Remember that pretty girl from your history class in college — the one who would blow hot and cold, so you never really knew what she was thinking? The U.S. housing market can be like that girl: you can get many mixed messages (especially about a housing bubble) unless you are paying attention. But who has time for that? Hey, that’s all I do, so you’ve come to the right place.

The latest messaging is that the Federal Reserve is creating a housing bubble by keeping rates so low that prices can skyrocket. Or that Americans who recently purchased homes are going to get all their equity wiped out when housing prices take a nosedive. Recently, CNBC contributor Peter Boockvar was quoted in Trading Nation as saying:

“I feel bad for the people who bought homes over the past year because they’re the ones that paid the very elevated prices.” The article goes on to say that “He singles out those who put down 5% amid historically low mortgage rates. If home prices correct by 10%, Boockvar sees a world of pain.”

A world of pain because a purchaser had the financial wherewithal to buy a home for their family during a time with historically low mortgage rates? Really?

To be fair, there is potential for pain if one purchased a home at the “top of the market” with a very low down payment right before a job-loss recession. This is one of the risks of “late-cycle lending.” Taking on debt, with little selling equity, then losing your means of repaying that debt is a crappy situation for anyone — and if it happens to a bunch of people at once, it’s even worse. But how likely is that scenario in the current market?

The factors that would need to be present to cause that pain are the following:

- Recent housing prices represent the top of the market.

- Recent purchases were made with no or a meager down payment, so new homeowners have little equity.

- We are going into a job-loss recession, so current homeowners have a high likelihood of losing their income stream.

The first condition: Housing prices are at the top of the market

Let’s look at the evidence for the first condition — that housing prices are at or near the top of the market.

I have talked about home-price growth during the years 2020 to 2024 because this is a period with the best demographics for home buying ever in our history. I have talked about if home prices would grow by up to 23% during this time due to our stellar demographic profile, it would be manageable.

Unfortunately, we have already achieved that level of price growth in 2020-2021. In my perfect world, we would have flat to negative home-price growth until 2025 to offset the home-price growth we have already seen. However, the real world doesn’t work that way. We have three more years of stellar demographics to drive demand which could lead to more unhealthy price growth during a time with historically low mortgage rates.

I can hope we have reached the apex of price gains, but is that likely? No, that’s not reasonable. The growth rate cools down, yes, but the very peak is not expected.

The shortage of homes on the market is another factor forcing prices to go up much faster than I am comfortable with. Housing tenure, which was five years from 1985-2007, has doubled from 2008-2021. In some parts of the U.S., people are staying in their homes for over 15 years. (I’m one of those people!)

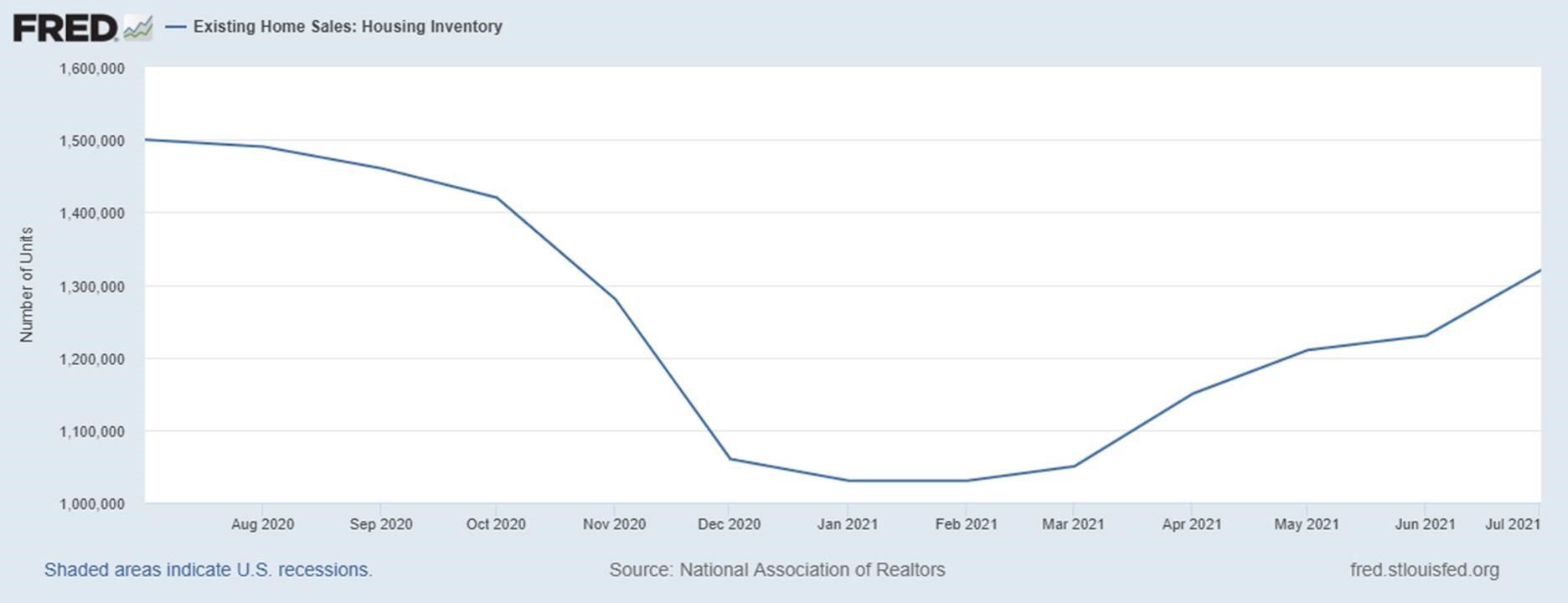

Inventory has been increasing since February of 2021, but so far, this has just been the typical seasonal adjustment in inventory from all-time lows. Ideally, these gains in inventory will not fade in the fall and winter this year like they usually do. We want higher inventory to stick and go higher in 2022 to balance inventory and demand.

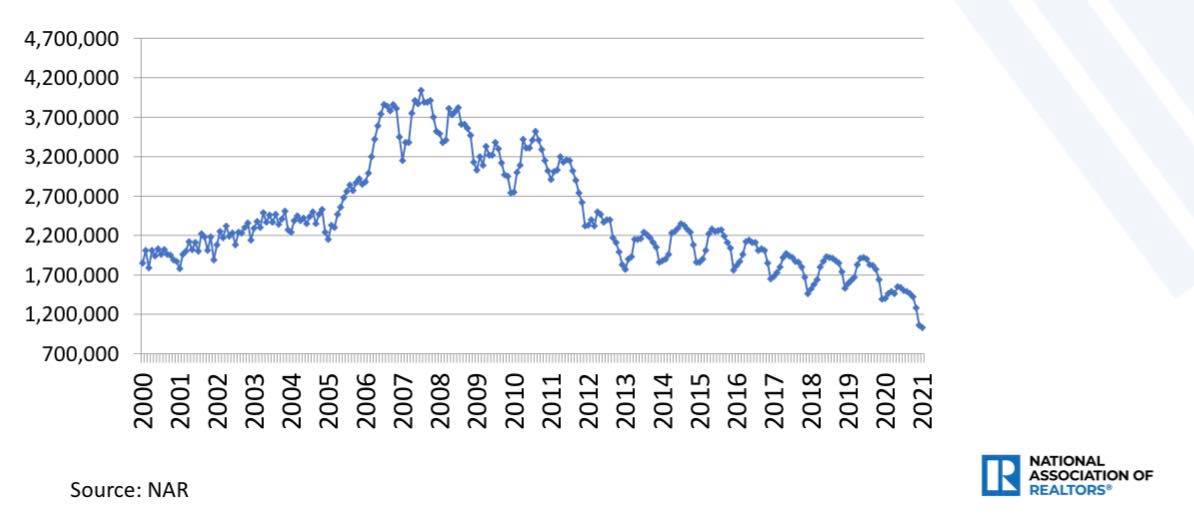

Speaking of demand, every existing home sales print this year has been higher than we closed in 2020. If we end this year with only one print below 5,840,000, then I would have to say demand is slightly better than I anticipated. More on that topic can be found here.

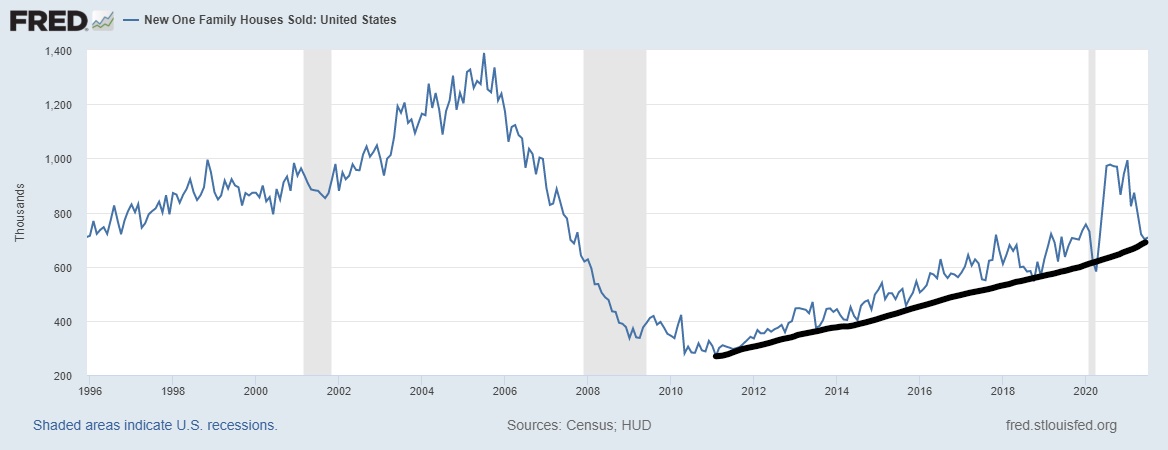

The new home sales market is where I can make a better case that sales have cooled, but that is just compared to the rebounding market following the COVID-induced slowdown. Last year in housing was not normal; a delay in sales due to COVID-19 followed by a massive rebound, then sales moderating back to trend.

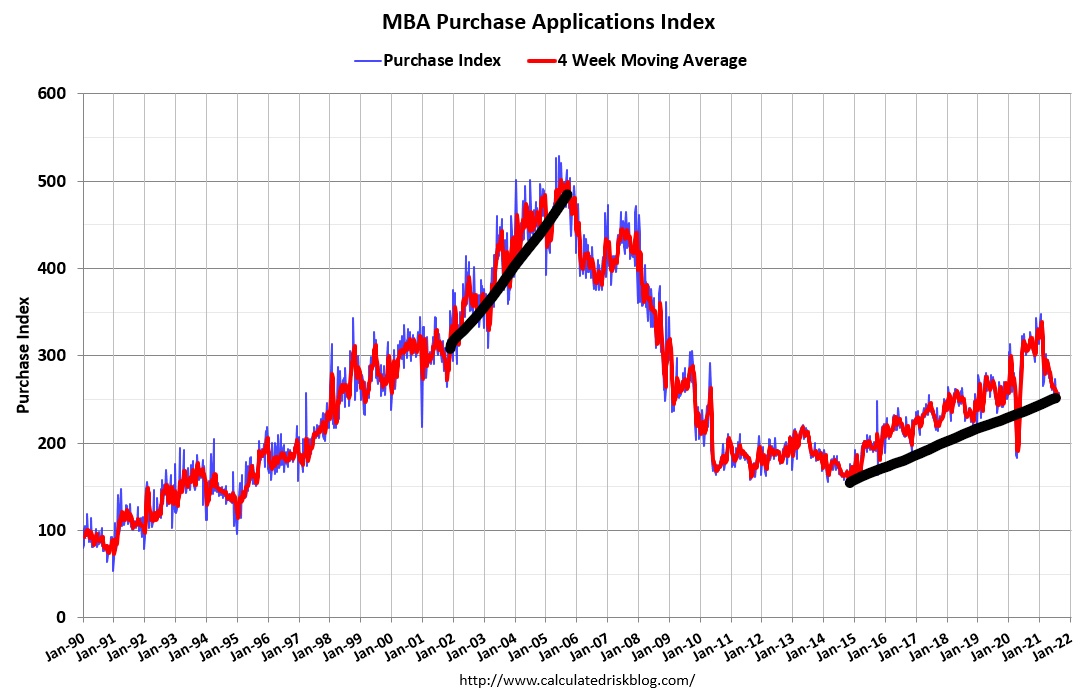

This pattern is evident in the purchase application index, as shown below. We had a V-shaped recovery last year in the data, then an abnormal volume surge after May, which never happens. This has created abnormally high comps for the second half of 2021.

On paper, it looks like purchase application data is down between 16%-18% year over year, but in reality, not much is happening. We are looking to end 2021 with more home sales than 2020. I wrote about this topic early in 2021 — that we should all expect negative year-over-year data in purchase applications due to the COVID-19 comps. Soon, this will be the case for all home sales data as well. This does not mean that we have a housing bubble because we don’t have a credit boom in 2021.

Now some may say that all of this is just making a case for those, like Boockvar, who believe that low mortgage rates are driving demand and creating a housing bubble, just like what happened between 2002 and 2005. In a recent article, I discussed all the differences in the current market compared to the housing boom period of 2002-2005, and the differences are many.

However, the main difference from the 2000s is that we had loose credit standards which facilitated leverage and drove speculation demand and a credit boom. Low mortgage rates may have played into that demand, but they were not causal in prompting speculation.

We know this because from 2008-2019, we had much lower mortgage rates than what we saw from 1996-2005, but we also had the weakest housing recovery ever and no credit boom. The inflation-adjusted mortgage debt currently isn’t even positive compared to the peak of the housing bubble.

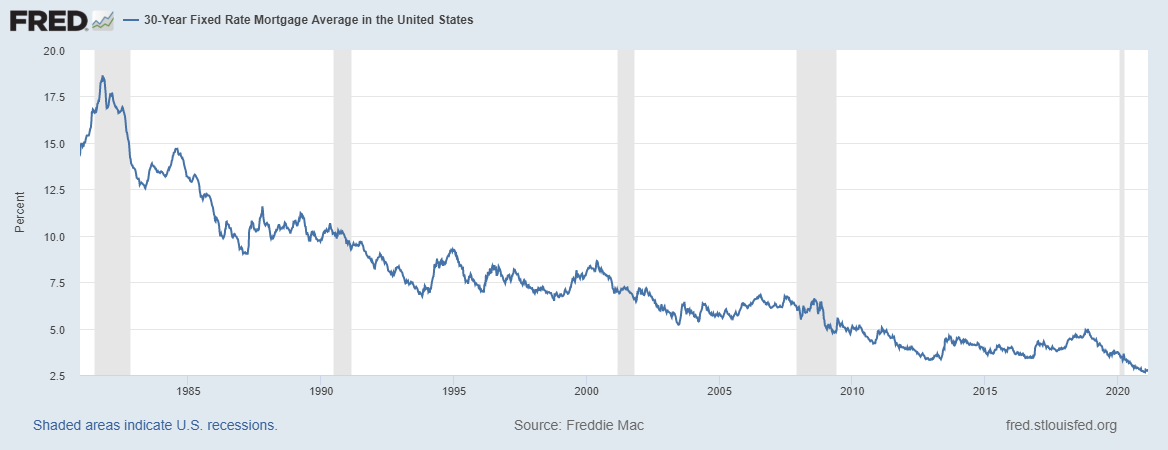

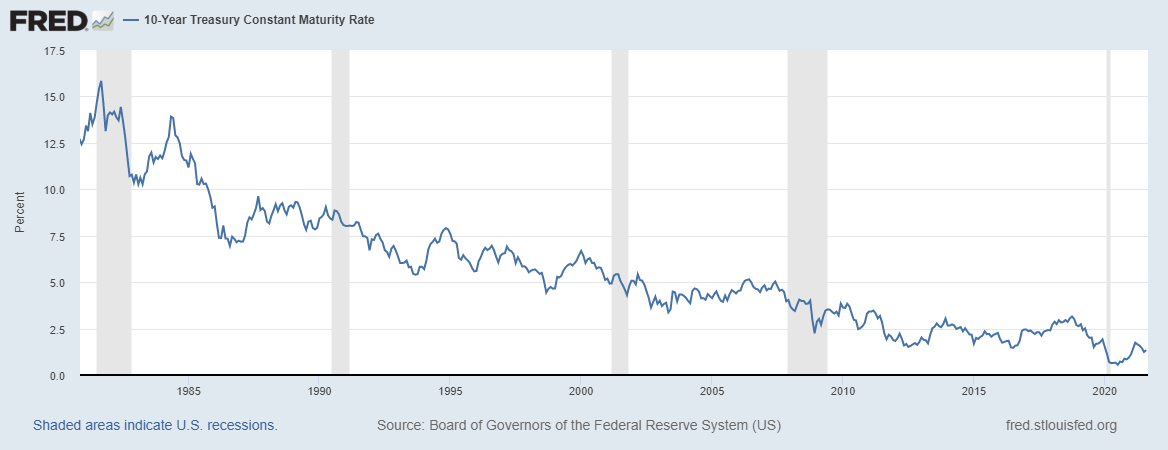

Remember, too, that mortgage rates and the 10-year yield have been falling since 1981. This has been a long-term down trend that has never once broken higher with any staying power. Plus, rates and bond yields tend to fall during a recession, not go up. So if we go into a job-loss recession (and there are no signs of this on the horizon), mortgage rates will stay low and go lower.

From 2008 to 2019, despite the low mortgage rate, the household formation wasn’t strong enough to drive purchase applications to 300 or housing starts to start a year at 1.5 million. We didn’t see those stats until 2020 when our favorable demographics finally kicked in. At the start of 2020, right on schedule, purchase applications hit 300, then stalled due to COVID-19, so a lot of folks didn’t even notice that housing had broken out of its doldrums.

All of that is in the past. It won’t be long before we start a year at 1.5 million. I talked about this in my 2021 predictions, as I had two long-term forecasts for many years.

So, from 2008 to 2019, mortgage rates were low, but demand wasn’t booming, and housing tenure wasn’t so long that it was bottlenecking the market. As you can see below, housing inventory has been falling since 2014, when purchase applications data started to rise from an all-time low adjusted to population. Even when mortgage rates got to 5% in 2018, the inventory picture didn’t change much for the existing home sales market. But the rate of growth in home prices cooled, which I wrote was healthy for the market as Americans had choices on homes to buy.

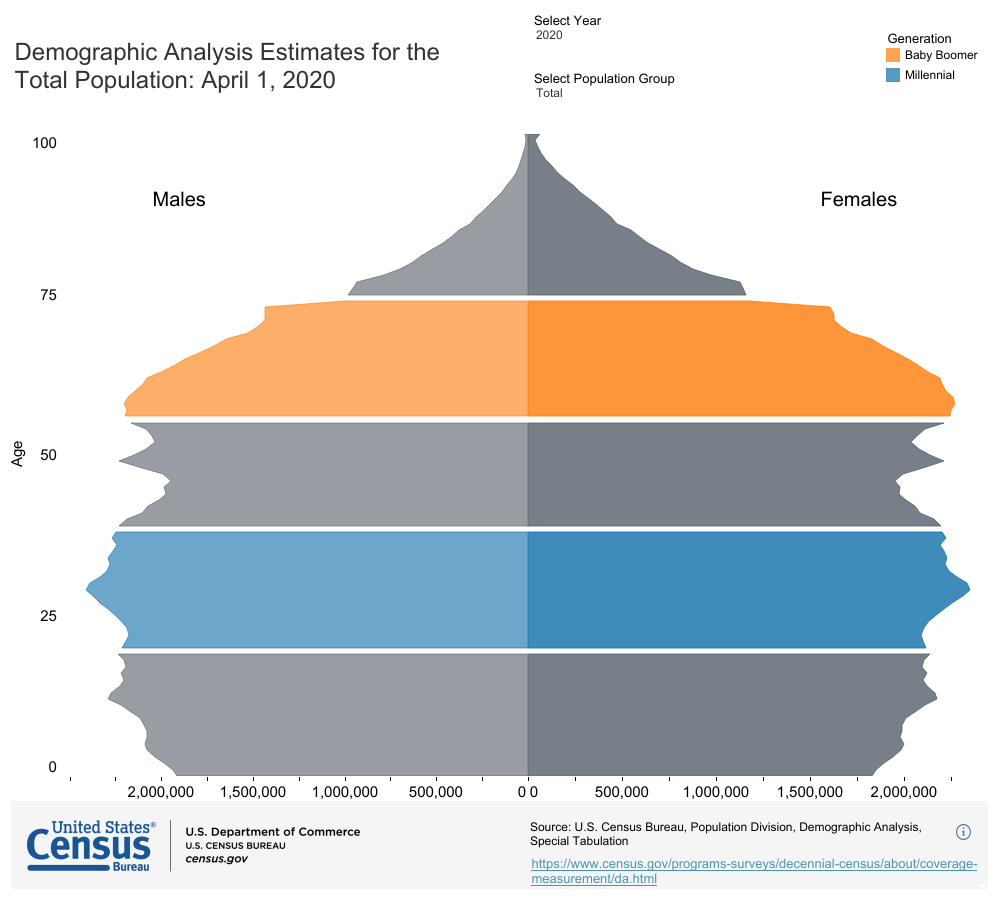

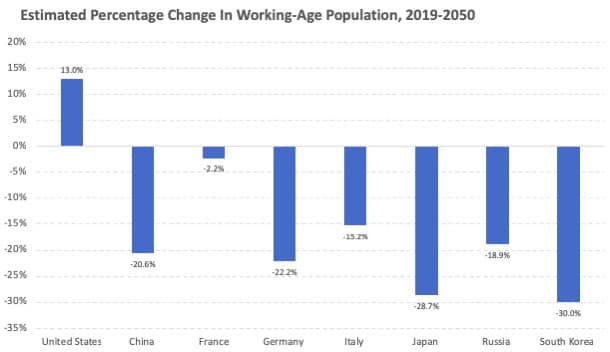

Today, however, we have demographics driving demand, and she is not playing. The number of people aged 27-33 is 32,458,118! This is the biggest demographic patch ever recorded in U.S. history, and the median age of first-time homebuyers is 33. The biggest age group currently is 29. But even with these positive demographics, we don’t have a credit boom. We just have solid replacement demand. With all these young Americans, you have to add to the buyer profile the move up, move down, cash and investors into the buyer demand pool mix.

Even with this demographic juggernaut, some people believe we are on the verge of a second housing bubble crash. When Boockvar said in the Trading Nation article: “People are now seeing sticker shock in home prices, and they’re backing off. Buyers are calling a time out. They said ‘I can’t afford this’ or ‘I want to wait to see home prices cool down,” I say, good on them. That’s how the market works. Prices rise too fast, and demand starts to cool — nothing new there and nothing that indicates a pending bust either.

If the lending standards were too loose so that folks could get mortgages for more than they could afford, this would be a problem. But that is not happening. And this leads us to the second condition that would need to be met to set the stage for the so-called “world of pain” or housing bubble scenario.

The second condition: Homeowners have little equity

Do our homeowners have little to no equity?

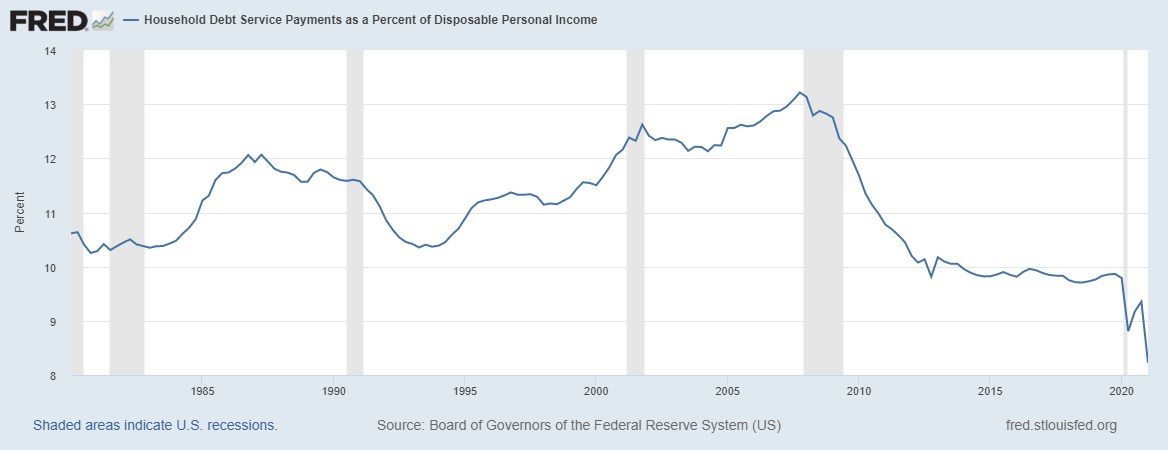

Again, the short answer is no. Because credit standards are reasonable now, mortgage holders can own the debt, notwithstanding some personal financial catastrophe. They’re buying a payment to provide shelter. That payment is a fixed low debt cost in an economic environment of rising wages. This is why the American homeowner has never looked better in history. They typically have excellent cash flow, high FICO scores, and nested equity.

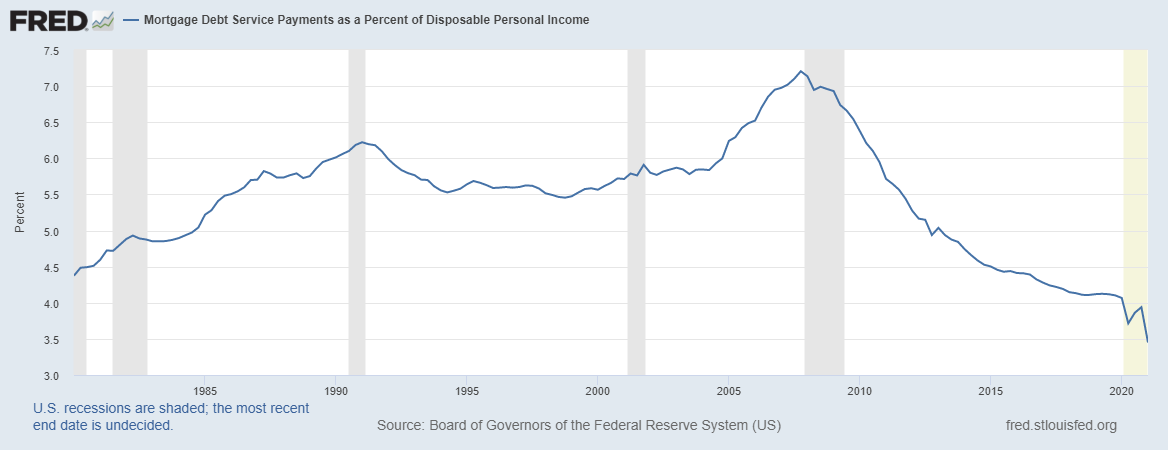

In fact, household debt service payments as a percentage of disposable income are at all-time lows. The multiple refinance booms the market has had since 2010 have driven debt costs down while wages overall have been rising.

The third condition: U.S. economy goes into a job-loss recession

The third condition that needs to be met for our world of pain/housing bubble scenario is that the U.S. economy needs to go into a job-loss recession. Is this likely?

Again, the answer is a big fat no. The recession ended in April of 2020. See my “American is back” recovery model for more on this and the charts to back it up here.

We currently have over 10 million job openings with 5.7 million jobs left to fill to recover all the jobs lost to COVID-19. We should be able to get all these jobs back by September 2022 or earlier. Further, we are very early in the economic expansion, so it is all up from here. We just passed the fiscal stimulus plan, and our demographics are going to keep driving consumer demand.

The previous economic expansion, the longest economic and job expansion in U.S. history, was paused for two months before we began the recovery. If anything, economic data is too hot that we should expect many data lines to moderate back to a proper trend; just check out retail sales.

So is a job-loss recession around the corner? The answer is not just no, but hell no!

If we look at the market and the economic environment, we can say with some confidence that the people who don’t support the Federal Reserve, like my friend Peter, don’t have much of a story to tell. We do not have any evidence that the Federal Reserve is setting the stage for a housing bubble by keeping short-term interest rates low.

For those interested in my thoughts on why the purchase of mortgage-backed securities by the Federal Reserve is not holding the housing market up like a puppet master, see my recent article in Housing Wire.

If you want someone to blame for home prices rising, don’t blame just the Federal Reserve. Blame the American homebuyer. We love big single-family homes and spend a lot of money to make our homes fancy for long-term living. Blame the builders for building bigger and bigger homes while our family size has been shrinking.

We don’t like to rent apartments when we make enough money to buy. At the same time, we fight to prevent the construction of multifamily homes or affordable housing in our neighbors. Blame America for having too many younger people, something other countries don’t have. From the Census Bureau:

The builders build based on the buyer demand curve to protect their profit margins and business models. They will never oversupply a marketplace as they did from 2002-2005. They learned their lesson well.

My last thought: Let’s assume home price fell 5% next year. This would be the best thing ever for housing. I could stop saying this is the unhealthiest housing market post-2010 because people are forced to bid on the shelter where they shouldn’t be in that position.

However, all those who bought homes in 2020 and 2021 would still be in the same position as the one that matters the most. Their cost of shelter would be the same, and they would still be enjoying their home, neighborhood and community. Also, their wages rose again! Late-cycle lending is a risk if it follows a job loss recession; but that recession ended last year.

Housing is the cost of shelter to your capacity to own the debt it’s not an investment. It is where you live and raises your kids, and this isn’t going to change anytime soon.

Fabulous article! As a Realtor(R) I get this question all the time. This is pretty much what I’ve been sharing but not at all as eloquently nor backed by such great data. Now I’m armed! Thank you!

Economics done right should be boring and full of data. Historical trends are significant and always need to be explained to understand why something is happening. It’s not always the final result that matters most; it’s the why factors.