As the nation ages and the demographics within the ranks of older Americans begin to shift, today’s seniors are increasingly open to the idea of carrying debt.

Almost half of retirees aged 75 and over had some kind of loan debt in 2016, according to an analysis from the Employee Benefit Research Institute (EBRI) — an increase of nearly 60% from 2007, when that figure sat at 31.2%.

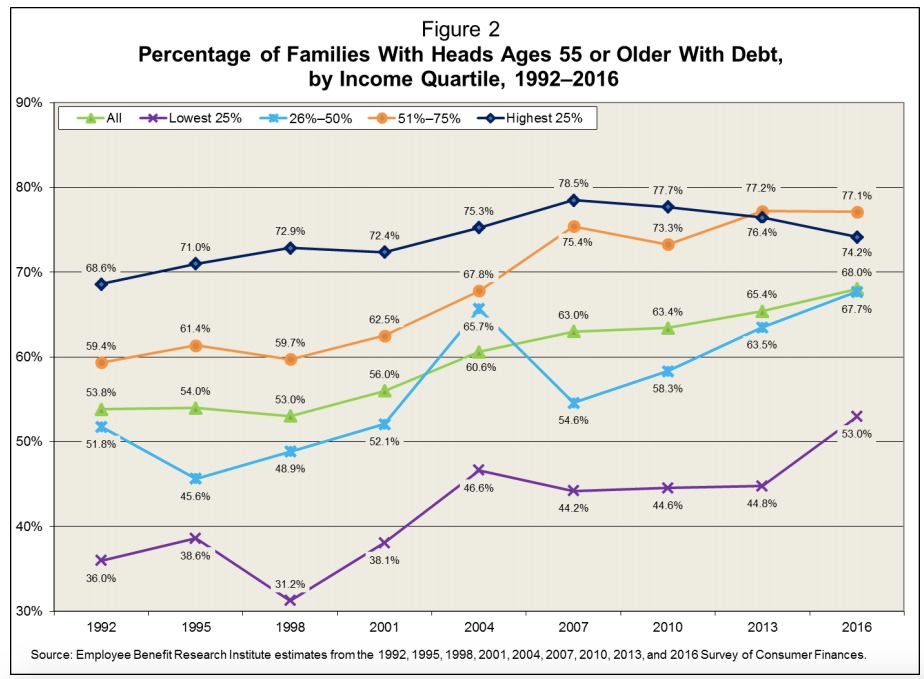

“While improving in many respects in the most recent years, the overall trends in debt are troubling as far as retirement preparedness is concerned, in that American families just reaching retirement or those newly retired are more likely to have debt — and higher levels of debt — than past generations, specifically those in the 1990s,” EBRI senior research associate Craig Copeland wrote in a summary of the findings.

Reverse mortgage professionals have long identified a perception gap between older, “Greatest Generation” seniors and their younger baby-boom counterparts. Among the older cohort, mortgages are traditionally seen as a means to an end that must be paid off as soon as possible, while boomers are generally more open to the idea of using debt to upgrade their existing properties — for instance, through the use of traditional home equity lines of credit — or to purchase a larger dream home in retirement.

But EBRI’s analysis — which uses data from the Federal Reserve’s Survey of Consumer Finances (SCF) — reveals a substantial rise in the proportion of older Americans with debt. For instance, among households headed by someone aged 55 and older, 68% had some kind of debt in 2016. In 1992, that number stood at just 53.8%.

So while Americans aged 75 and older remain the least likely of all demographics to have any kind of debt, they represent the fastest-growing cohort in terms of debt over the last 25 years.

The Washington, D.C.-based non-profit typically assesses retirees’ attitudes toward savings and long-term costs, but Copeland notes that debt can often serve as a significant strain on an older family’s retirement finances.

“Any debt that an elderly or near-elderly family may have accrued entering or during retirement can offset any asset accumulations, resulting in lower levels of retirement income security,” he wrote.

The effect is particularly strong for Americans in the lowest income quartile, who have the highest debt load in relation to their overall income. The lowest 25% have debts that equate to 16.4% of their income, while the highest 25% pay the equivalent of 6.2% of their incomes.

But no matter the income level, Copeland warned that the increasing prevalence of debt among older Americans poses a significant problem for the incoming generation of retirees.

“More families that have elderly heads are placing themselves at risk of running short of money in retirement due to their increased likelihood of holding debt while in retirement,” Copeland concluded.

Written by Alex Spanko

{kind=link}