The Consumer Price Index data released Wednesday showed again that the breakaway 1970s-style inflation is not happening, even with an expanding economy and an unemployment rate under 4%.

The headline inflation data came in lower than anticipated. While we have made progress in cooling down the inflation data, which is running into tough year-over-year comps (and will for the rest of the year) don’t expect the Fed to pivot anytime soon.

I believe the Federal Reserve won’t pivot until the labor market breaks. Pivoting doesn’t mean they’ll cut rates, it just means they’ll change their language describing the economy. They’ll only cut rates when jobless claims are above 323,000 on a four-week moving average and we aren’t there yet.

The Federal Reserve has said time and time again they want the labor market to break, and they will only be satisfied once the unemployment rate goes much higher than it is today. This is why they constantly forecast a job-loss recession with their higher unemployment rate forecast, and some Fed members talk about sending short-term rates much higher. I recently talked about this on CNBC.

Even though the headline inflation report was lower than estimates, the 10-year yield didn’t have too much of a response today. As I am writing this article, it’s trading at 3.42%.

While the 10–year yield, mortgage rates and inflation look about right for my 2023 forecast, let’s not forget the real prize the Federal Reserve has in store: they want you to lose your job and that is why they keep forecasting a job-loss recession with a higher unemployment rate.

Even though the Fed said they’re tracking core Personal Consumption Expenditure (PCE) data over three, six and 12-month timeframes and their forecast shows that the data there should improve, it doesn’t matter. The Fed is so afraid of the 1970s that the fear is more important than anything else.

Even when they say rate hikes have a 12-18 month lag, meaning that the full effect of these aggressive rate hikes won’t hit the economy until later, they’re not waiting for that lag. They talk about more rate hikes, and keeping rates higher for longer because they believe this is the most effective way to beat inflation — by creating more labor supply through job losses. This is why they still don’t care that housing is in a recession.

Let’s look at the internal data in this CPI report and find some good nuggets to discuss.

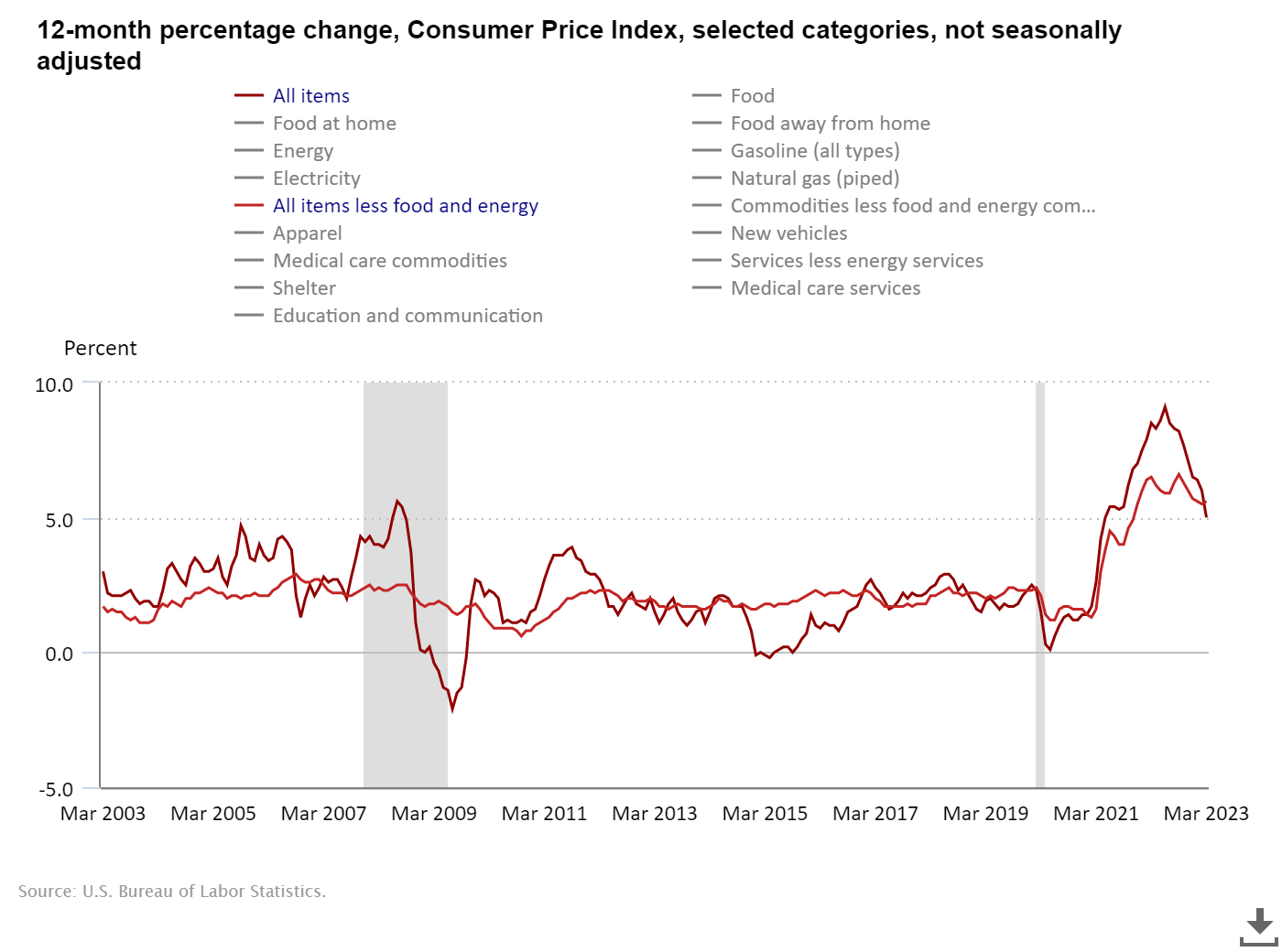

From BLS: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.1 percent in March on a seasonally adjusted basis after increasing 0.4 percent in February, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 5.0 percent before seasonal adjustment.

As we can see in the chart below, the year-over-year inflation growth rate peaked a while back, and it’s tough to push this higher than the recent peak unless oil, food, and rent take off again.

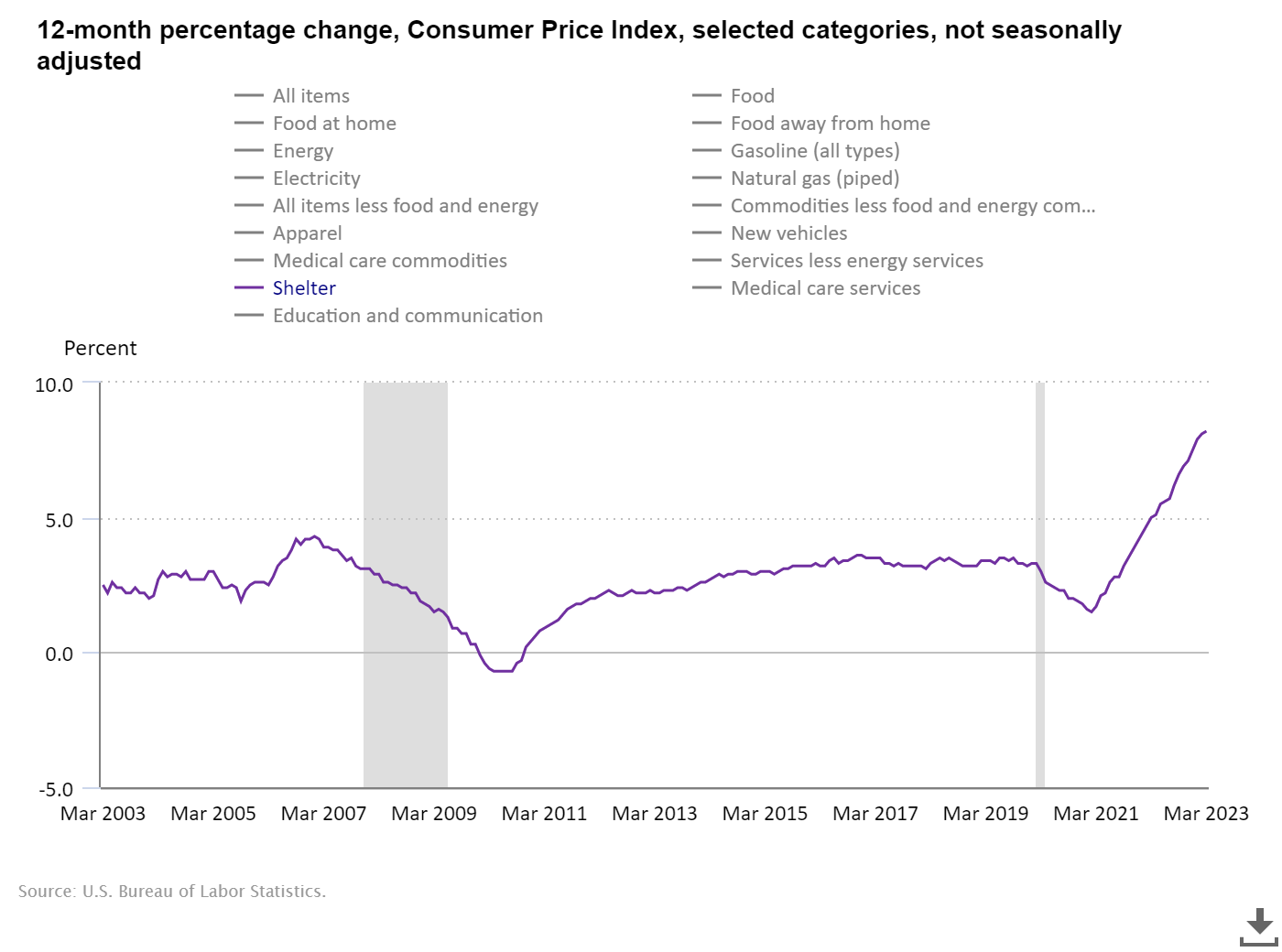

One of the reasons didn’t see breakaway inflation during the housing bubble years is that rent inflation was tame back then. This hasn’t been the case recently, and 44.4% of CPI is shelter inflation. We all know the lag of shelter in the CPI data; this is something I covered on CNBC last September. I stressed that by January and February, we would see the growth rate of shelter inflation fading, but it would take time to hit the CPI data.

We are getting to the point where the year-over-year comps and the lag will start to show the growth rate of inflation declining and catching up with the current market reality, which means the 1970s inflation thesis will suffer yet another blow.

We can’t have entrenched 1970s inflation because, back then, rental inflation was booming; I mean, it was massive before, and wage growth was scorching back then too. As you can see below, if shelter Inflation is about to start its reality tour for the next 12 months, it will be hard to dance to disco music again.

Also, in the last jobs report, year-over-year wage growth is falling, all with a tight labor market still.

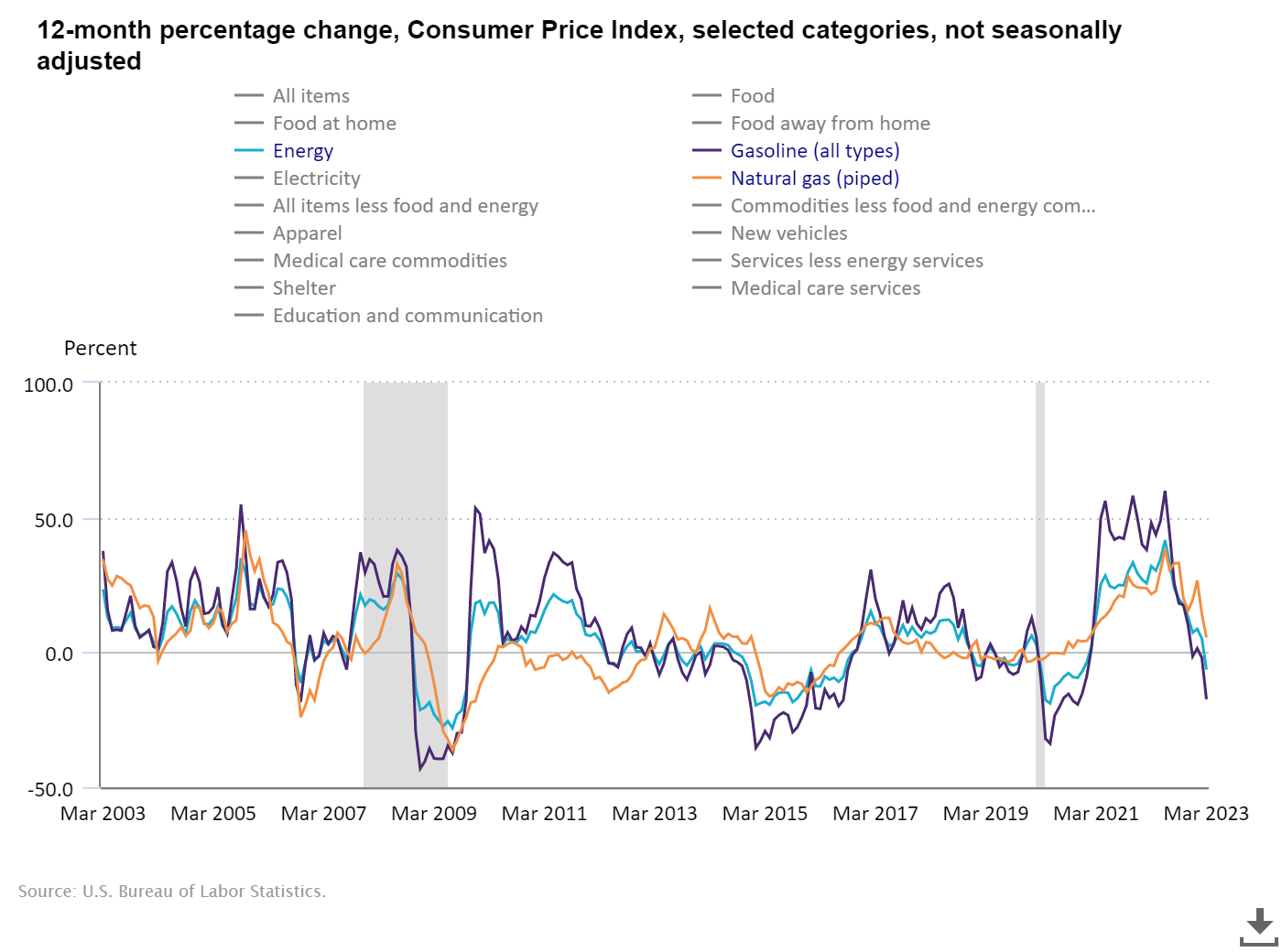

It’s tough to get 1970s inflation unless wage growth, energy, food and shelter all move much higher together, which isn’t happening. Energy inflation is falling as the comps year over year are challenging. The Russian invasion pushed energy prices much higher.

We had higher oil prices from November 2010 to September 2014 without CPI inflation breaking out because shelter inflation and wage growth were tame back then. The chart below shows the period I discussed with oil prices, while core CPI was very tame.

Even though the CPI inflation data came in lower than anticipated on Wednesday, we saw no significant drop in the 10-year yield. Mortgage pricing did get a tad better this morning, as the last two days’ pricing was pretty bad.

With the 10-year yield still trading in the 2023 forecast range of 3.21%-4.25%, the bond market has acted remarkably in line with my view that everyone is waiting for the labor market to break, especially the Federal Reserve, before we make another aggressive move lower in the 10-year yield.

We all know that shelter inflation will fade over the next 12 months, making it mathematically impossible to have another burst in inflation. The housing market needs bond yields to go down and the spreads between the 10-year yield and 30-year mortgage rate to get better to get more traction.

Purchase application data also came out on Wednesday and it was positive 8% week to week, which means 2023 so far has had more positive purchase application data than negative.

Now, imagine a housing market with mortgage rates in the low 5% range, not in the mid 6% range. That would change a lot of the dynamics in the housing market and put the sector on more solid footing. However, until then, we will track all the economic data one day and one week at a time.

Thanks, Logan. As always, your content is so valuable to us as Realtors. We are hoping and praying that as 30 year rates hit the low 5’s that it will also spark more Sellers to jump in and help to give us inventory to sell as we are back to multiple offers (south Orange County, CA), begging & pleading and leaving a few arms & legs with every offer for a client wanting their dream home. Happier days ahead we hope. Maybe someday the Fed will start to pay attention to what you’ve been saying for over a year!