, and this last week we hit a weekly new all-time low for the previous week.

- 2019 – 65,868

- 2020 – 62,447

- 2021 – 50,671

- 2022 – 49,159

- 2023 – 42,769

- This isn’t a good story for housing because a traditional seller is usually a traditional buyer. So, if people don’t list their homes to sell and buy, demand can collapse, as we saw in 2022.

As you can see below, the year-over-year declines are massive, but as the year progresses, the declines should get less if demand is stable from these levels, especially in the second half of 2023.

NAR Research: Year-over-year, sales retreated 36.9% (down from 6.34 million in January 2022).

Price growth has cooled considerably, especially in the second half of 2022. As someone who said we needed higher rates in February of 2021 and deemed the housing market savagely unhealthy in February 2022, this puts a smile on my face.

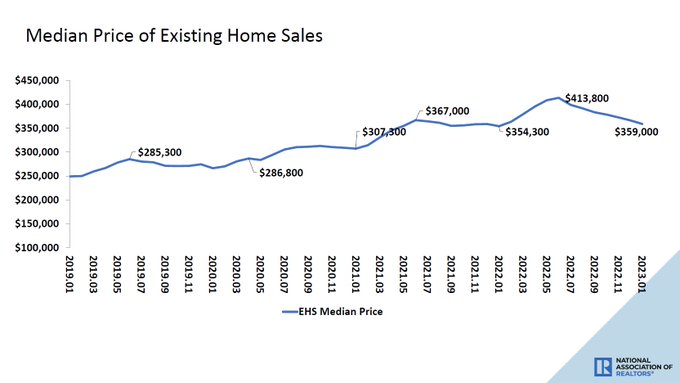

NAR Research: The median existing-home price for all housing types in January was $359,000, an increase of 1.3% from January 2022 ($354,300), as prices climbed in three out of four U.S. regions while falling in the West.

My fear since 2020 has always been that we would have major housing inflationary issues if inventory broke to all-time lows during 2020-2024. Of course, this happened, and then some, in the most destructive fashion ever.

My rule of thumb for 2020-2024 was that if home prices grew 23% during these 5 years, we would be ok with housing. This, of course, didn’t happen, as home prices grew 30% in just 2020-2021, and once rates rose in 2022 after the major housing inflation hit, demand just collapsed.

However, with that said, the one thing I wanted to see to get back to a boring and balanced market finally happened today: days on the market got over 30 days.

This is a huge step in getting back to normal, even though I know my forecast last June of just getting total housing inventory back to 2019 levels — which means just breaking over 1.52 million — looks bad now. However, one of the factors for this to occur was to have days on the market get above 30 days again. This is a positive step in the right direction.