In Tuesday’s new home sales report from the Census Bureau, monthly supply hit recent highs at 6.2 months and 5.9 months on the more critical three-month average.

I focus on the monthly supply as being the most critical data for the new-home market. The new home sales market is a small but essential part of the overall market and the economy. I have long said that the builders don’t build for the existing home sales market; they build based on demand for their specific products. When the monthly supply of new homes grows, builders will throttle back construction to control the flow of products in order to protect their margins.

From the Census report: The seasonally adjusted estimate of new houses for sale at the end of July was 367,000. This represents a supply of 6.2 months at the current sales rate.

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months, and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is an ok market for the builders. They will build as long as new home sales are growing.

- When supply is 6.5 months and above, the builders will pull back on construction.

Inventory levels for new homes are near the higher end of the range of the previous expansion. New home sales and housing starts in the last expansion were at the lowest levels ever, but had a slow but steady rise during the longest economic expansion ever recorded in U.S. history. We had a pause in 2018 when mortgage rates got to 5%, but the supply data got better quickly as mortgage rates went lower.

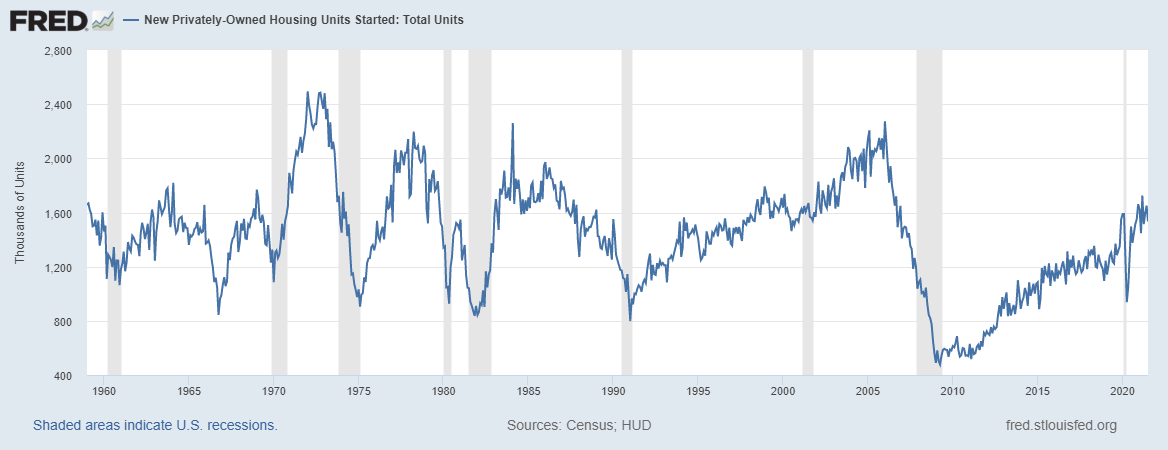

As you can see in the chart below, housing starts now are not higher than the previous post-1960s peaks — which, by the way, were during periods when mortgage rates were much higher than the current market.

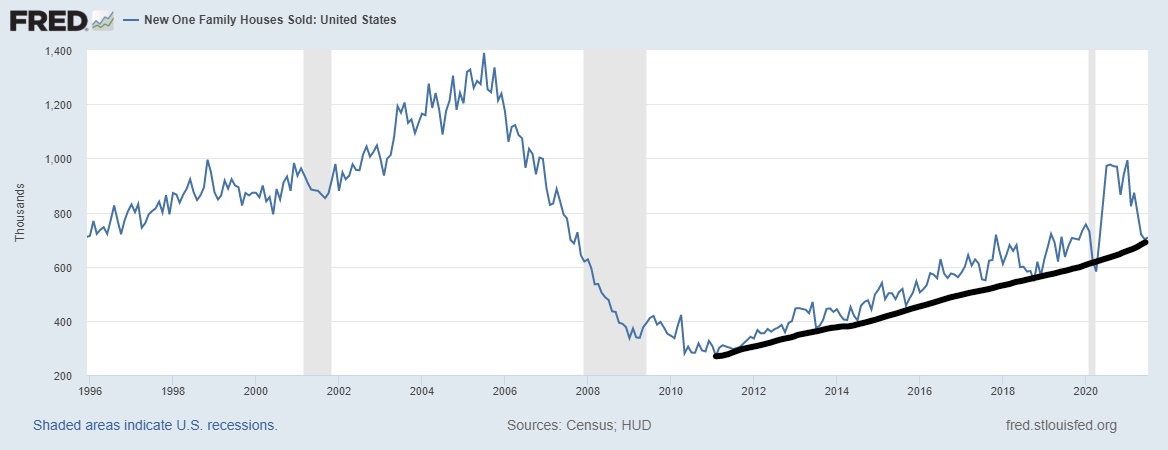

From the Census report: Sales of new single‐family houses in July 2021 were at a seasonally adjusted annual rate of 708,000…This is 1.0 percent (±11.3 percent)* above the revised June rate of 701,000, but is 27.2 percent (±7.3 percent) below the July 2020 estimate of 972,000.

New home sales came in as a beat, but revisions were all positive; that was the best part of the report. The best advice on the new home sales data is that this data line is exceptionally wild, both positive and negative. Typically, when it deviates big time, either way, it gets revised back to a trend.

A big theme of my work has been that housing data went straight parabolic last year. It wasn’t normal; it was all makeup demand in the second half of 2020, and some spillover into 2021. When the housing data moderates, don’t overthink that. Right now, just like the existing home sales market, we are moderating to a proper trend working on a more normal base to work from.

The builders aren’t fools. The make-up demand in the market combined with low inventory and good housing demographics gave them pricing power. They used this power to keep their margins solid even though construction costs rose significantly. How do you think they fund this operation? They aren’t the March of Dimes. They sell their products at a price to make money, and they did!

But even though lumber prices have crashed since then, don’t expect new home sales prices to go down. Instead, builder’s margins will get better, which is what they want as long as they can sell prices high without any discounting or incentives.

If you’re looking for a massive housing construction boom, don’t hold your breath. The builders manage their product line exceptionally well and won’t repeat past mistakes of overbuilding when the market is fading. The new homes sector gets impacted by higher rates much more than the existing home sales market, so builders need to watch rates and inventory. This recent inventory increase is occurring without increasing rates, so you shouldn’t be surprised that we don’t have a construction boom, just growth.

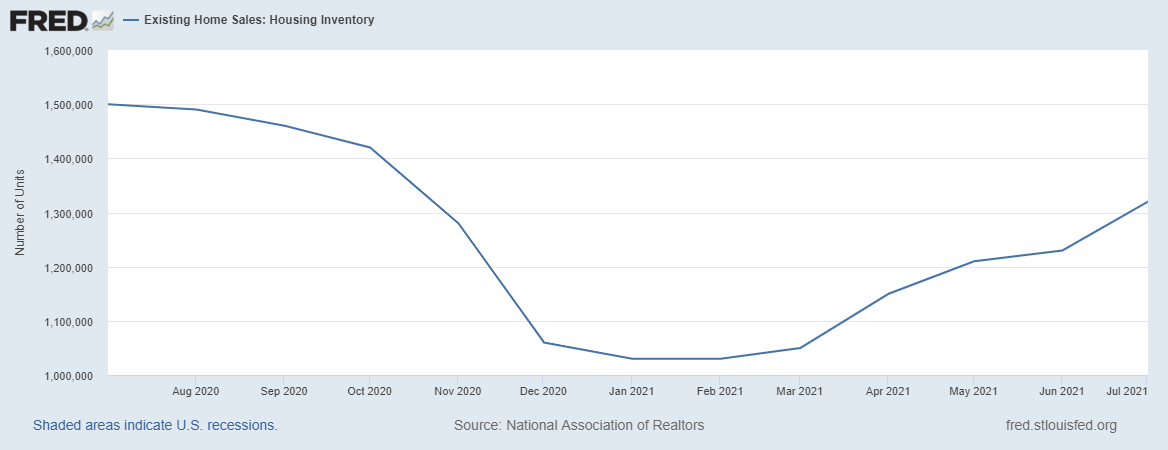

When considering the future of new home sales, remember that as existing home inventory increases, it provides more (and less expensive) competition for the new home sales marketplace.

For the first time in over a decade, the builders took advantage of the all-time lows in existing home inventory and captured some buyers from that sector. As long as mortgage rates stay low, the growing existing home supply shouldn’t provide too much of a competitive disadvantage for the builders. Existing home inventory levels are just bouncing off an all-time low. Some of the growth is also seasonal.

This was a good report for the new home sales sector. Sales beat expectations, and revisions were all positive. The monthly supply did rise but is still at moderate levels. We can expect that new home sales will be negative, year over year, for the rest of the year because comps were so high last year due to rebound sales. This does not mean the market is failing!

The new home sales and housing starts sector going back to trend after a very intense 2020-2021. The homebuyers for this sector are typically older and make more money than the buyers of existing homes, but the existing market is massive compared to this sector. If mortgage rates rise to even 3.75%, this can change the landscape for new home sales.

For now, however, we aren’t close to that, and an increase in rates was not part of my forecast for 2021. I projected a peak in the 10-year yield to be 1.94%. The highs so far have been around 1.75%, and we are at 1.28% today.

When assessing the U.S. housing market, its best to keep things simple. Don’t get caught up in the hot mess of the housing crash crew that has ruined so much of the housing discussion from 2012-2021. For both the existing and new home sales market, you just need to look to demographics and mortgage rates to know you have solid replacement demographic buyer demand to go with move up, move down, cash and investors, like the existing home sales report showed yesterday.