The 10-year yield closed today above my key level of 4.25%: Does that mean mortgage rates will hit 8%? To understand what’s happening, here’s how I look at the bond market and mortgage rates in my forecast for 2023.

In my 2023 forecast, the range on the 10-year yield was between 3.21%-4.25%, emphasizing that the bond yields can go lower than 3.21% only if the labor market breaks — which would require jobless claims to go over 323,000 on a four-week moving average.

That 10-year yield channel equates to 5.75%- 7.25% mortgage rates. And since the labor market isn’t breaking and the economy is doing well, mortgage rates are at the higher end of my range for this year. In fact, mortgage rates today were as high as they have been since December of 2000.

The big surprise in 2023 has been that the spreads with mortgage rates got worse, not better — all due to the banking crisis.

As you can see in the chart below, spreads were getting better, then the banking crisis hit and they got worse. This new variable is our 2023 reality until the Federal Reserve cries uncle.

Now let’s look at the 10-year yield: We closed today at 4.28%. For intraday action, I wanted to see if we could reach the highest level of last year at 4.34%. We didn’t, and in fact, yields headed lower toward the end of the day from the high peaks. For now, keep an eye out for that 4.34% level because breaking above that could cause more short-term bond selling.

As we can see below with a longer timeline chart, the 10-year yield has stayed in my range this year for 99.9% of the time. Considering where the economic data has been recently, it makes sense that we are at the higher end of the range because there is no recession in the data lines currently.

The critical time was early this year when it looked like the bond market wanted to go lower due to the banking crisis, but my Gandalf line (the red line below) held. I believe as long as the economy isn’t breaking, the 10-year yield shouldn’t go under 3.37% — and the chart below shows that line has held up eight times.

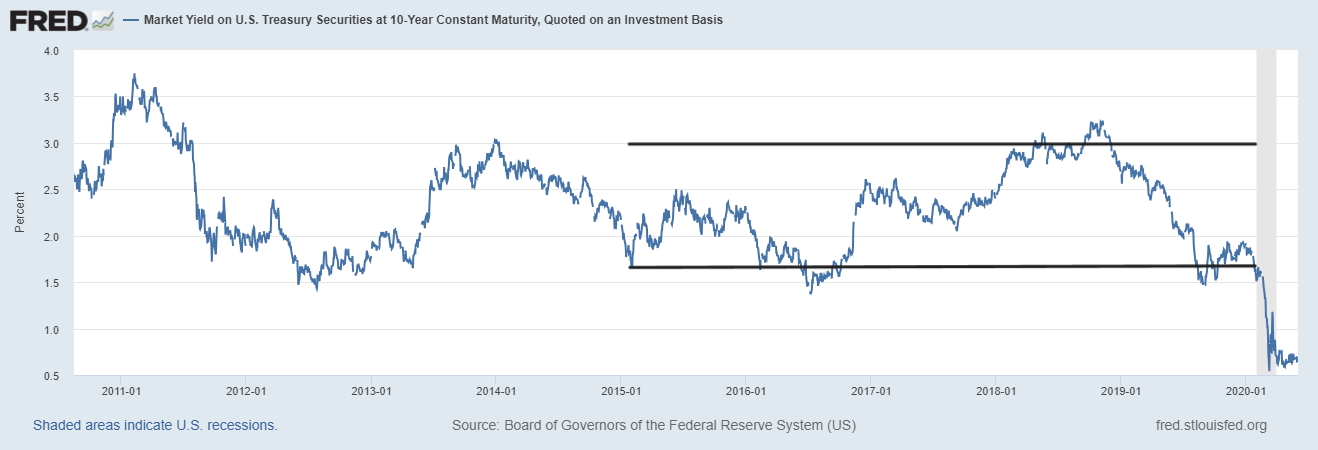

I started forecasting 10-year yield ranges and mortgage rates in the previous expansion: It was a very boring channel. Every year starting from 2015, it was the same forecast; the 10-year yield would be between 1.60%-3% which meant mortgage rates between 3.50%-4.75%, roughly.

As the chart below shows, before the COVID-19 recession, bond yields mostly stayed in that range, although there were times between 2015-2020 when they broke below 1.60% and over 3%. Currently, we are slightly above 4.25%.

When COVID-19 hit, I had a 10-year yield range for the recession at -0.21%-0.62. My COVID-19 recovery model began on April 7, 2020, as the 10-year yield was above 0.62% on that day.

In 2021, even though I was calling for higher mortgage rates because home prices could explode higher, the 10-year yield forecast was 0.62%-1.94% with an emphasis on creating a range between 1.33%-1.60%. That happened and we spent a good amount of time there in 2021.

In 2022, my 10-year yield call peaked at 1.94%, but I said that if global bond yields rose, we could hit 2.42%. March of 2022 brought a Fed pivot and the Russian invasion of Ukraine and we were off to the races with bond yields getting as high as 4.33% intraday in 2022.

So will mortgage rates go to 8%?

The inflation growth rate has been falling, but my bond yields range for 2023 was based on the economic data staying firm, meaning if economic data gets better, yields should be at the higher end. This week’s economics data, retail sales, and industrial production data beat estimates and the Atlanta GDP data is at 5.8%. The economic data hasn’t just stayed firm — it’s gotten better so bond yields are now above the range.

We also have to consider the Federal Reserve. The Fed now believes its policy is restrictive, which wasn’t case last year, so this is a reason why they’re not talking about more aggressive rate hikes.

How much higher can bond yields and mortgage rates go before the Fed starts talking about it? Hopefully, this chart below gives you an idea, because if the inflation growth rate cools even more, the Fed might step in to cut rates or stop their balance sheet reduction, which is another form of tightening policy.

So, can mortgage rates hit 8%?

Yes, they can, but it would require the economic data to stay firm. Short-term, as long as the economy outperforms, 8% is in the works. However, you can see the limits of mortgage rates now because the Federal Reserve has told us they believe their policy stance is restrictive. They don’t want to push the lever too much because one of their goals is to keep the Fed funds rate higher for longer.

The one thing that can change the Fed’s mindset is the labor market breaking, but for now they don’t have to worry about that.