Mortgage rates are finally headed lower after a crazy week of jobs data showing that the economy isn’t going into recession. Job growth is slowing as we get closer and closer to the target range of the make-up demand in labor, but it hasn’t broken yet.

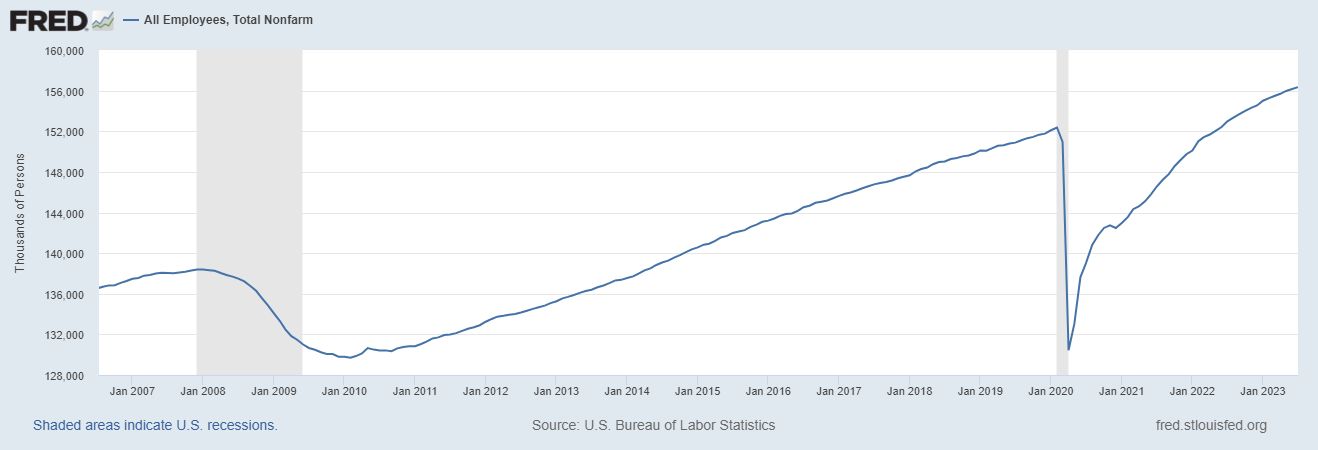

What do I mean by a make-up demand in labor? Assuming we had no COVID-19 and the economy continued as it had been — which was running at the most prolonged economic and job expansion ever recorded in history — we would be between 157 million – 159 million jobs today. Currently, we are at 156,342,000, which means we are a few jobs reports away from getting into that make-up range.

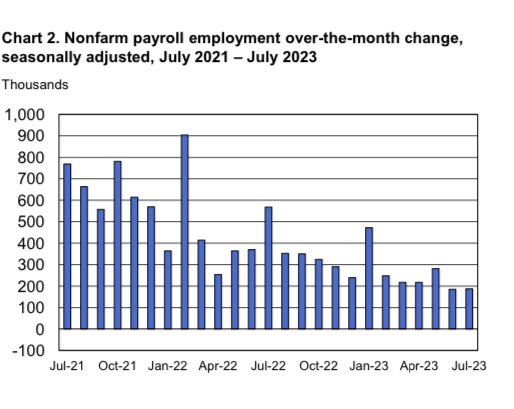

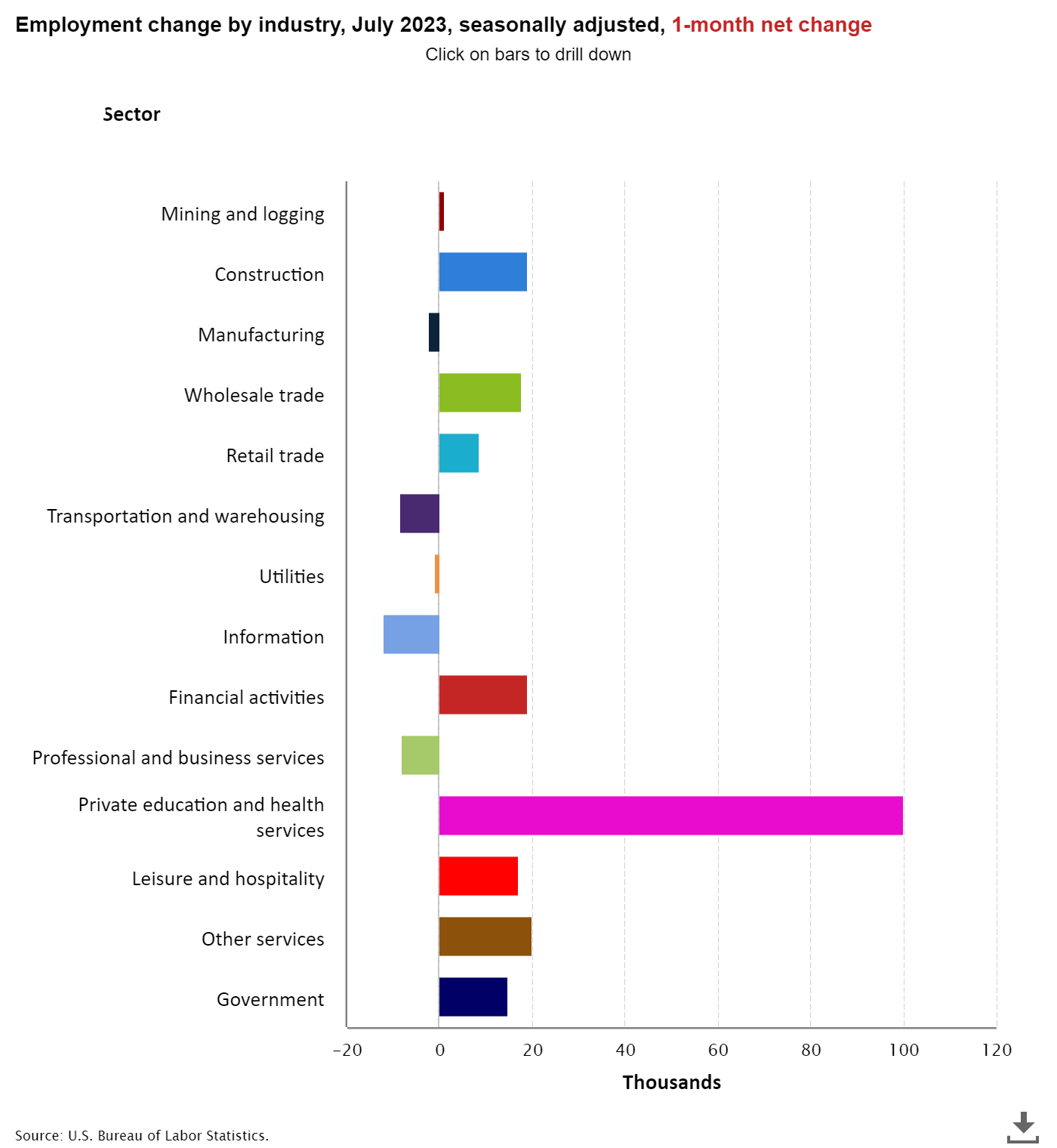

From BLS:Total nonfarm payroll employment rose by 187,000 in July, and the unemployment rate changed little at 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, social assistance, financial activities, and wholesale trade.

As you can see in the chart below, the job growth rate is slowing, as it should. We had negative revisions to this jobs report and excluding the government jobs, we are averaging 185,000 jobs added per month in the last three months.

Let’s look at the report’s internals, where we gained and lost jobs, and why mortgage rates fell today.

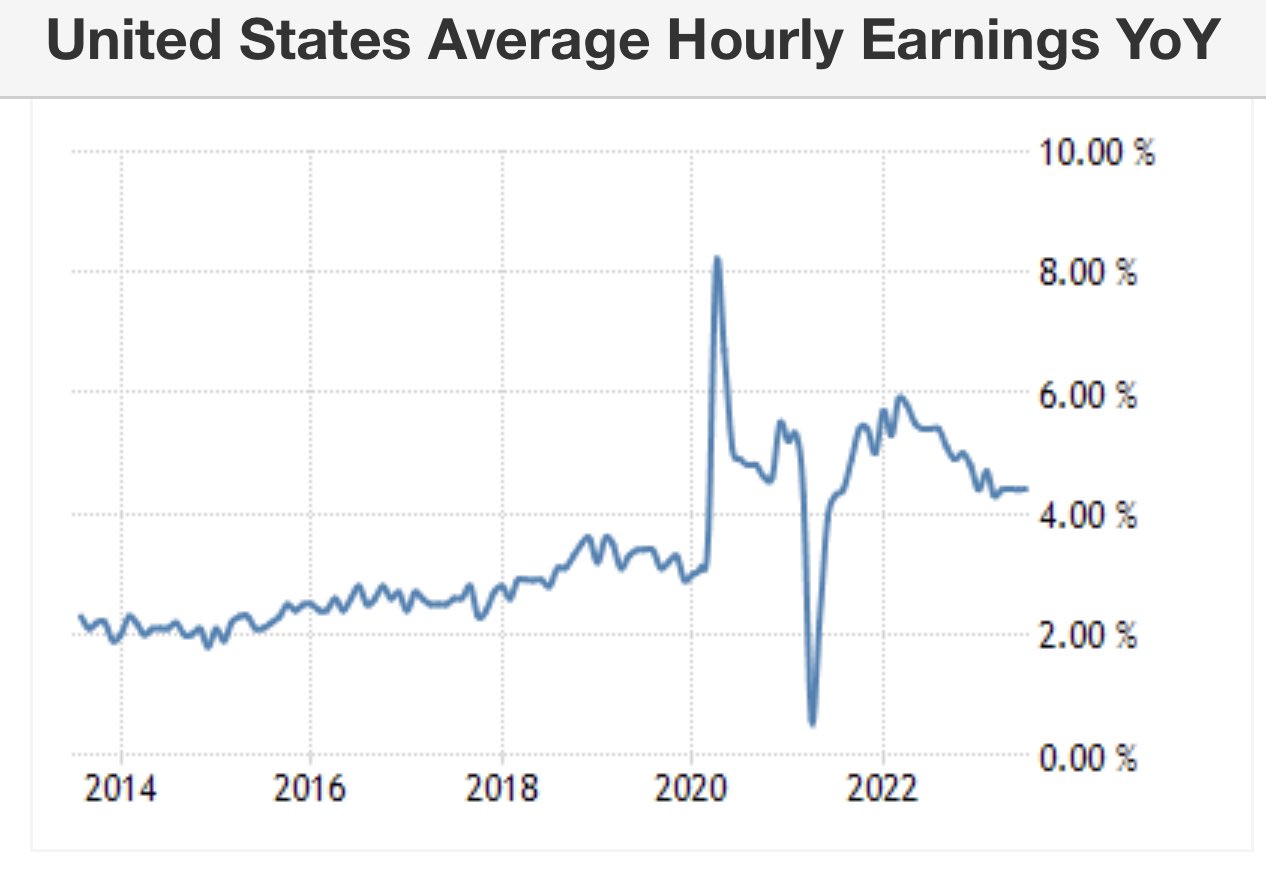

Wage growth is not spiraling out of control as some have feared; this would have been bad news for mortgage rates because that’s what happened in the 1970s. However, wage growth has stayed firm the past few months. With headline consumer price index inflation running at 3% year over year, people are seeing real wage growth again, as we have been steady at 4.4% for a few months here.

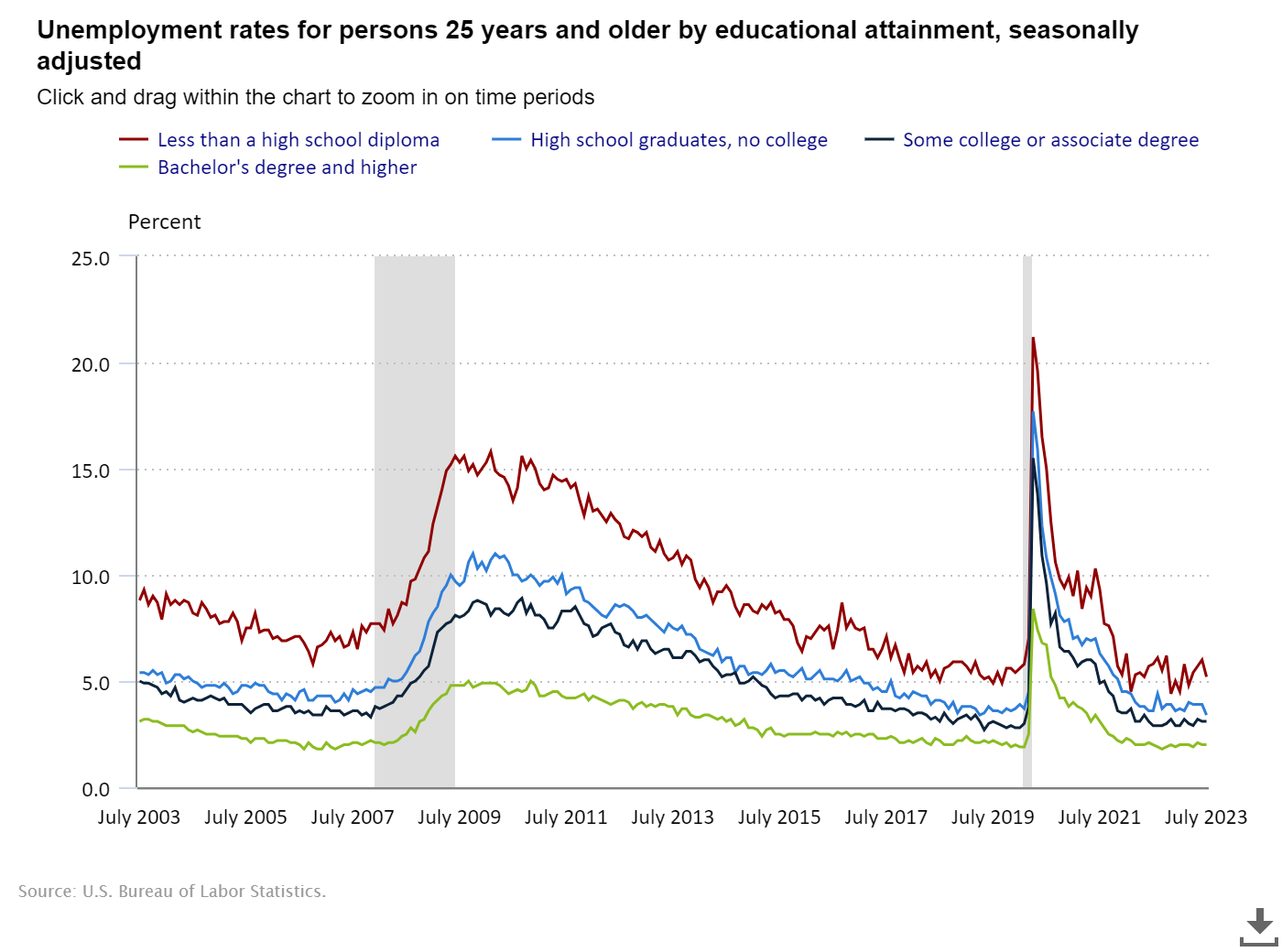

The unemployment rate for those who didn’t finish high school has been pretty wild up and down lately; in this report it fell from 6.0% to 5.2%. Traditionally, those without a high school education tend to have the highest unemployment rates in any recession.

In this job report, the unemployment for education levels:

- Less than a high school diploma: 5.2%

- High school graduate and no college: 3.4%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.0%

The hours worked were less in this report, meaning that employers are holding onto their labor but are cutting hours. If you want to see why mortgage rates are falling today, this is one data line to keep an eye on going out for months.

What other labor data did we have this jobs week?

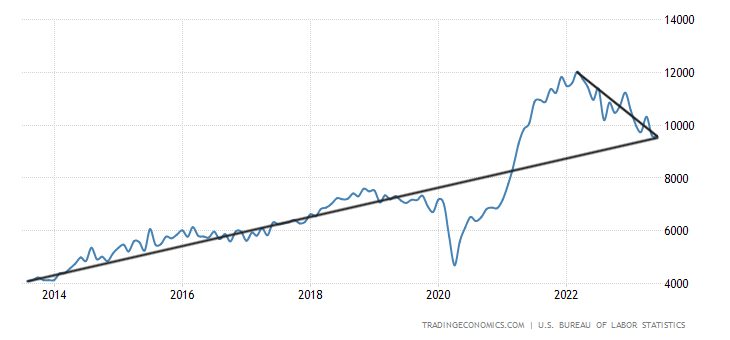

This week we had a decrease in job openings, but that number is still abnormally high for the Fed. Even though we have fallen from 12 million to under 10 million, the Federal Reserve would love to see this back toward the 7 million level. So far, no luck! Here is a look at job openings with a longer-term view, and you can see the decline from the peak.

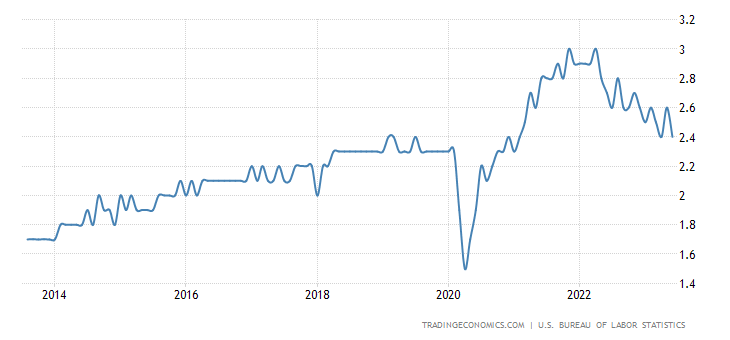

Now the quits ratio is almost back to pre-COVID-19 levels; this is a big thing for the Fed because less people are leaving work for higher wages, which they see as a positive.

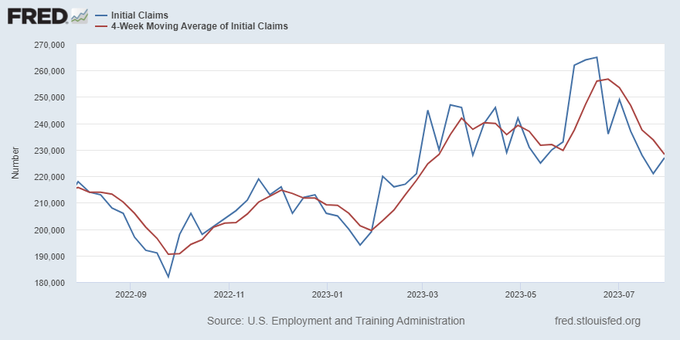

Jobless claims, the most important data line at this expansion stage, rose this week, but it is still far from my key 323,000 target level for the Fed to pivot.

From the St. Louis Fed: Initial claims for unemployment insurance benefits increased by 6,000 in the week ended July 29, to 227,000. The four-week moving average declined to 228,250

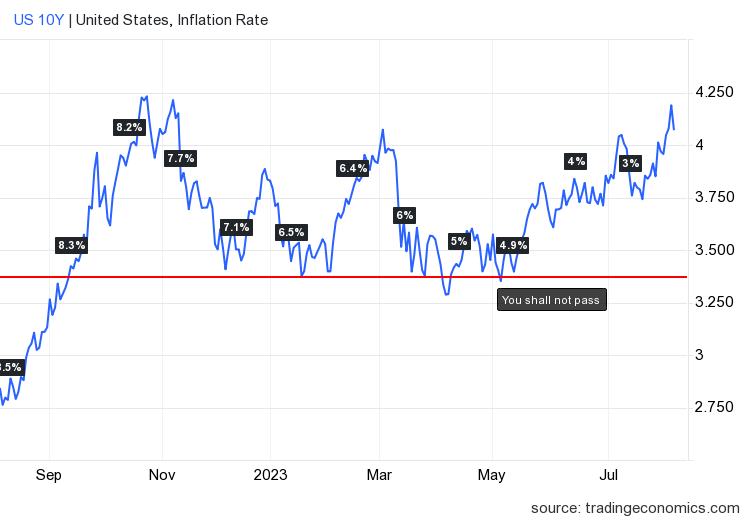

So what does this mean for mortgage rates? Today we were close to testing the high-end range for my 10-year yield 2023 forecast of 4.25%. We got as high as 4.20% but bond yields have fallen since that level. As I write this article, the 10-year yield is currently at 4.04%.

The 10-year yield channel has held in my range of 3.21%-4.25%, which equates to mortgage rates of 5.75%-7.25%, assuming where the spreads were at the start of the year. This is how I traditionally forecast mortgage rates for a year, by creating a level of where the bond market should be for most of the year. If the 10-year yield closed above 4.25% today and we saw more bond market selling next week, we would need to have a new conversation about mortgage rates rising more this year than I had anticipated. However, that hasn’t happened yet.

It’s been a crazy week with jobs data and the bond market. The key, for now, is that the labor market is slowing down but not breaking. We held the key line on the 10-year yield and mortgage rates went lower today, so at least for one day the housing market can say it was a good Friday. Next up is the Consumer Price Index inflation report on Aug. 10, which will be a market-mover for mortgage rates.

Interesting