The housing market experienced more volatility last week, with housing inventory dropping as mortgage rates moved higher.

Here is a quick rundown from last week:

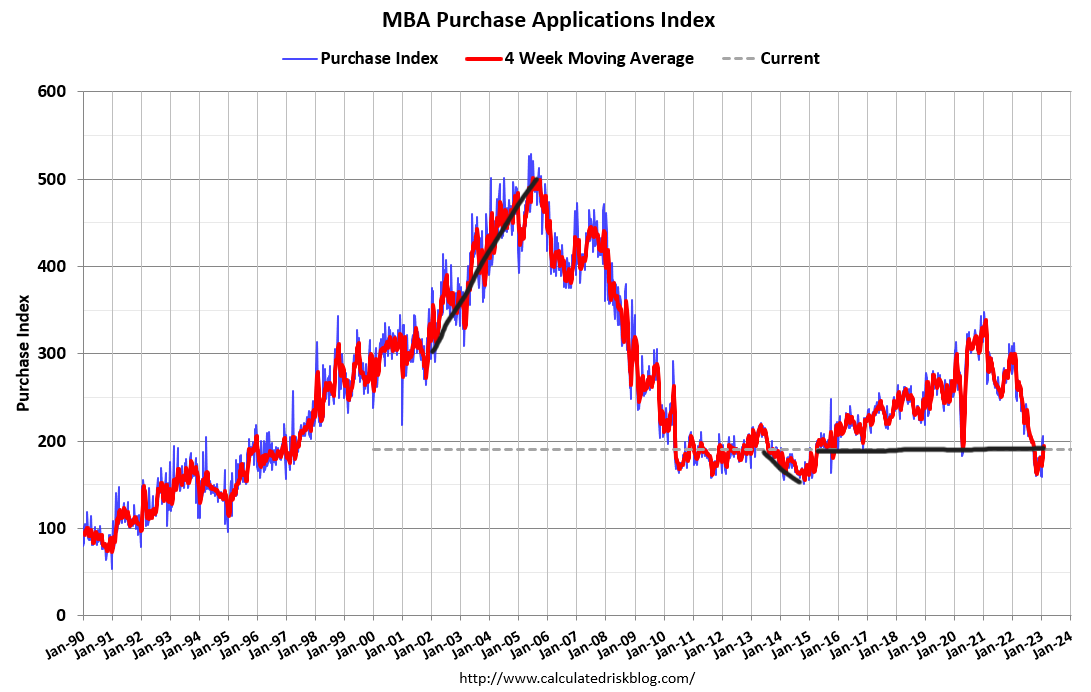

- Purchase application data had a 3% week-to-week increase. The start of 2023 has been good, considering mortgage rates have stayed above 6% most of the time.

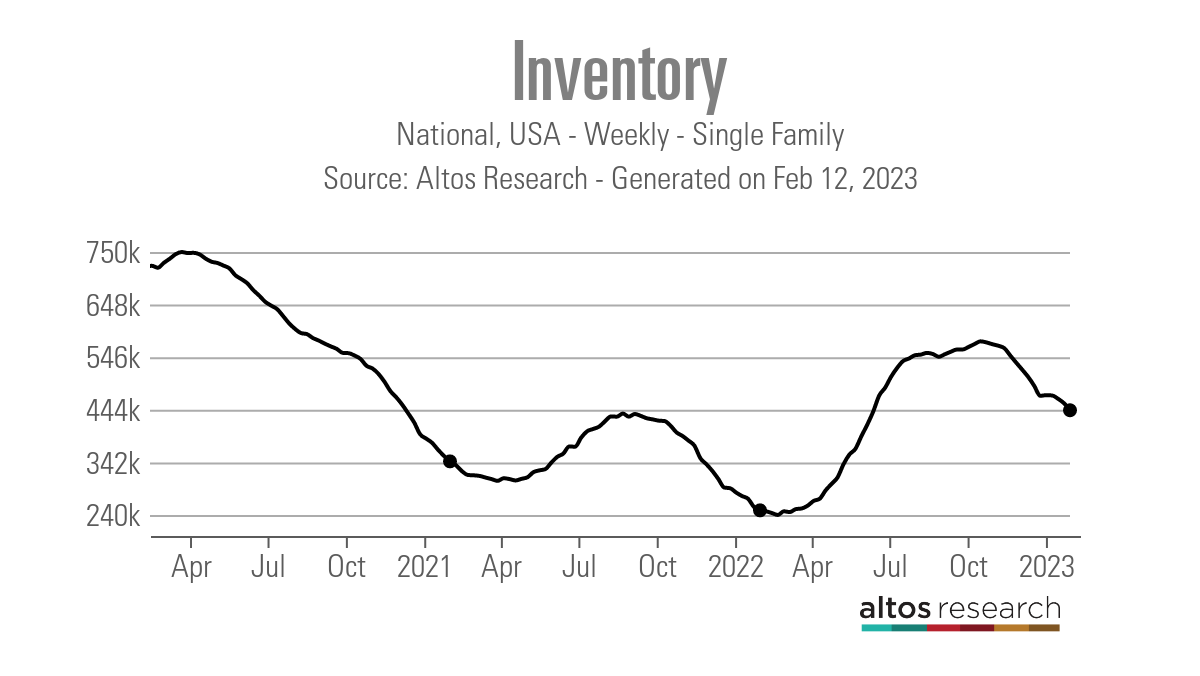

- Weekly housing inventory continues to decline, as we saw a decrease of 13,238 units, double the amount we had this time last year. However, we are working from a higher level in 2023.

- The 10-year yield jumped aggressively, continuing the decisive move from jobs Friday, and mortgage rates have moved from the recent lows of 5.99% back to 6.50%.

Purchase application data

We saw a weekly increase of 3% in purchase applications and the year-over-year data is improving, although it is still down 37% from last year. The extremely high comps that we had to deal with from October 2022 to January 2023 are coming to an end, which means that every month we should see the year-over-year declines move lower, even if the data just stay flat.

Last year, we had a historical dive in purchase application data, but recently we found a bottom and purchase apps have bounced from the lows. Since Nov. 9, when this data line started to get better, and excluding the traditional extreme slowdown the last and first week of the year, it’s been positive outside of one week. I am keeping an eye on how much growth we can get with mortgage rates over 6%.

This week, we will get a good test with the purchase application data as mortgage rates have risen recently. I am looking forward to seeing how the data reacts to higher rates. Unlike the COVID-19 recovery, which was fast and sharp, we are now dealing with a much different backdrop. Morgage rates are higher and we’re working from much higher home prices as well.

The one benefit of the housing market now is that days on the market are no longer teenagers, which means we are getting closer to a more balanced marketplace. This means buyers have more say now in the home-buying process. Finally, all the positive data we have seen since Nov. 9 looks forward 30-90 days, so the existing home sales will show better data coming up.

Weekly housing inventory

When I saw a slight increase in housing inventory in January, I got very excited because some of the demand collapse we saw in the second half of 2022 was from people choosing not to list their homes because of their fear of buying another. So, when I saw the slight inventory increase, I thought this was a good trend.

Before 2020, weekly housing inventory bottomed out in the January/February timeframe, and then the seasonal spring increase would start. From 2014 to 2016, housing inventory bottomed out in January. From 2017 to 2019, the inventory levels in January and February were very close to each other before the seasonal push higher.

However, since 2020, this hasn’t been the case — inventory has tended to bottom out a little later in the year. In 2021, inventory bottomed out in April, and in 2022 inventory bottomed out in March.

In the last two weeks, housing inventory has been declining significantly and I hope we are coming closer to the bottom of the seasonal inventory decline. Unfortunately, last week we saw a bigger decline in inventory than the previous week, as units fell by 13,238 according to Altos Research.

So I am crossing my fingers that we are getting closer to the end of the seasonal inventory decline because the last thing we want to see is bidding wars again, especially with demand working from much lower levels than what we saw in 2020/2021, and the early months of 2022. The positive aspect is that inventory is still higher than last year

- Weekly inventory change (Feb. 3-Feb. 10): Fell From 456,990 to 443,416

- Same week last year (Feb. 4-Feb. 11): Fell from 255,662 to 249,161

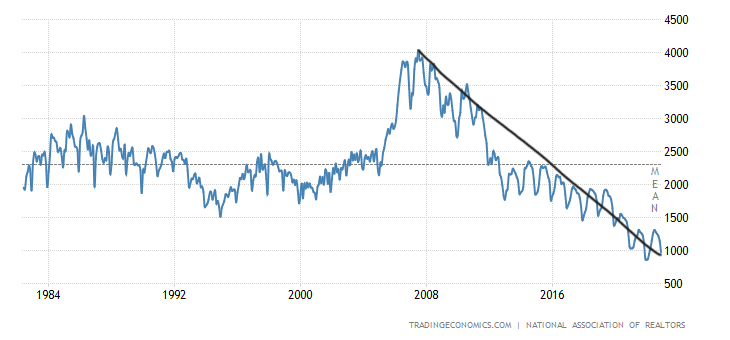

Because I could see that housing demographics were going to be good in the years 2020-2024, I really didn’t want to see inventory break to all-time lows during this period. This reality created my fear of home prices overheating, which they did, and once mortgage rates rose, the housing market took an extreme affordability hit. Last year, we had a historical dive in housing demand and didn’t get much inventory.

Unfortunately, we have a good shot of the next existing home sales report showing even lower inventory levels than the 970,000 level we are dealing with today. This means 2022 and 2023 are the only times in recent history where the NAR active listing data is under 1 million.

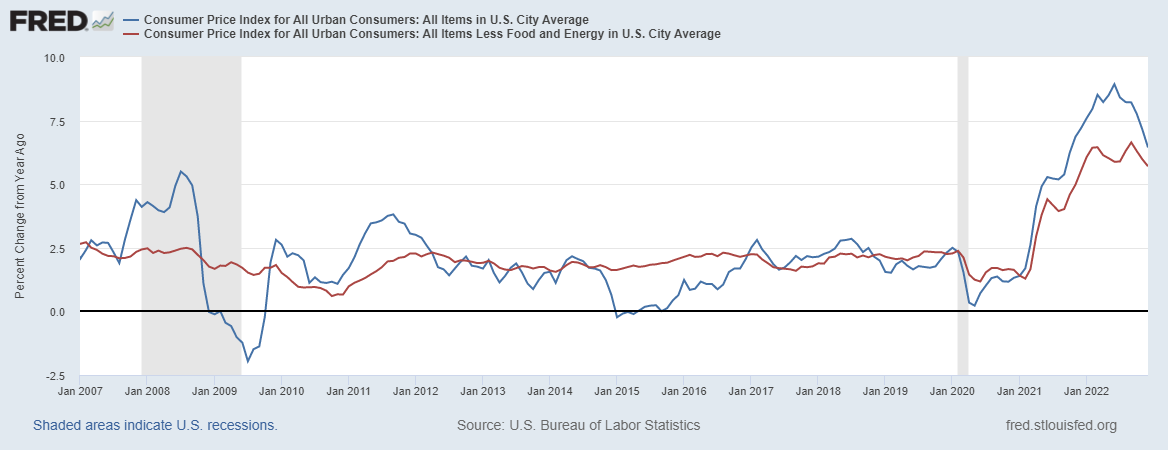

10-year yield and mortgage rates

In my 2023 forecast, if the economy stayed firm my 10-year yield range was between 3.21% and 4.25%, equating to mortgage rates staying in a range of 5.75% to 7.25%. For some time now, I have discussed how it would be hard to break under 3.42% with follow-through bond buying, meaning mortgage rates would fall further. The market made a few attempts to break that level, but now bond yields have reversed higher.

The question this week with the CPI report data being released, is whether we will see a W forming in this chart, which would mean bond yields head back to 4.25%, or whether the downtrend continues. Over time, the growth rate of inflation will cool down once rents get accounted for in a more real-time fashion.

Also, part of the 2023 forecast is that if the labor market breaks, the 10-year yield could get to 2.72%, which would mean mortgage rates in the low 5% range. And if the spreads get better, we could even have a 4-handle on mortgage rates. For now, though, the labor market is still solid.

The week ahead

This will be an exciting week for economic data, bonds and housing. First and most important, this week’s purchase application data is vital. It will be the first apps data amid a half a percentage move higher in mortgage rates, and the next few weeks will be critical, too, if rates stay at 6.50% or head higher. Remember, you should prioritize numbers over people; if the tracker data goes negative, you go with data rather than a personal belief.

The big move for rates should be the Consumer Price Index report this week. If it’s hotter than expected, we could see bonds act negatively to that report. Also, this week we have jobless claims, retail sales, Producer Price Index inflation, the homebuilders’ confidence survey, housing starts and the Leading Economic Index!

It’s going to be a busy week with economic data that can move the bond market and mortgage rates. One thing is certain from the data: mortgage rates heading lower, even to just 5.99%, shifted the housing market, which is something to remember as we go forward

Why is there such a difference is Alto’s inventory levels (443,416) and NAR’s number (around 1,00,000)? Is one just single family vs single family and multifamily or is there another variable.