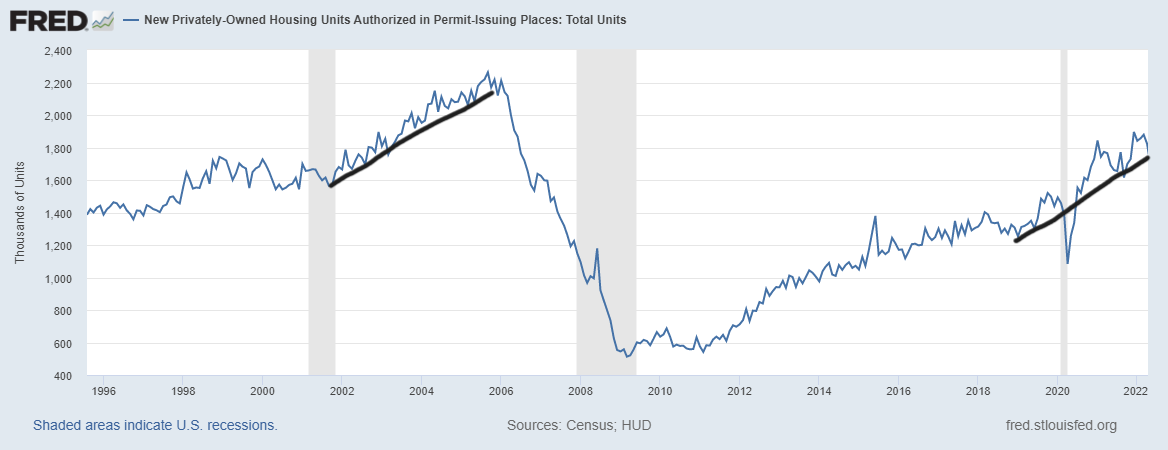

I’m raising my fifth recession red flag today based on the Census Bureau‘s May housing starts data. Housing starts showed a miss on the estimate but positive revisions. Housing starts came in at 1.549 million and housing permits came in at 1.695 million.

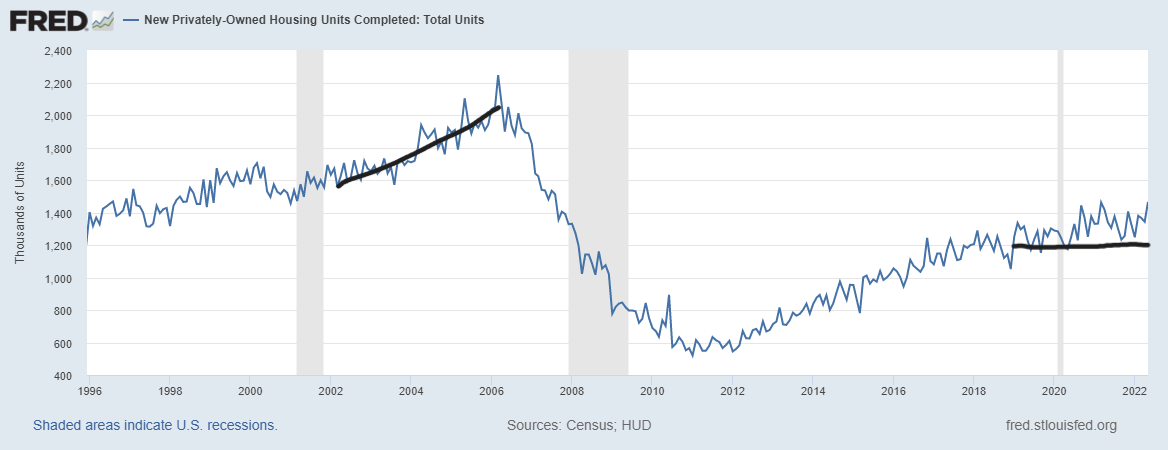

Housing completion data did grow to 1.465 million and more of the backlogged homes are finished. However, considering Wednesday’s builder confidence index and mortgage rates over 6%, it’s time to raise the fifth recession red flag, since the builders will have a tough time growing housing starts with rates this high.

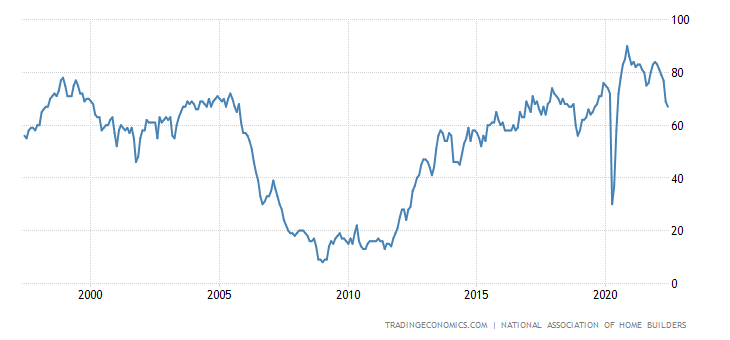

The data from the NAHB/Wells Fargo builder’s survey is always crucial because it is forward-looking, and it takes the reality of today’s market into the equation. However, the most current one doesn’t account for the higher rates we have today.

From NAHB:

From Census: Housing Permits Privately‐owned housing units authorized by building permits in May were at a seasonally adjusted annual rate of 1,695,000. This is 7.0 percent below the revised April rate of 1,823,000, but is 0.2 percent above the May 2021 rate of 1,691,000. Single‐family authorizations in May were at a rate of 1,048,000; this is 5.5 percent below the revised April figure of 1,109,000. Authorizations of units in buildings with five units or more were at a rate of 592,000 in May

Housing permits aren’t collapsing by any means, but the permits data is backward-looking. As rates rise, this will impact the builders more as they try to find buyers for current homes in cancellation. Then, they need to manage what they can or can’t sell.

From Census: Housing Starts Privately‐owned housing starts in May were at a seasonally adjusted annual rate of 1,549,000. This is 14.4 percent (±8.9 percent) below the revised April estimate of 1,810,000 and is 3.5 percent (±10.7 percent)* below the May 2021 rate of 1,605,000. Single‐family housing starts in May were at a rate of 1,051,000; this is 9.2 percent (±11.0 percent)* below the revised April figure of 1,157,000. The May rate for units in buildings with five units or more was 469,000.

While this data line isn’t crashing, the ability to grow from these levels is limited with rising mortgage rates. The story in the future is how many current homes builders can sell and when they will feel comfortable building more single-family homes. Multifamily construction is different than single-family homes. In some sense, taking away potential homebuyers fuels rental demand and keeps current renters in their homes for longer.

From Census: Housing Completions Privately‐owned housing completions in May were at a seasonally adjusted annual rate of 1,465,000. This is 9.1 percent (±22.6 percent)* above the revised April estimate of 1,343,000 and is 9.3 percent (±19.0 percent)* above the May 2021 rate of 1,340,000. Single‐family housing completions in May were at a rate of 1,043,000; this is 2.8 percent (±13.6 percent)* above the revised April rate of 1,015,000. The May rate for units in buildings with five units or more was 417,000.

Housing completions have been one of the worst stories for the housing market. The ability to finish houses has taken forever; thus, now the completion data is picking up to say hello to the falling housing starts. Historically, housing completions move with housing starts and permits data. However, supply shortages have created delays in completing homes in a timely matter. As you can see below, housing completion data hasn’t done much for many years, unlike 2002-2005. But, this data line should grow a tad more while they finish up homes that they do have buyers for.

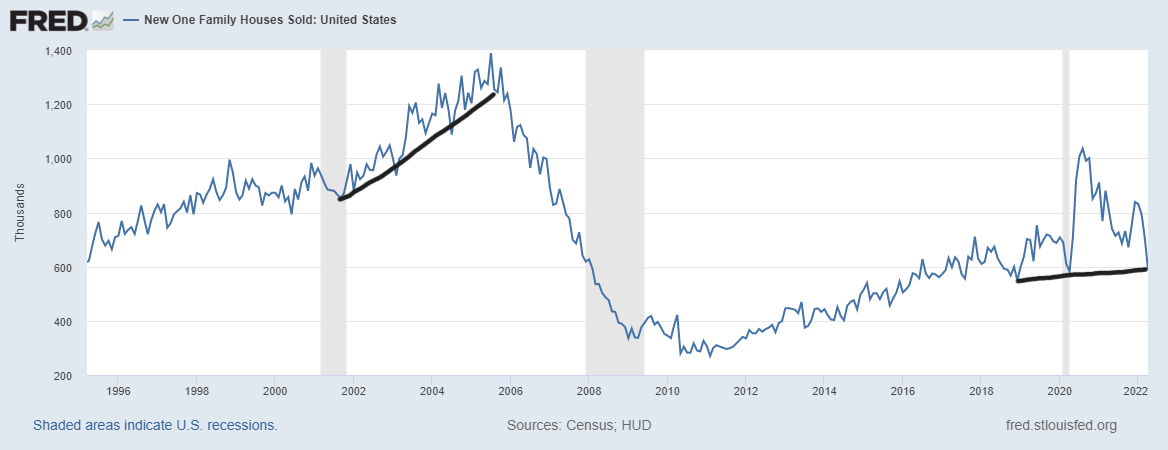

The builder’s confidence is falling, new home sales are falling, housing starts and permits are falling, while rates keep increasing. The trend is your friend until rates fall or the builders discount enough to get some buyers. One thing to note, new home sales hasn’t had a credit boom, so we are working from levels that are not that far off from historical lows. We are already below the 2000 recession levels.

The 5th recession red flag

My recession model is a progression model; it’s created to show you when we’re going into a recession and out of recession. It’s not created for glory-hound recession callers that time-stamp a date on their recession call.

At this point in 2022, we don’t see recessionary data as of yet. We have never had an active recession where employment, sales and production levels were positive. It doesn’t exist. We created many jobs in the first half of 2022 and while jobs are a lagging indicator, the other data was positive. So, a recession isn’t just two negative GDP quarters like some people believe.

Traditionally, housing starts, permits and new home sales fade into a recession. As we can see, the Federal Reserve is hiking rates to impact demand, don’t make it any more complicated than that. Back in 2018, housing starts and new home sales got hit, but we only had three recession red flags back then, plus 2020 was coming. It’s a much different backdrop now, so I’m raising the 5th recession flag.

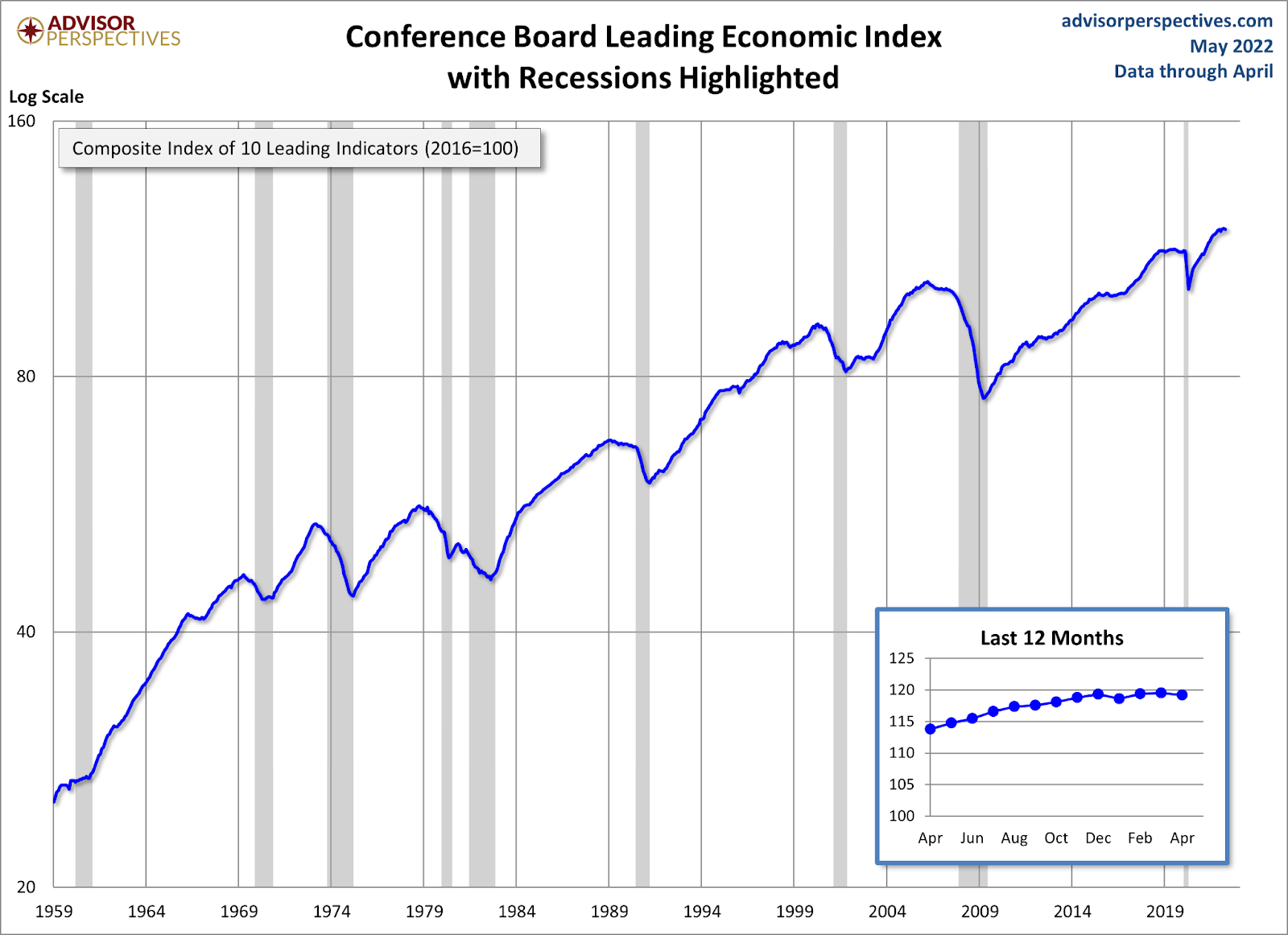

What is left — the sixth recession red flag — is the leading economic index. When this falls for four to six months, then I can go on recession watch. That is an entirely different conversation at that point. During the housing bubble years, all six flags came up in 2006, so it was sometime before the job loss recession happened.

Each economic cycle is unique, and we have to adjust to new live variables. If mortgage rates fall back, this will be a stabilizer for the housing market. Until then, we will take every housing data line and the economic data one week at a time.