The growth rate of inflation has been falling for a year, but mortgage rates are still near multi-decade highs. Why? While it is true that mortgage rates traditionally fall alongside inflation, I believed 2023 was going to be about the labor market. This was the core premise of my 2023 forecast, and so far it has worked.

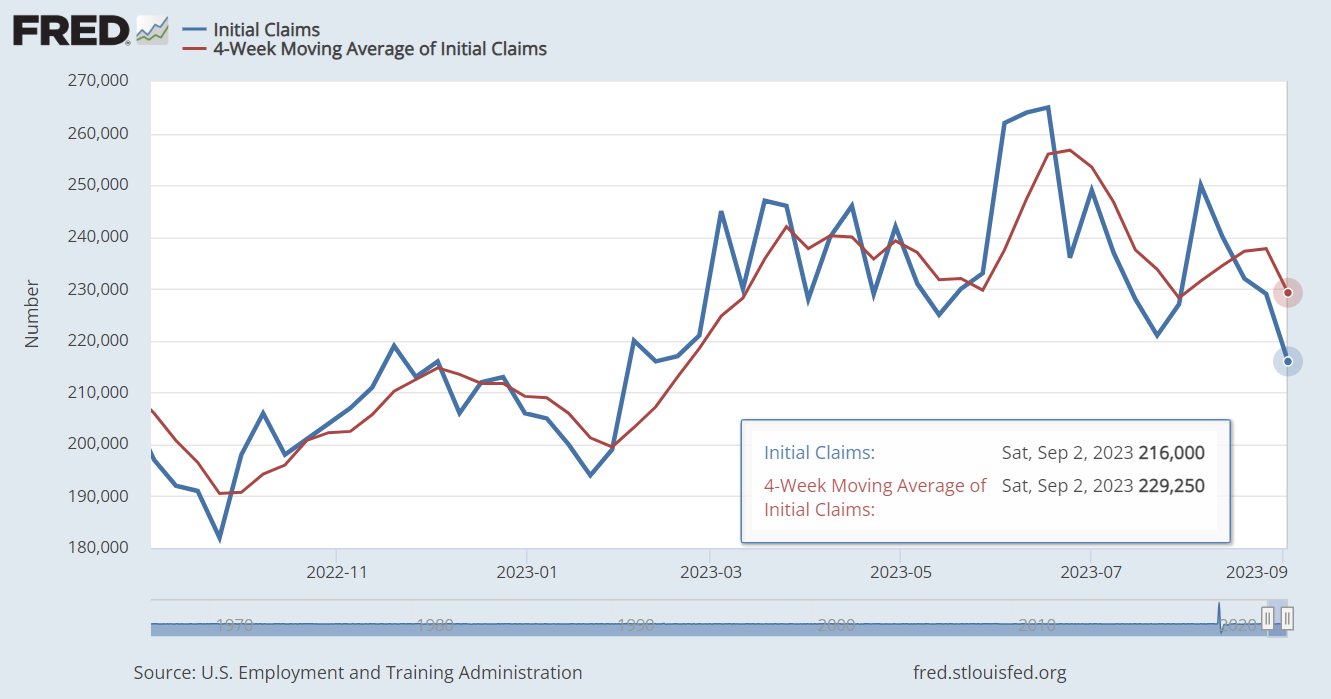

In my 2023 forecast, I set the range on the 10-year yield between 3.21%-4.25%, emphasizing that the bond yields can go lower than 3.21% only if the labor market breaks — which would require jobless claims to go over 323,000 on a four-week moving average. The labor market is not as tight as it used to be, but jobless claims are not breaking either. As shown below, 229,250 on the four-week moving average is historically deficient.

From the Fed: In the week ended Sept. 2, initial claims for unemployment insurance benefits declined by 13,000 to 216,000, the lowest level since February. The four-week moving average declined by 8,500 to 229,250.

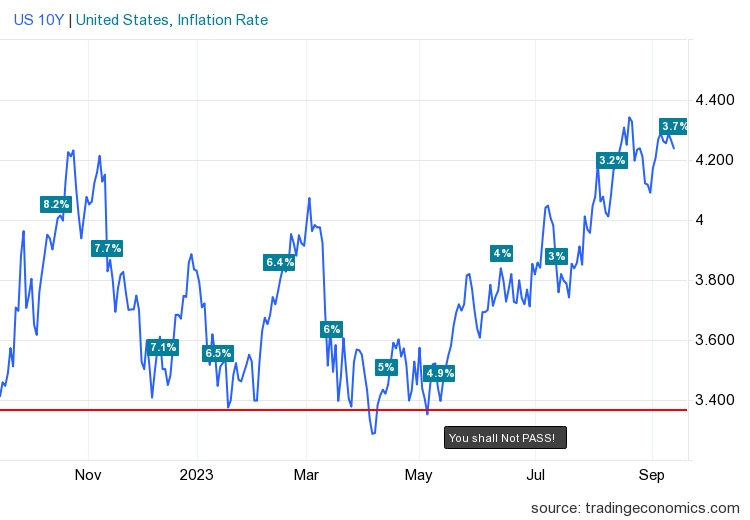

After Wednesday’s CPI inflation report, we can now look at a one-year data line set comparing the 10-year yield and the growth rate of inflation to see that we had lower mortgage rates with hotter inflation data. While the data below is headline inflation, not core inflation, we have made good progress from the 9% plus year-over-year inflation growth data we had last year.

What do we think about mortgage rates and inflation now? Let’s take a look, since a year ago I went on CNBC and talked about how the growth rate of rents cooling off would be a 2023 story, and it’s a good one for inflation.

Wednesday’s CPI report was firmer than expected, but the core disinflation story remains intact and this is key for the Fed and what they will think about in the future.

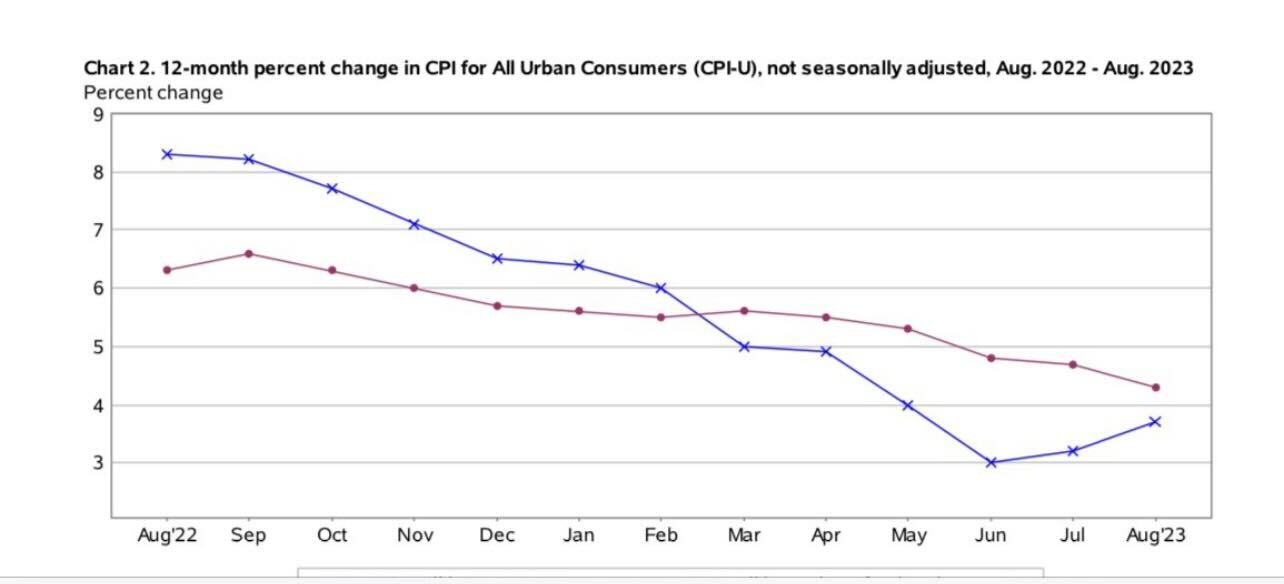

From BLS: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.6 percent in August on a seasonally adjusted basis after increasing 0.2 percent in July, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 3.7 percent before seasonal adjustment.

As shown below, headline inflation has increased over the past two months as oil prices have risen. However, core inflation is still in a downtrend. The Fed has always stressed that core inflation is key, so even though we made better progress with headline inflation, that doesn’t matter to them as much as core inflation.

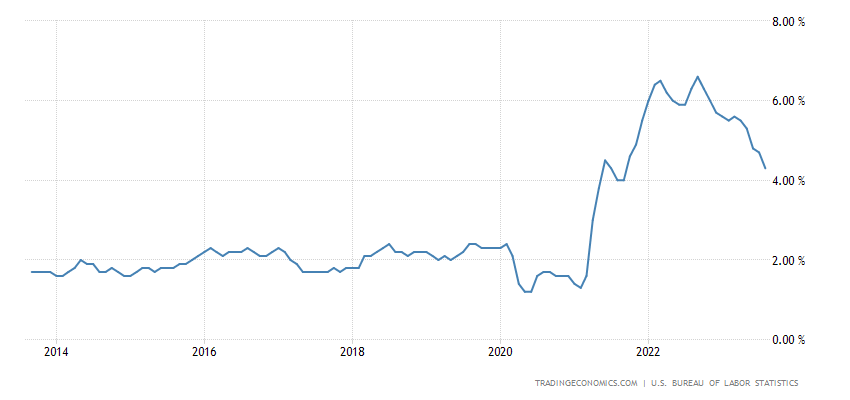

A longer look at core inflation, where the Fed focuses its energy, shows a lot of progress from last year, but it’s still historically high compared to COVID-19 trends.

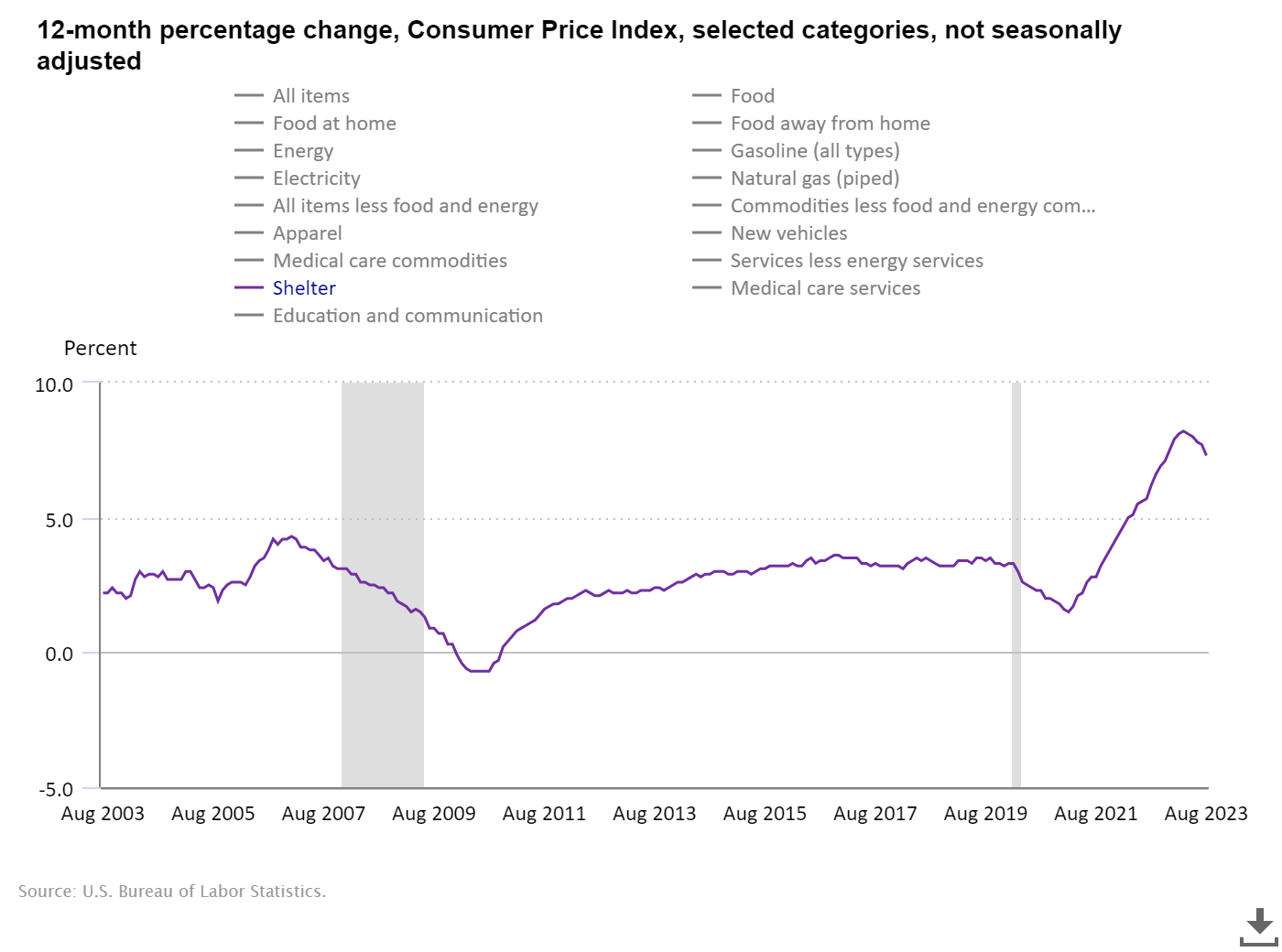

Also, the biggest component of core inflation is shelter inflation, which has legs to go lower for many more months. This data is much lower in real-time, so the core inflation data isn’t far from the 2% that the Fed targets. The Fed knows this, too.

Now, why is inflation data more important going out? The Fed has talked about rate cuts next year, even without a job loss recession, because they believe rates are currently very restrictive with the inflation growth rate. Now, as long as the inflation growth rate falls, they will cut rates a bit to ensure the U.S. doesn’t go into a recession where they will have to cut more than they like. So, for the first time in a while, the groundwork has been laid for a rate cut with the growth rate of inflation falling.

For 2023, the key data line I was tracking was jobless claims, even more than the inflation growth rate. Next year will be different. As of this writing, the 10-year yield is at 4.25%, and we are at the peak of the forecast for 2023. Going into next year, we do have a lot of key economic data to track, but for the first time, we can see we can get rate cuts without a job loss recession.

This is why it’s important that the growth rate of inflation is falling, but it will influence the Fed and mortgage rates more in 2024 than 2023.