When the Department of Housing and Urban Development rolled out lower principal limit factors last year, many industry-watchers predicted that reverse mortgage originators would need to begin competing fiercely on margins.

While the changes have brought some increased competition, margins on adjustable-rate Home Equity Conversion Mortgages appear to be settling in the 2% range, according to data from Baseline Reverse.

“The simple average from April to June has decreased slightly from 2.11% to 2.05% to 2.04%, but we are not seeing a ‘race to the bottom,'” Baseline Reverse founder Dan Ribler told Reverse Mortgage Daily.

On the high end, meanwhile, the maximum mortgage margin on all HECMs funded under the new principal limit structure has dropped from 4.5% to 3.38% in June.

Those numbers track with more anecdotal evidence reported by RMD late last month, when originators from around the U.S. noted that margins tended to be falling somewhere in the 1.5% to 2.0% range.

“As far as the pricing of loans goes, I don’t think anyone can price at the floor right now with the index at 2.97% and the floor at 3%,” Bruce Simmons, reverse mortgage manager at American Liberty Mortgage Inc. in Denver, said. “The majority of my loans are priced between a 1.5% and 2% margin.”

This new focus on margins comes from the disappearance of the so-called “rate floor” of 5.06%. Under the new structure, every one-eighth of a percent difference in expected rate has an effect on the eventual principal limit all the way down to 3%, which prompted the predictions of cutthroat margin competition.

“It still creates the potential to give a loan to this client, but the lenders must be flexible in the margins they offer,” author and reverse mortgage professional Dan Hultquist told RMD last fall. “They’re going to have to reach down deeper to provide lower lender margins, and, of course, lower lender margins may protect borrowers with higher loan amounts.”

Ribler allowed that there have been some loans issued at extremely low margins — all the way down to .05% in one case — but aside from these outliers, the industry seems to be settling down in the 2% range.

“We haven’t seen much migration from April to May to June as originators tend to be offering consistently the same products,” he said.

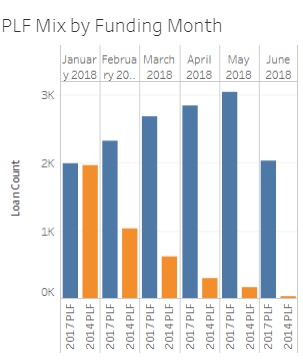

The Baseline Reverse data also shows a steady increase in loans funded under the new PLF structures, according to Ribler. Despite a decline between May and June, the analytics firm has tracked a steady increase in the 2017-vintage PLF loans as any remaining HECMs funded under the old structure clear out of the pipeline.

“The June numbers look down, but our data set includes only loans sold through July, and it’s probable that there were several loans funded in June that have not made it into HMBS bonds yet,” Ribler said. “We’ll need to wait one more month to see what actually happened in June, but it is quite apparent that the industry is increasing production of 2017 PLF [loans].”

Written by Alex Spanko

{kind=link}