Have homebuilders reached their limit on how much they can lower mortgage rates to boost demand? Today we got the housing starts data, which was a beat of estimates, but total housing activity isn’t booming here.

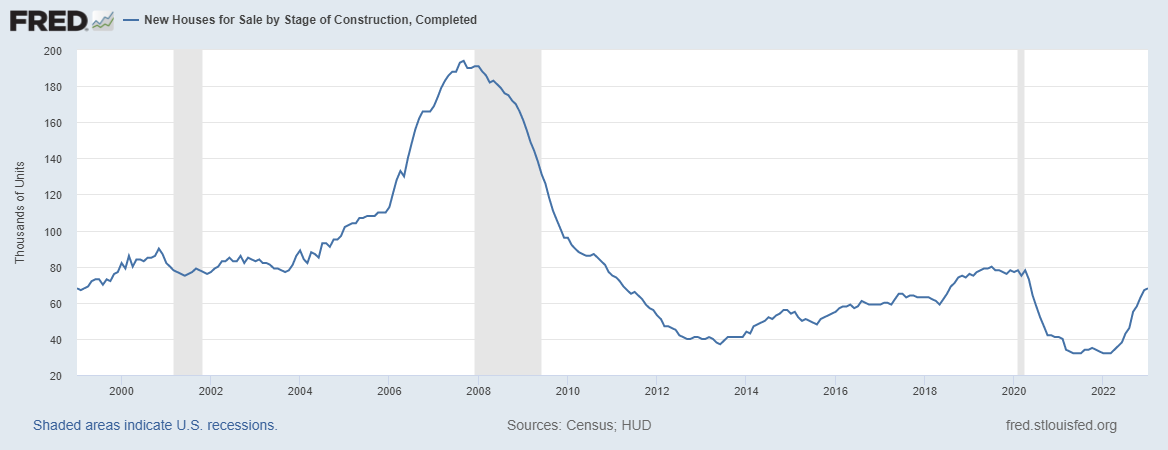

I firmly believe that the builders can’t solve the housing inventory situation when it comes to single-family units because they will simply not provide enough. As shown below, we currently have only 72,000 new homes for sale.

This data is returning to more normal levels, but even during the worst days of the housing bubble crash, we never got to 200,000 homes. In a country with over 335 million people (and over 156 million people working), 72,000 isn’t going to do much to move the needle on inventory.

From Census:

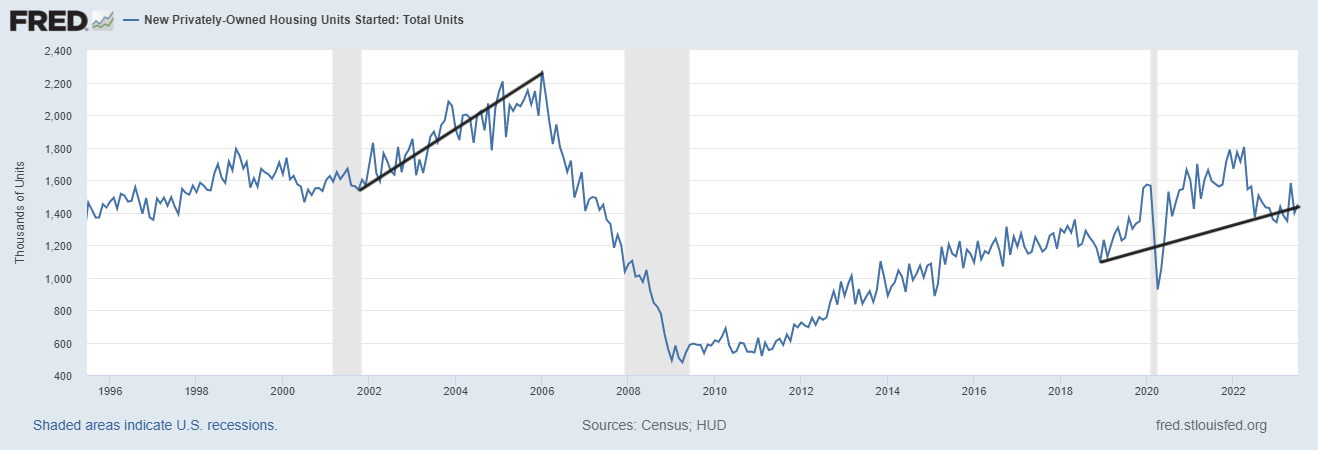

Housing Starts: Privately‐owned housing starts in July were at a seasonally adjusted annual rate of 1,452,000. This is 3.9 percent (±16.0 percent)* above the revised June estimate of 1,398,000 and is 5.9 percent (±16.1 percent)* above the July 2022 rate of 1,371,000. Single‐family housing starts in July were at a rate of 983,000; this is 6.7 percent (±13.0 percent)* above the revised June figure of 921,000. The July rate for units in buildings with five units or more was 460,000.

As you can see in the chart below, housing starts have stabilized as new home sales are still showing year-over-year growth, but starts aren’t exactly booming. We must remember that the homebuilders still have a sizable backlog of houses they haven’t started to build yet.

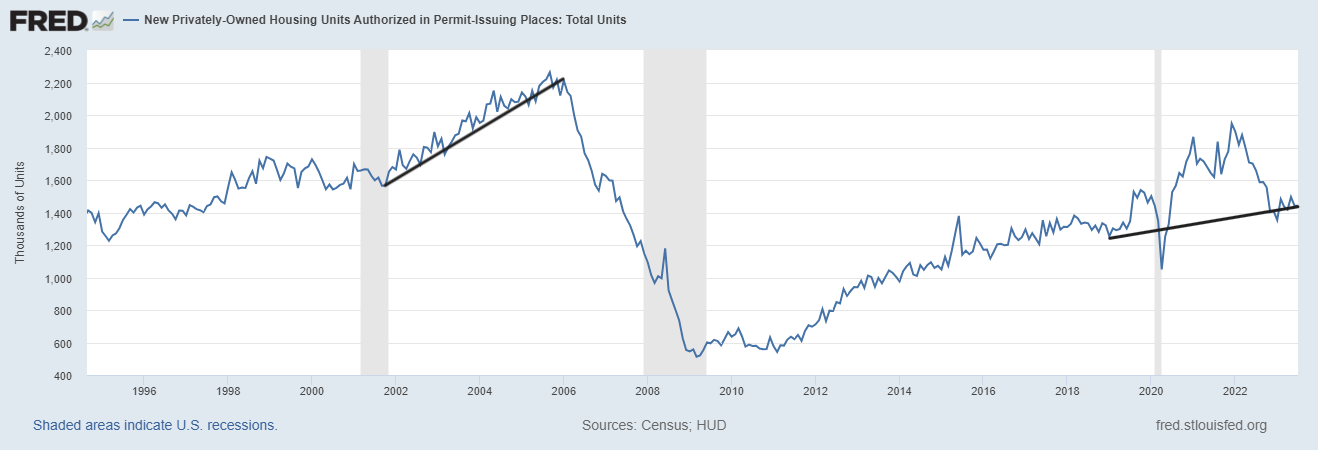

Building permits: Privately‐owned housing units authorized by building permits in July were at a seasonally adjusted annual rate of 1,442,000. This is 0.1 percent above the revised June rate of 1,441,000, but is 13.0 percent below the July 2022 rate of 1,658,000. Single‐family authorizations in July were at a rate of 930,000; this is 0.6 percent above the revised June figure of 924,000. Authorizations of units in buildings with five units or more were at a rate of 464,000 in July.

Housing permits have also stabilized from their fall, and we are seeing more single-family permits issued, but it’s not a big move, as the chart below shows.

How long will the builders keep their advantage?

Why am I focusing on mortgage rates now? Well, mortgage rates are now at the high end of my forecast range for 2023, and we are still dealing with a stressed mortgage market. Over the last year the builders have grown yearly sales by offering lower mortgage rates, which they could do because they had good enough profit margins.

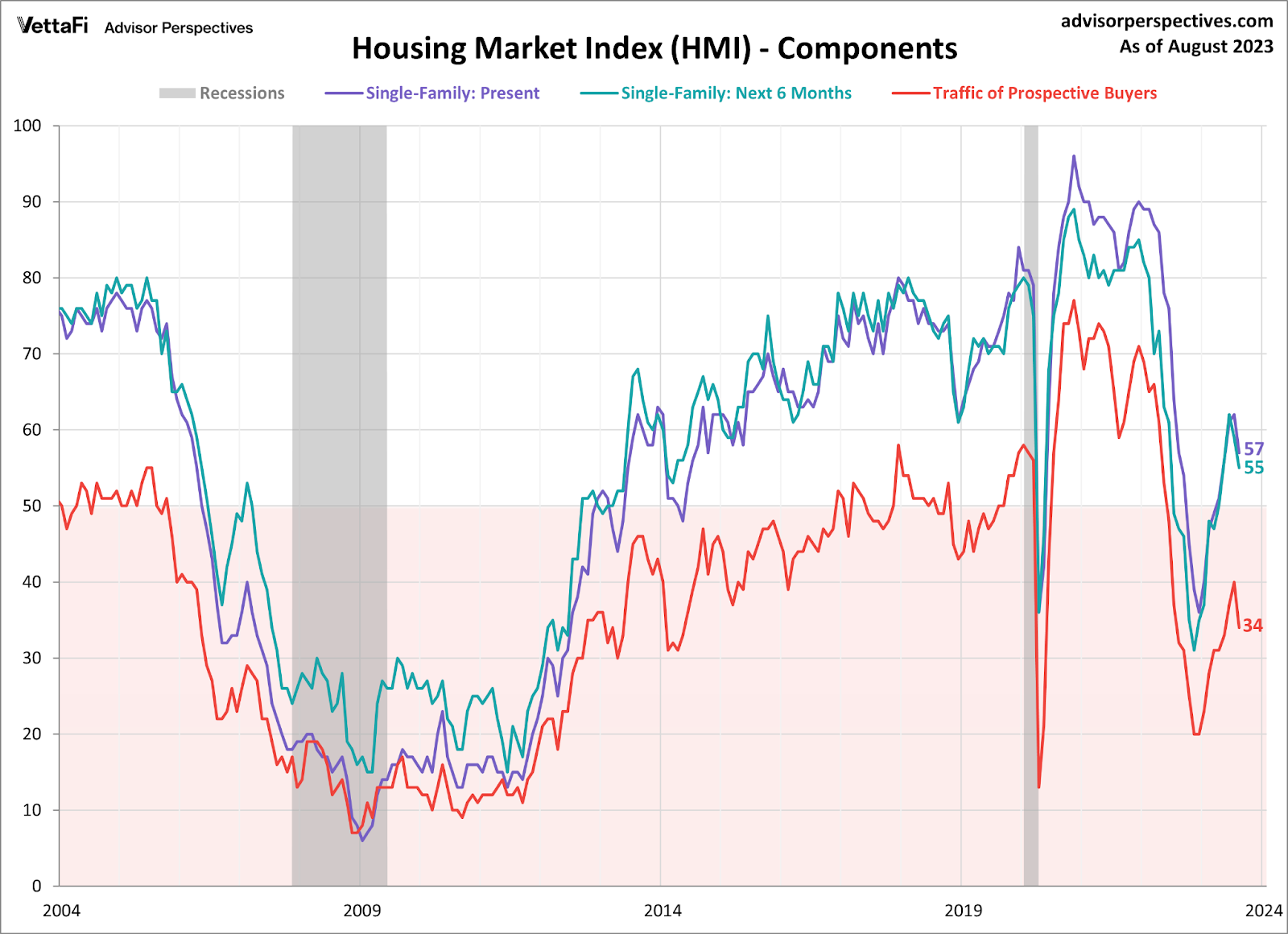

However, for the first time this year, they have expressed concern about their future in the builder’s confidence index: back-to-back declines in the forward-looking six-month data line from the builder’s survey. The headline data also fell for the first time in a long time, but last month the forward-looking data line declined even with the positive print.

Forward-looking housing data for the builders was positive for many months, but in the last two months, that changed, so the builders are more cautious about their future. What has changed is that mortgage rates have stayed higher for longer over the last two months, so we have a direct correlation to higher rates here.

I am a big fan of the HMI data because the builders know more than anyone else what they can and can’t do. You just have to believe in this survey and keep an eye out for whether higher rates are starting to hit their confidence metrics looking ahead. I see cracks in the system that warrant close monitoring because this data line can be very choppy sometimes, but if we get a string of these lines, it makes a trend.

For now, I am keeping a watchful eye on this because if the builders are having issues looking ahead, then the housing market, in general, will be in a slow phase as well. As we saw today with the purchase application data, we aren’t crashing in sales like in 2022, but we aren’t growing either.