Bank of America recently announced a loan for lower-income households that doesn’t require homebuyers to come up with a downpayment or closing costs, and doesn’t base the loan on a minimum FICO score. People’s first reaction was to wonder if this was 2008 all over again. Are we really doing those types of loans and promoting homeownership again without understanding the risks?

Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment. For sure, this Bank of America loan doesn’t have the exotic loan debt structures that caused so much pain during the housing crash years, but it’s good to understand what could happen.

First, to explain my logic here, I need to express what I believe housing is: “Housing is the cost of shelter to your capacity to own the debt. It’s not an investment.”

Part of our housing dilemma is this: How can you make something affordable when you promote it as someone’s best investment? Since many people think of housing as a wealth creator — and we want more Americans to have more wealth — then the government needs to make sure demand stays high enough for that wealth product to grow.

The entire system has to be designed to inflate the price over time. This is what we do in America. The housing market is very subsidized for demand to grow and whenever the economy gets weaker, rates fall and that impacts the housing market in a disproportionate way.

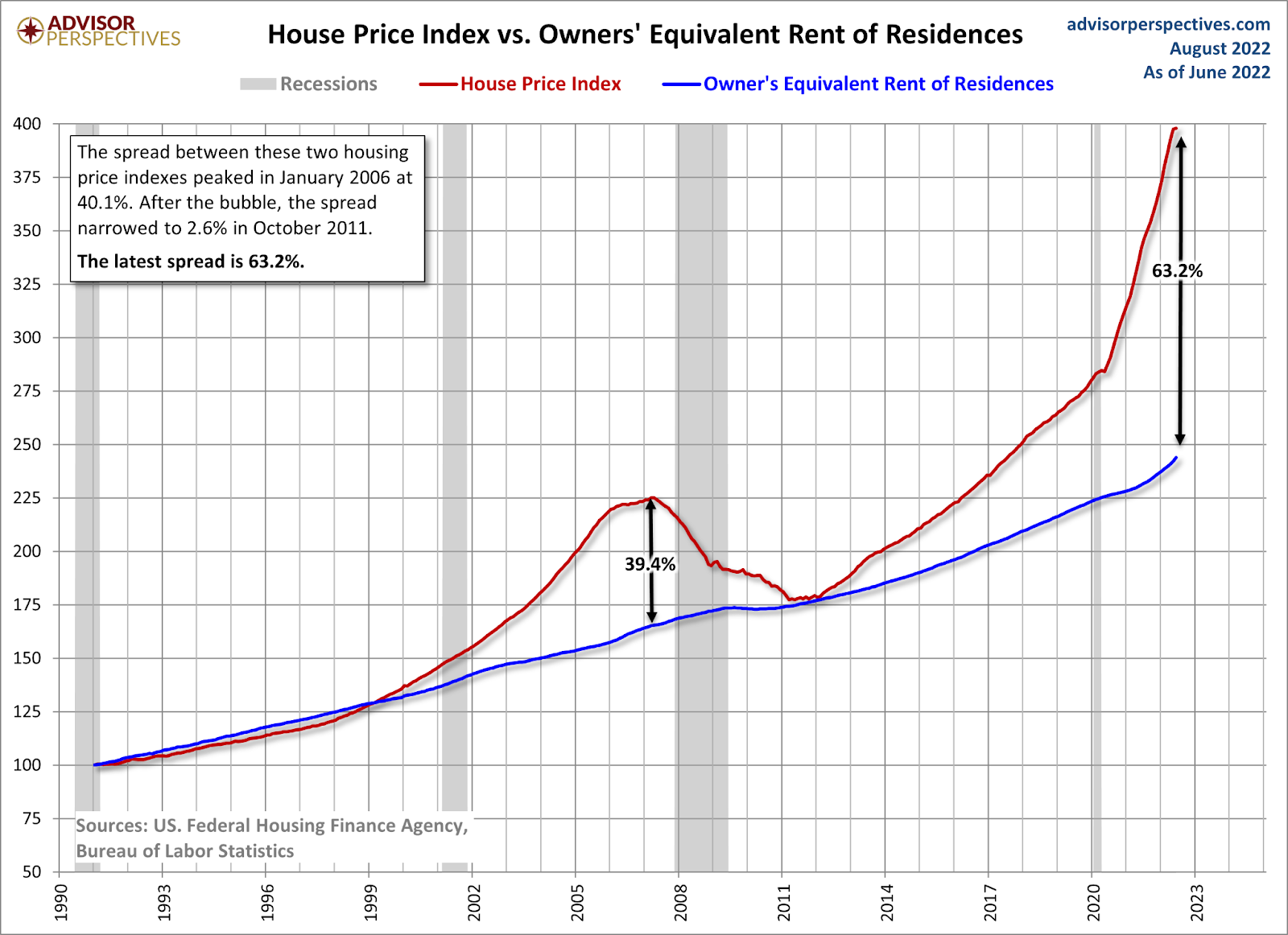

When mortgage rates fall, the majority of homebuyers (including homeowners who need to sell to buy another home) are mostly employed, so lower rates greatly benefit them, and housing demand increases. This can lead to home prices getting out of control, especially when total inventory gets to all-time lows. That is what has happened here in the U.S. We finally paid the price — pun intended — of not having enough product, with massive home price gains from 2020-2022.

The National Association of Realtors’ total Inventory data shows that historically we have between 2 to 2.5 million homes for sale, but in 2022 we got as low as 870,000 in total inventory. I always like to add that active listings were higher in the 1980s — and we have a lot more people now. So when you add move-up buyers, move-down buyers, first-time homebuyers, cash buyers and investors together, this can get out of hand.

We can see a clear deviation in home-price growth starting in 2020, when we broke to all-time lows in inventory. So if it seems like I was panicking about home-price growth and desperately wanted the inventory to grow, you can see my logic. By the summer and fall of 2020, I was basically into “danger, danger, Will Robinson” mode as inventory channels broke at the worst time possible for our country.

Now, we are talking about a housing reset, and the Federal Reserve is hiking rates with a tone that even implies they realize they can create a job loss recession! I just want emphasize this: the Federal Reserve is actively saying households are going to feel pain and some are making statements that they might not cut rates during a recession if inflation is high.

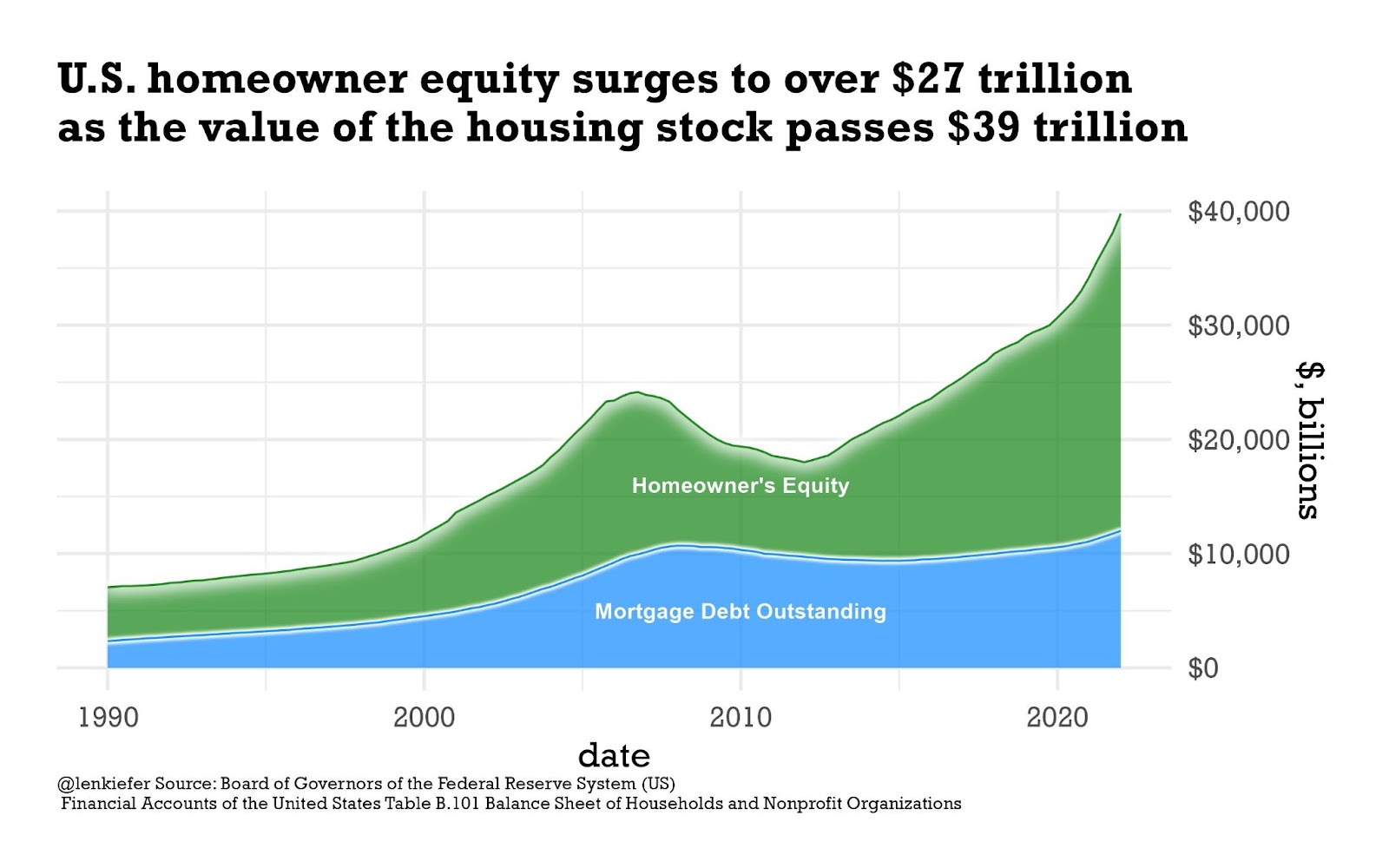

For the traditional homeowner who bought a home many years ago and has seen their nested equity position explode higher, this isn’t much of an issue. If they lost their job, they have a lot of equity in their home, and most likely their financials have gotten better over time.

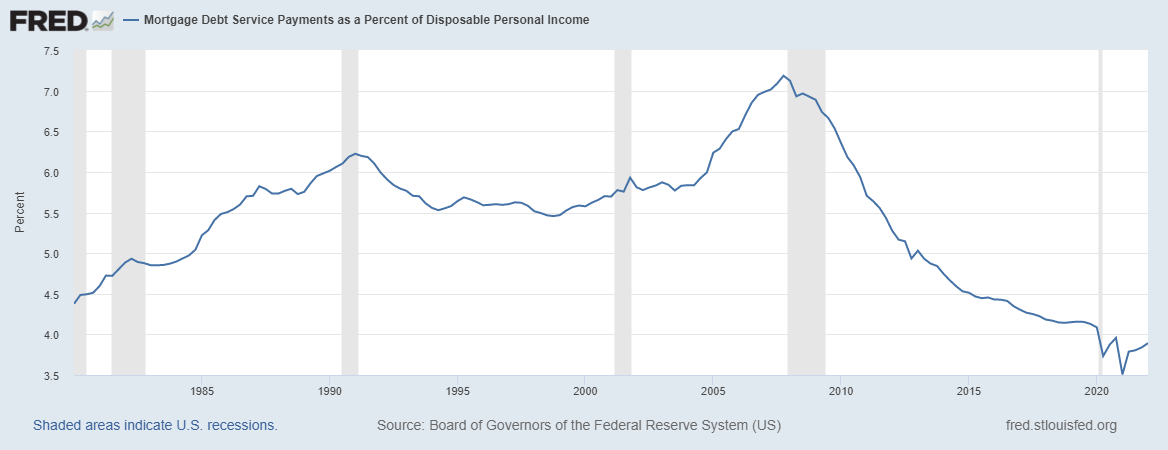

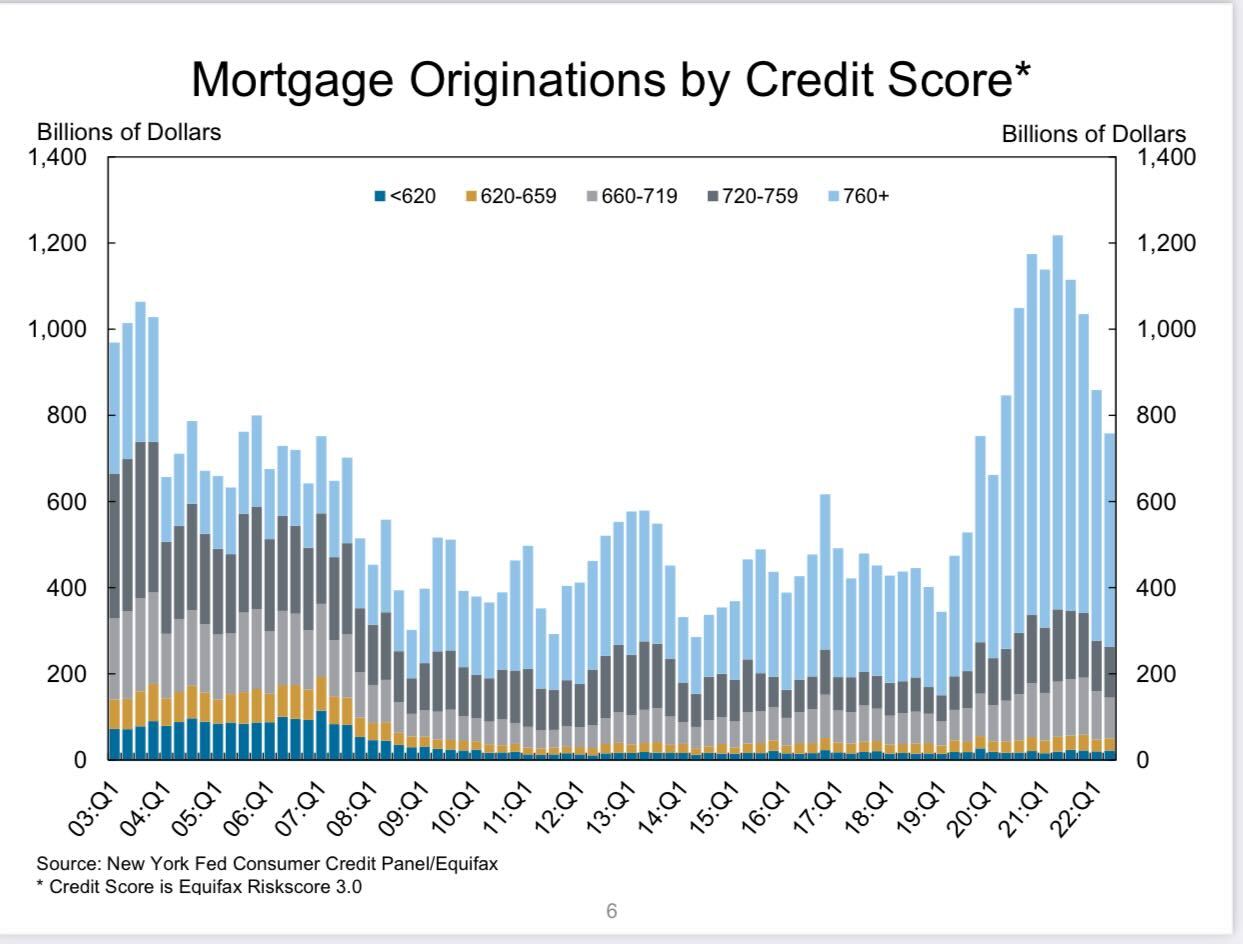

This is a plus of homeownership, a fixed long-term debt cost while their wages rise every year. As you can see below, we haven’t had the mortgage credit boom like we saw during the housing bubble years. So, not only do we have 40% plus of homes with no mortgage, the nested equity homeowners have now is almost unfair. Remember, the system is designed to keep home prices inflated.

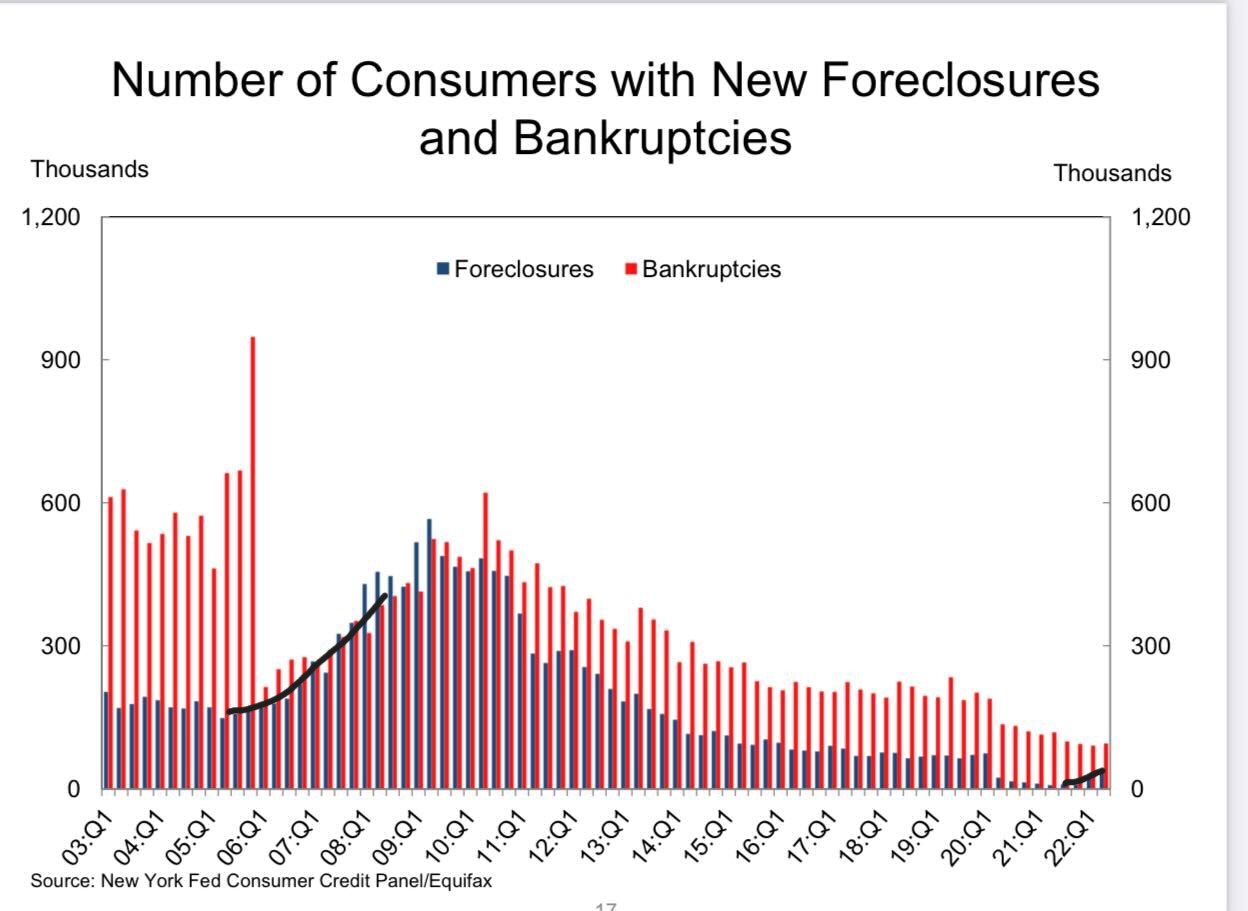

I always stress how crucial it was to have the 2005 bankruptcy reform laws and the 2010 qualified mortgage laws, which together have allowed homeowners to have the best financial profiles in our country’s history. When we look at the credit data over the past 10 years, it looks nothing like the stress we saw from 2003-2008, which was an economic expansion and jobs being created before the job loss recession in 2008.

Homeowners buy a home, have a fixed payment, and over the life of the loan, as their wages grow, their cash flow gets better.

FICO scores look a lot better now than in the run up to the great financial crisis. So you can see the benefit of having a fixed payment shelter cost, while your wages rise. We don’t have any more 100% loans that have significant recast rate risk, so that the total payment of the home can force someone to sell, even if two people are working full time and haven’t lost their jobs. We have a much better housing ecosystem now for sure.

With that all said, the concern I have with Bank of America’s no-down loan will be the concern I always have with late-cycle lending in any economic expansion. If we are going to provide 100% financing with no closing costs and the Federal Reserve is talking about the need for a recession, then I believe we need to make sure people realize the risk of this type of loan. I have to make this statement because all six of my recession flags are up.

Suppose all parties understand the risk of the Bank of America 100% loan and other low downpayment loans at the same time the Federal Reserve is trying to increase the unemployment rate. In that case, nobody can be blamed for the product — whether they are the ones offering the loan or the ones taking it.

In theory, you should never lose your home unless you lose a job or you experience a financial emergency. Your home is where you raise your family and that mortgage payment you make each month should make you sleep easy every night.

However, no matter how sound the loan is, we can’t close our eyes to the economic cycle risk, especially when we have Federal Reserve officials talking about the need to have unemployment rates going up to help combat inflation.