What is HMDA?

The Federal Financial Institutions Examination Council released the Home Mortgage Disclosure Act (HMDA) data for 2015 at the end of September. HMDA data is considered the most comprehensive report on mortgage originations. For 2015, 6,900 institutions reported 14.3 million loan records. This makes HMDA an important data source even though it is released with a nine-month lag.

The state of the mortgage and housing market for 2015

The most important story is that the mortgage origination market continued to benefit from an improved housing market in 2015. Higher home sales, rising home prices and more homeowners in the housing market contributed to a stronger purchase origination market. But growth has been unevenly distributed across different parts of the country, with faster growth centered in the West and Southeastern parts of the country, reflecting faster demand growth in these regions.

The strong momentum behind the multi-family housing market also continued in 2015, as growth in multi-family purchase originations eclipsed growth in the single-family segment. With the collapse in oil prices in late 2014, housing markets in oil-producing states saw slower growth, and that also slowed the mortgage origination markets in those states. On the refinance side, the unexpected drop in mortgage rates in early 2015 helped to revive refinance activity.

But because many eligible borrowers had already refinanced at similar rates during the 2012-2013 refinance boom, the impact of lower mortgage rates was much smaller in 2015. Finally, rising home equity and lower interest rates created favorable conditions for home improvement lending in 2015, allowing homeowners to start overdue home improvement projects.

With this backdrop, here are my top five takeaways from the new HMDA data set:

1. Mortgage originations benefited from a stronger housing market in 2015.

The housing market experienced strong overall growth in 2015—boosted by a strong job market and lower mortgage rates. Home sales, including both new and existing homes, grew by approximately 7% to 5.76 million. Housing supply tightened in many markets across the country, driving home prices higher. Nationally, home prices grew by around 6% in 2015, according to the Federal Housing Finance Administration’s Purchase Home Price Index.

Higher home sales and rising home prices lifted both the number of purchase loans and the average loan balance. Purchase originations increased by 18% to $872 billion in 2015, the highest volume since 2007. The number of single-family home purchase loans increased by 13%, while the average size of purchase loans increased by 4%. The number of home purchase loans grew almost twice as fast as home sales (13% vs. 7%), suggesting that the percentage of mortgage-financed home sales has been on the rise, while the percentage of cash sales has been falling. This is an important aspect of the housing recovery, suggesting that there were more “normal” home sales in 2015. We believe this trend will continue.

Another indicator that the housing market is improving is the increased proportion of homeowners in contrast to investors. The percentage of owner-occupiers in purchase originations grew from 89% to 89.4%, reaching its highest level since 2009 and 2010, when the first-time homebuyers’ tax credit temporarily boosted the percentage of homeowners in the purchase market.

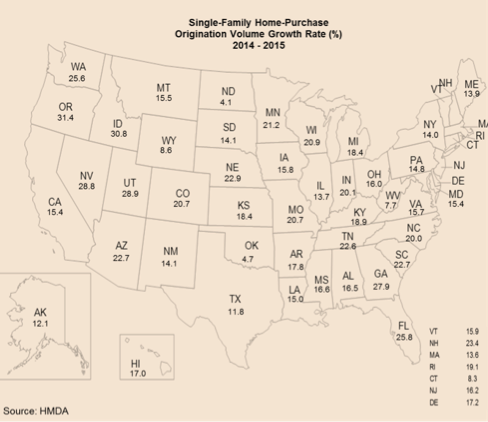

2. Purchase origination growth was uneven at the state level.

Single-family purchase originations grew in all states during 2015, but growth was centered in the Western and Southeastern parts of the country, where purchase origination volume grew well over 20%. A notable exception here is California, which saw purchase origination growth slightly below the national average of 18% on weaker home sales growth. With the collapse in energy prices in late 2014, energy-producing states saw a general slowdown in purchase origination growth, with smaller states such as North Dakota and West Virginia reporting some of the weakest growth rates in the country.

3. There was stronger momentum in the multi-family market.

The strong growth in the multi-family housing market has been an important feature of the recovery. Multi-family housing did not experience the same magnitude of overbuilding in the lead up to the housing crisis, and has benefitted from the shift toward renting. Between 2011 and 2014, while single-family purchase origination volume grew by around 55%, multi-family volume grew by over 190%. That trend continued in 2015, with multi-family purchase origination volume growing 35% over 2014 levels, twice as fast as growth in the single-family segment.

4. Lower mortgage rates boosted refinance origination volume, but its impact was not as powerful as in 2012-2013.

Refinance origination volume increased by 56% to $768 billion in 2015. The 30-year fixed mortgage rates dropped below 4% in 2015, creating a small refinance boom. But because many eligible borrowers had already refinanced at similar rates during the 2012-2013 refinance boom, the impact of lower mortgage rates was much smaller this time around. Refinance volume in 2015 was only around half the size of 2013. We expect refinance volume in 2016 to exceed the 2015 level because rates have declined further. But unless rates moved even lower in 2017, we expect refinance volume to decrease.

5. Mortgage lending going into home improvement was beginning to increase.

Eight years after the Financial Crisis, housing starts remain well below the historical trend of 1.5 million units a year. This prolonged downturn in new home construction means that housing stock has become older, requiring more repairs and home improvement work. Historically, many homeowners use home equity as a way to finance these projects. But mortgage lending for home improvement projects between 2009 and 2014 had been disappointing. Home improvement lending averaged just $30 billion a year, significantly below the $100 billion mark in 2006. But rising home prices since 2012 means that there was more home equity for homeowners to tap. In addition, mortgage rates have remained low, making it cheaper to finance home improvement projects. These favorable conditions helped boost home improvement lending by over 50% in 2015 to $49 billion, accounting for about one-third of the home improvement spending that year.