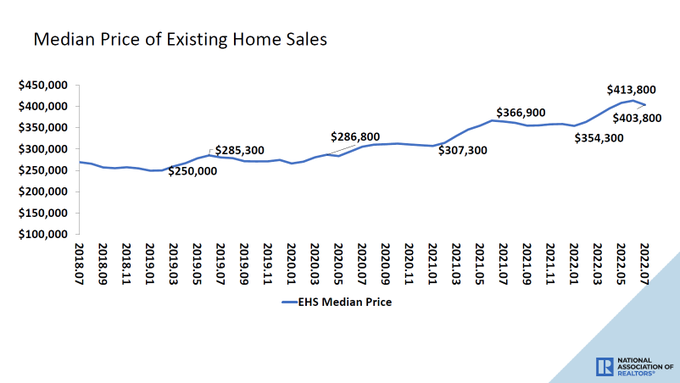

Today the National Association of Realtors reported that the trend of declining existing home sales, which we have seen since mortgage rates rose, is getting worse. But that isn’t the worst part of the data line! The shocking stat (for some, not for me) is that even with the significant decline in sales since January of 2022, the median sales price is up 10.8% year over year. The savagely unhealthy housing market continues — a function of starting the year at all-time lows in inventory.

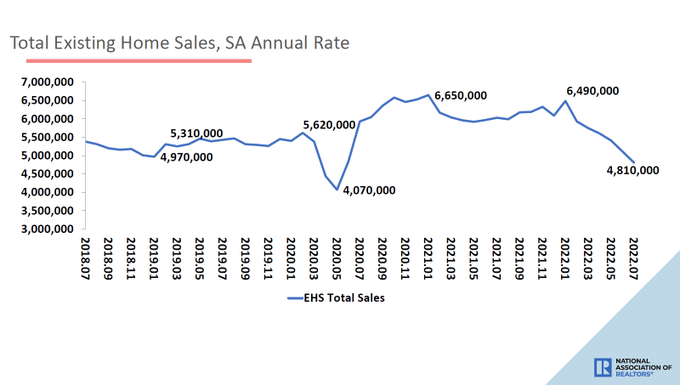

From NAR: Total existing-home sales slipped 5.9% from June to a seasonally adjusted annual rate of 4.81 million in July.

I was concerned about 2022 home-price growth because by October of 2021, I knew we would start 2022 at all-time lows in inventory, which can create forced bidding action. I am not a fan of forced bidding action under any circumstances, but when it’s due to a raw shortage of homes and not a credit boom, as we saw from 2002-2005, it’s even worse.

NAR: The median existing-home price for all housing types in June was $403,800, up 10.8% from July 2021 ($364,600), as prices increased in all regions. This marks 125 consecutive months of year-over-year increases, the longest-running streak on record.

On the good news, inventory is rising, which is a positive. The parts of the country where inventory levels are at peak-2019 levels or higher are officially off the savagely unhealthy market list because they have plenty of inventory to have a more functional housing market. However, as a nation, we aren’t there yet.

NAR: The inventory of unsold existing homes rose to 1.31 million by the end of July, or the equivalent of 3.3 months at the current monthly sales pace.

My rule of thumb is that I will take the savagely unhealthy housing market theme off once we can touch 2019 peak levels of 1.93 million homes for sale and have at least four months of supply, which would mean a balanced housing market in my book. I am looking for a range of 1.52-1.93 million, something I have talked about for some time post-COVID-19. Because inventory is very seasonal — it falls in the fall and winter and then rises in the spring and summer — it’s not going to happen in 2022, but hopefully, we can get there next year.

NAR lists total current inventory at 1.31 million. Historically we are between 2-2.5 million. The peak in 2007 was roughly 4 million.

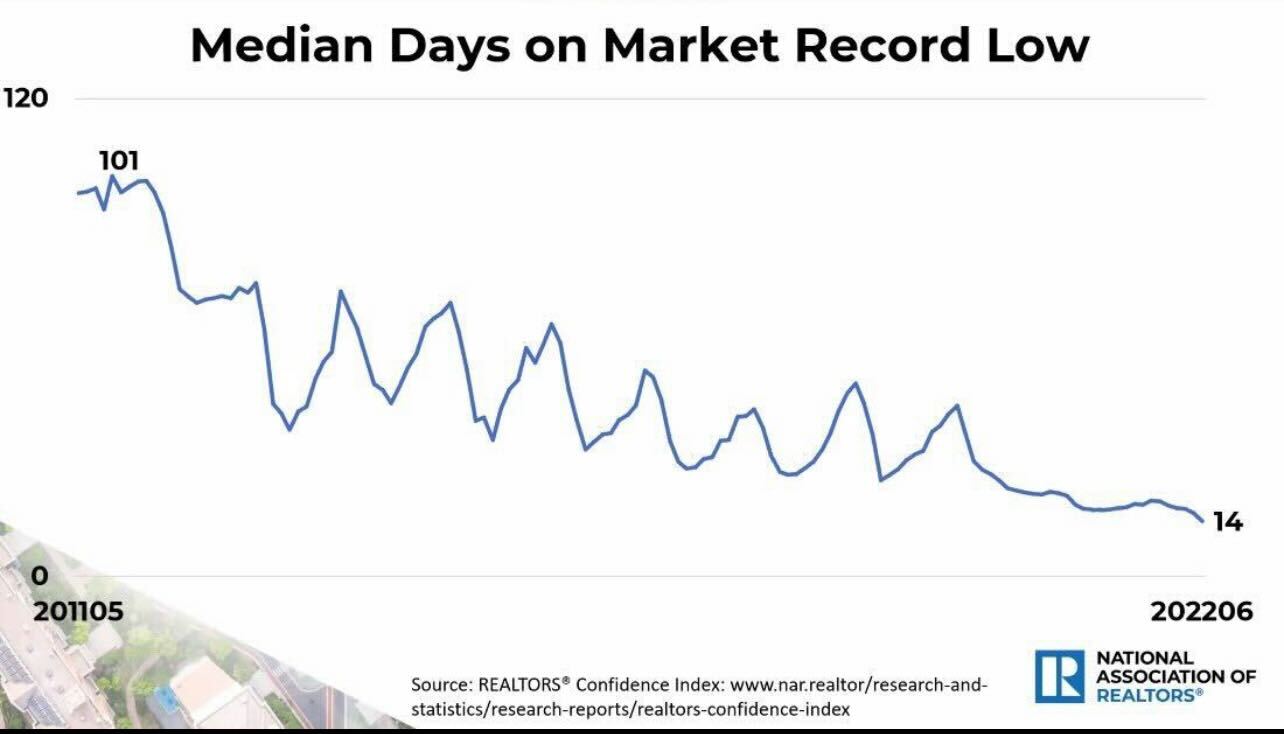

One of the most painful data lines to watch over the last two months has been the median days on the market, which have now broken to all-time lows. In a regular housing market, we are over 30 days, which is why I want the total inventory to get back to 2019 levels to have more balance nationally.

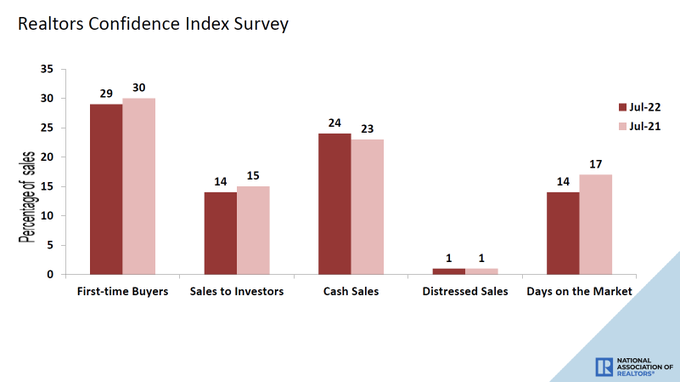

NAR: First-time buyers were responsible for 29% of sales in June; Individual investors purchased 14% of homes; All-cash sales accounted for 24% of transactions; Distressed sales represented approximately 1% of sales; Properties typically remained on the market for 14 days.

To give you some historical perspective here, you can see why I am using the term savagely unhealthy, as the median days on the market have never been lower in history.

Higher days on market mean choices for buyers and sellers. We never focus on the seller aspect because it’s easy to forget that a traditional primary recent home seller is also a buyer. Now that rates are up a lot, some sellers can’t afford to move or have delayed moving.

However, this is a good thing for others that need to move, as it means more inventory and more choices. This is one of the reasons I haven’t been the biggest fan of the housing market in recent years: we lacked options and time for people to have a more traditional home-buying and selling process. Over 30 days is preferable; anything that is a teenager isn’t a good thing at all.

This year, we saw that housing acted poorly when mortgage rates exceeded 6%. Of course, we have seen a 1% move lower and a lot of back-and-forth action on rates daily. If mortgage rates can head toward 4% again, the market should act better. However, until then, the market is still dealing with the affordability shock to demand as rates jumped massively this year. This, on top of the 44% + home-price growth since 2020, is a meaningful hit on affordability.

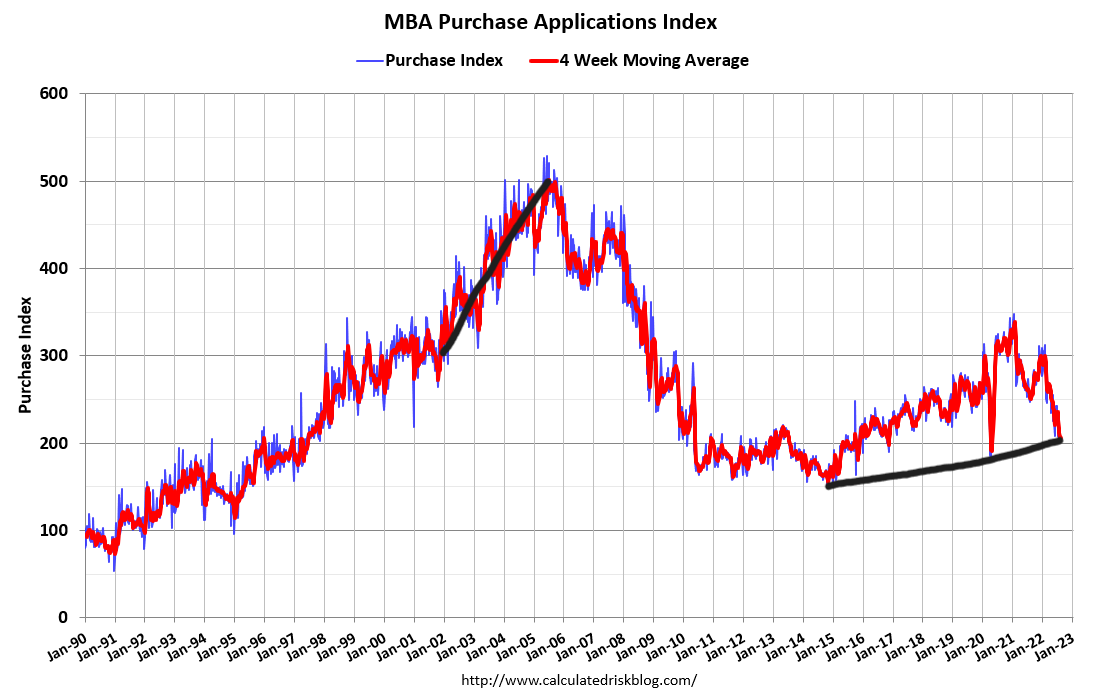

Purchase application data was down 1% weekly and down 18% year over year. The four-week moving average is down 17.75%. I had anticipated four-week moving average declines of 18%-22% once mortgage rates got above 4%. That didn’t happen, but rates above 5% did the trick.

We will soon enter a time where the year-over-year comps will be more challenging because we will have a higher bar to work from. Last year starting in October, mortgage demand started to pick up noticeably and pushed the existing home sales data toward 6.49 million at the start of this year. Some of the year-over-year data can look weaker than the 18% decline trend we have recently just due to higher comps.

Today’s existing home sales report isn’t the best due to home-price growth still being in the double digits. We should see less price growth in the upcoming months. However, this year, even with the big hit on demand and the housing market recession, we are still seeing unhealthy home price growth. I talked about this recently on CNBC.

We still have home prices growing faster this year than what we saw in the previous decade, and this has to do with the fact that we started the year at all-time lows in inventory, and we are working our way back to normal. Remember, normal inventory levels is a good thing, not a bad thing, because we all want a B&B housing market — boring and balanced — not savagely unhealthy.

We’re covering this important topic at our HousingWire Annual event Oct. 3-5 where Logan is a featured speaker. Register here to join us in Scottsdale, Arizona.

Logan

Your insights are excellent

Your A Rock Star

Robert A