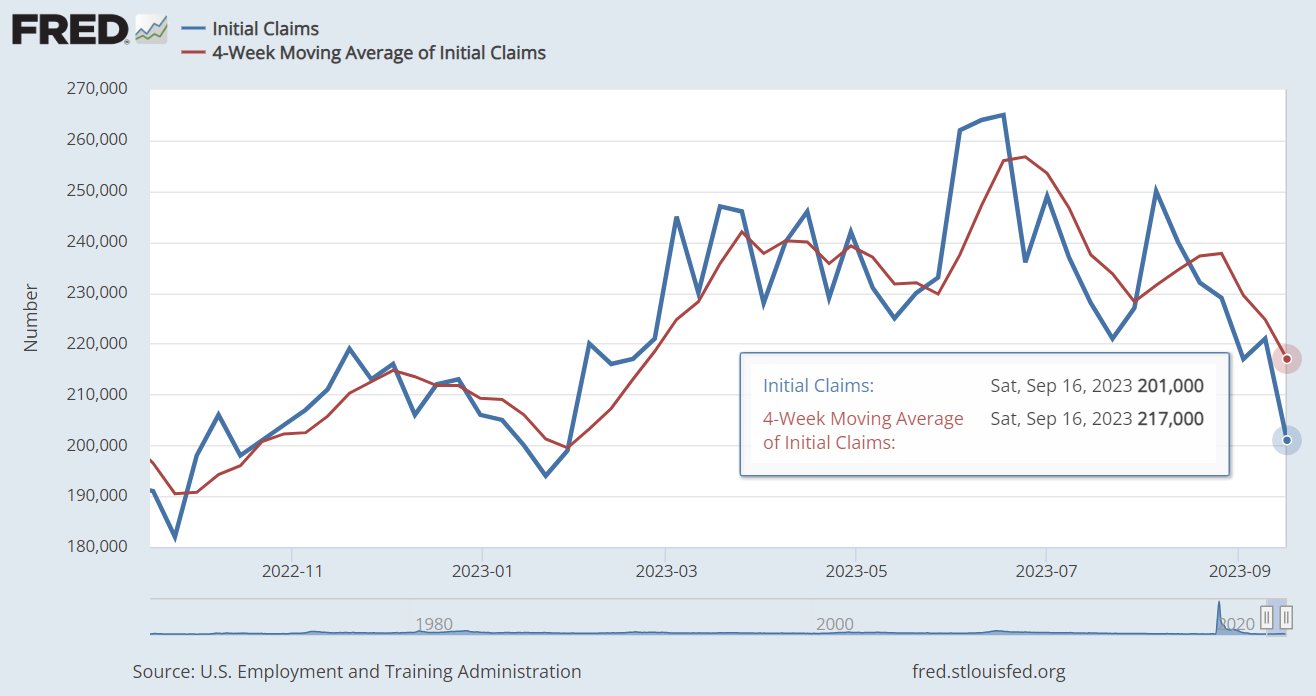

Mortgage rates shot up last week after a hawkish Federal Reserve meeting, even though they didn’t raise rates. In addition, jobless claims data had another solid print, showing that the labor market hasn’t broken yet, which led to more selling of the 10-year yield. Mortgage rates did find some relief on Friday as bond yields headed lower.

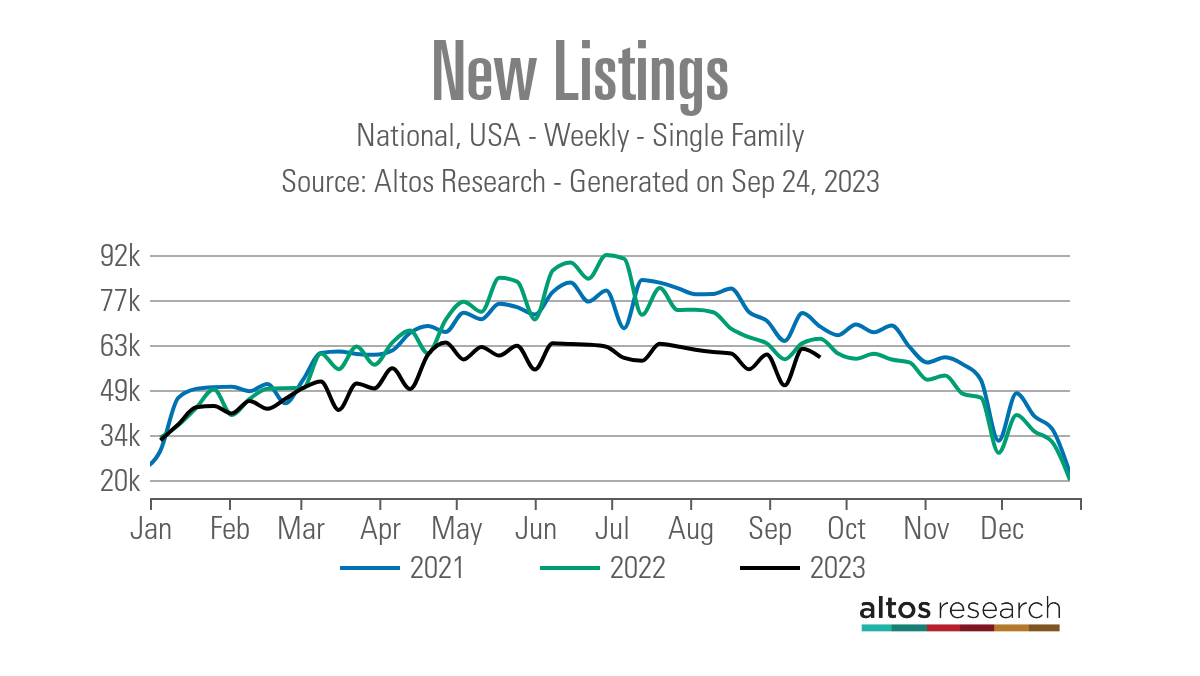

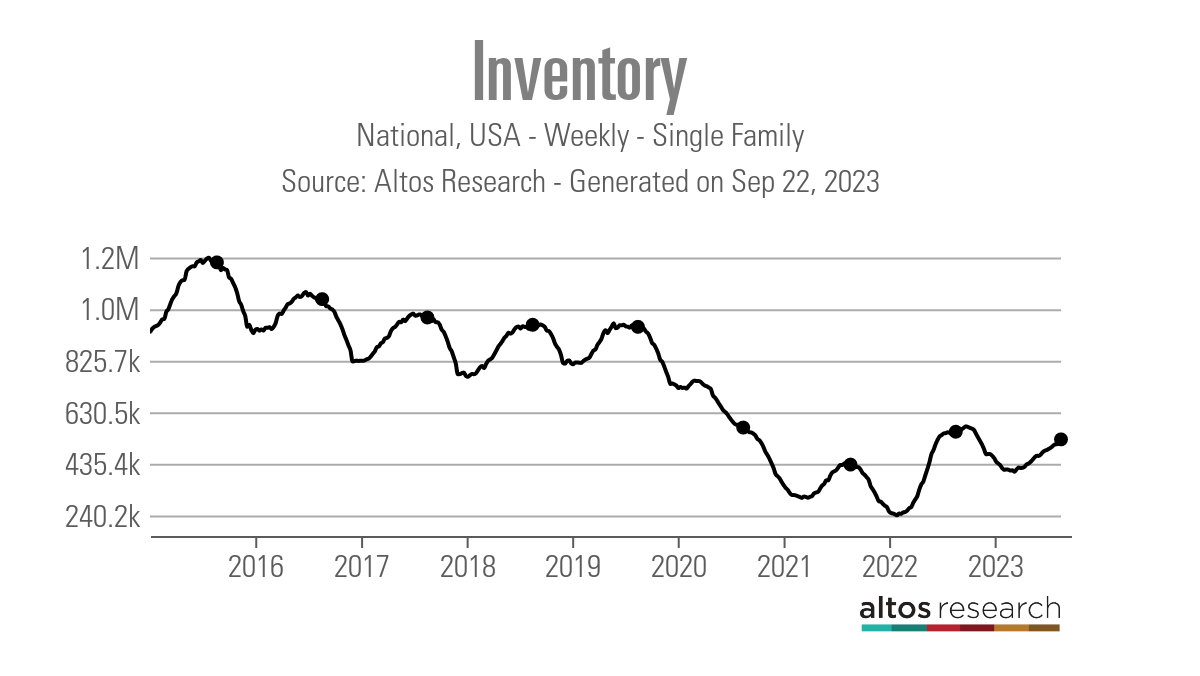

On housing inventory, new listings data saw a small decline last week, but active listings grew at a healthy clip. Purchase application data had another positive week, pulling off back-to-back positive prints.

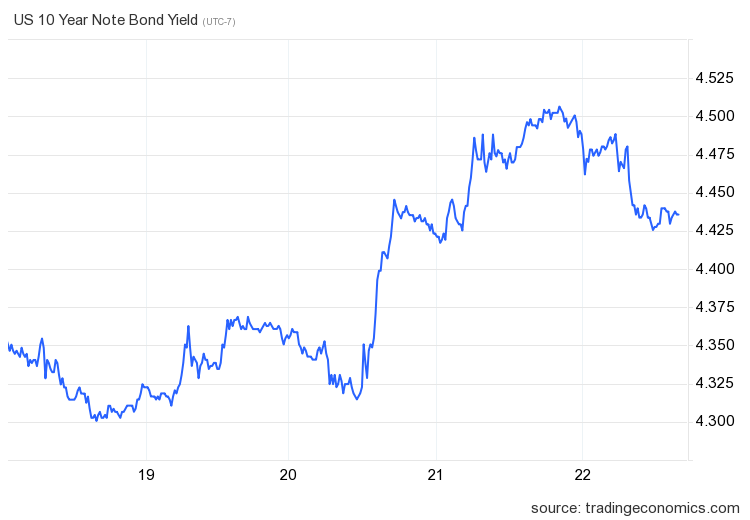

Mortgage rates and the bond market

Last week was wild for the 10-year yield, as the key support line that I have been talking about for weeks broke after the Fed meeting, sending the 10-year yield to highs last seen in 2007. The 10-year yield fell on Friday, bringing some relief, but we got very close to yearly highs for mortgage rates. Mortgage rates started the week at 7.28%, got as high as 7.47%, and ended at 7.39%. The yearly high is 7.49%.

I have noticed for weeks now that the spreads between the 10-year yield and mortgage rates are better, so rates didn’t hit new highs last week, even with the 10-year yield breaking to new yearly highs.

The Fed sounded hawkish in their talk on Wednesday, but their rate hike cycle is over now, with the possibility of only one more rate hike if they think it’s warranted. The labor market isn’t as tight anymore, but jobless claims had another solid print and are near monthly lows. The four-week moving average for jobless claims is 217,000 — far from the key level of 323,000 level that I think would trigger a Fed pivot.

Weekly housing inventory data

Whenever mortgage rates rise, I fear that the weekly new listings data will decline more aggressively because homebuyers simply throw in the towel on listing their homes to sell because higher rates make it less attractive to sell and buy another home

Last week on CNBC, I talked about how I still believe that we will see some flat to positive year-over-year data because we have had to deal with higher rates for longer and we haven’t see new listings data take a meaningful fall lower. A lot of this has to do with this data line trending at the lowest levels ever. I explained my premise here in this interview on CNBC.

We have had some volatile weekly numbers in the new listings data recently, but even with the mortgage rate spike, the decline was orderly, as it has been all year. So, I am not worried about another leg lower in the data.

- Sept. 15: 61,852

- Sept. 23: 59,107

There is some positive news: weekly active listings grew 9,312. This is not at the levels that I think we should see with mortgage rates this high, which would be between 11,000-17,000 weekly, but it’s good enough, considering that we are almost done with September. I am a very pro-supply person because more supply brings balance. It’s been hard to grow the housing supply this year as home sales are stable compared to last year’s massive collapse in demand.

According to Altos Research:

- Weekly inventory change (Sept. 15–22): Inventory rose from 518,626 to 527,938

- Same week last year (Sept. 16-23): Inventory rose from 552,042 to 556,865

- The inventory bottom for 2022 was 240,194

- The inventory peak for 2023 so far is 527,938

- For context, active listings for this week in 2015 were 1,198,033

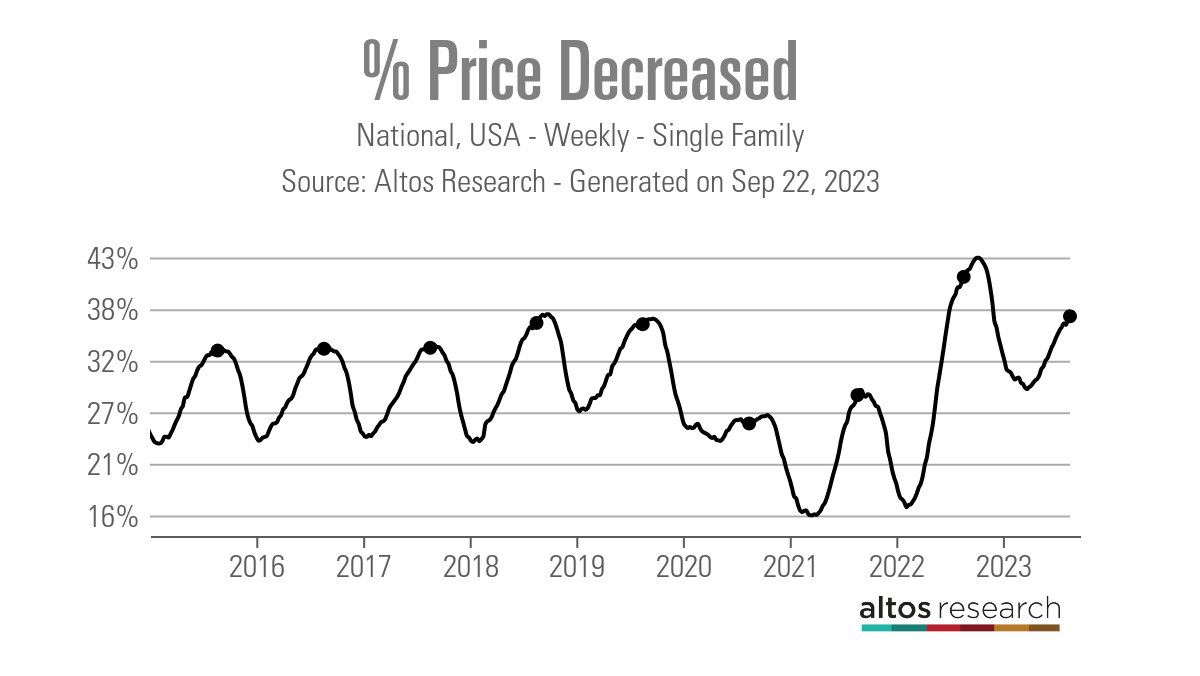

Historically, one-third of all homes have price cuts every year. Last week’s price cuts were lower than last year at the same time by 4%. This is happening with rates over 7%, too, and part of the reason is that housing inventory has been negative year over year since mid-June. Last year, inventory grew fast as the mortgage rate shock toward 7% created faster and higher price-cut data.

The housing market still has major affordability issues, and we are seeing a higher number of price cuts than in 2015-2017. Back then, we ran at 33%; in 2018 and 2019, it was 36%.

- 2021 28%

- 2022 41%

- 2023 37%

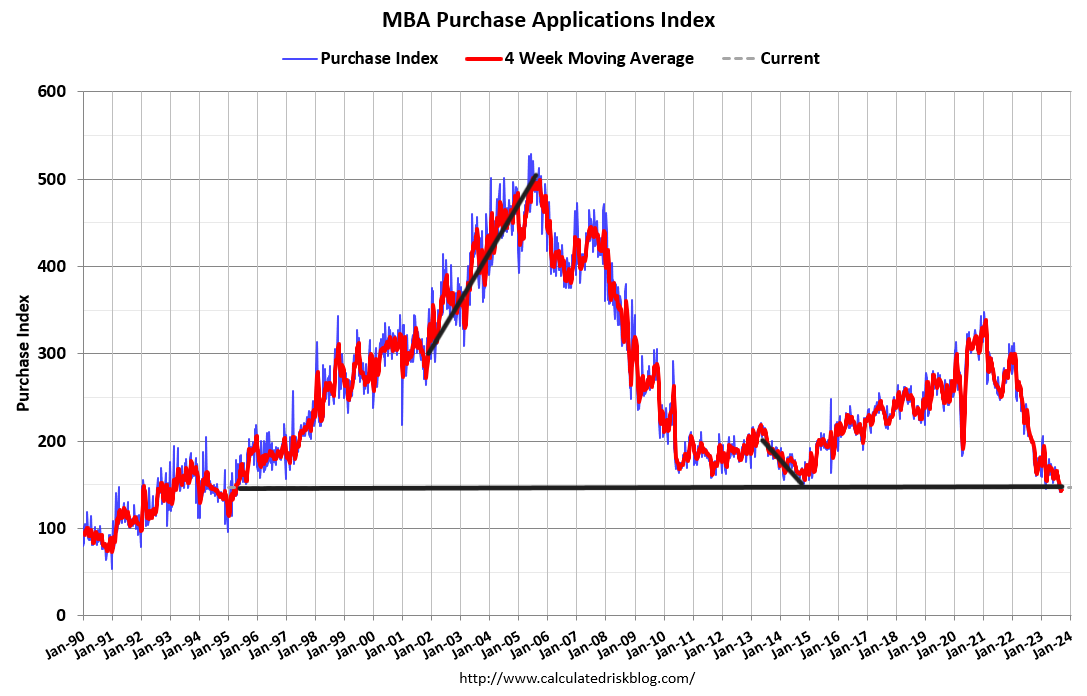

Purchase application data

Purchase application data was 2% higher last week, making the year-to-date count 17 positive prints, 18 negative prints, and one flat week. If we start from Nov. 9, 2022, it’s been 24 positive prints versus 18 negative prints and one flat week. The week-to-week data has gotten softer since mortgage rates have been trending above 7%. However, it’s not crashing like it was last year.

The week ahead: Housing and inflation data

We have another week of housing data ahead with new home sales, pending home sales, the S&P CoreLogic Case-Shiller home price index and the FHFA home price index. The pending home sales data should come in soft with the recent spike in mortgage rates. Also, we have the PCE inflation report, the main inflation data that the Federal Reserve tracks. As always, the Thursday jobless claims data is the key for this cycle and mortgage rates.