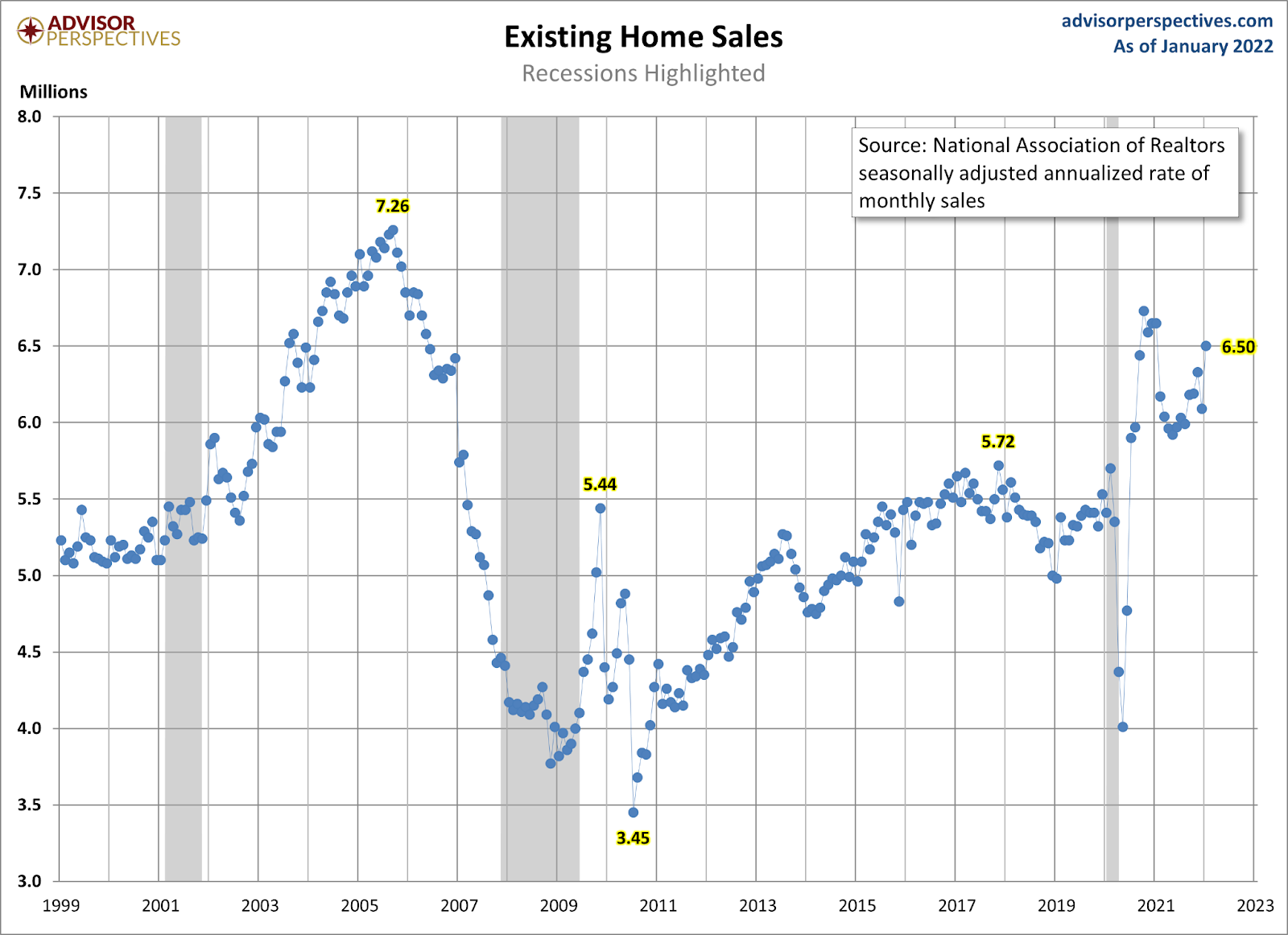

The National Association of Realtors reported that existing home sales for January came in as a big beat at 6.5 million. This is well above my peak sales ranges for 2022, as the sales trend forecast was between 5.74 million and 6.16 million. So, we have started the year off on a stronger-than-expected note. I believe there might have been some spillover demand from December into January as the December number came in lighter than expected. This might explain the big beat in estimates.

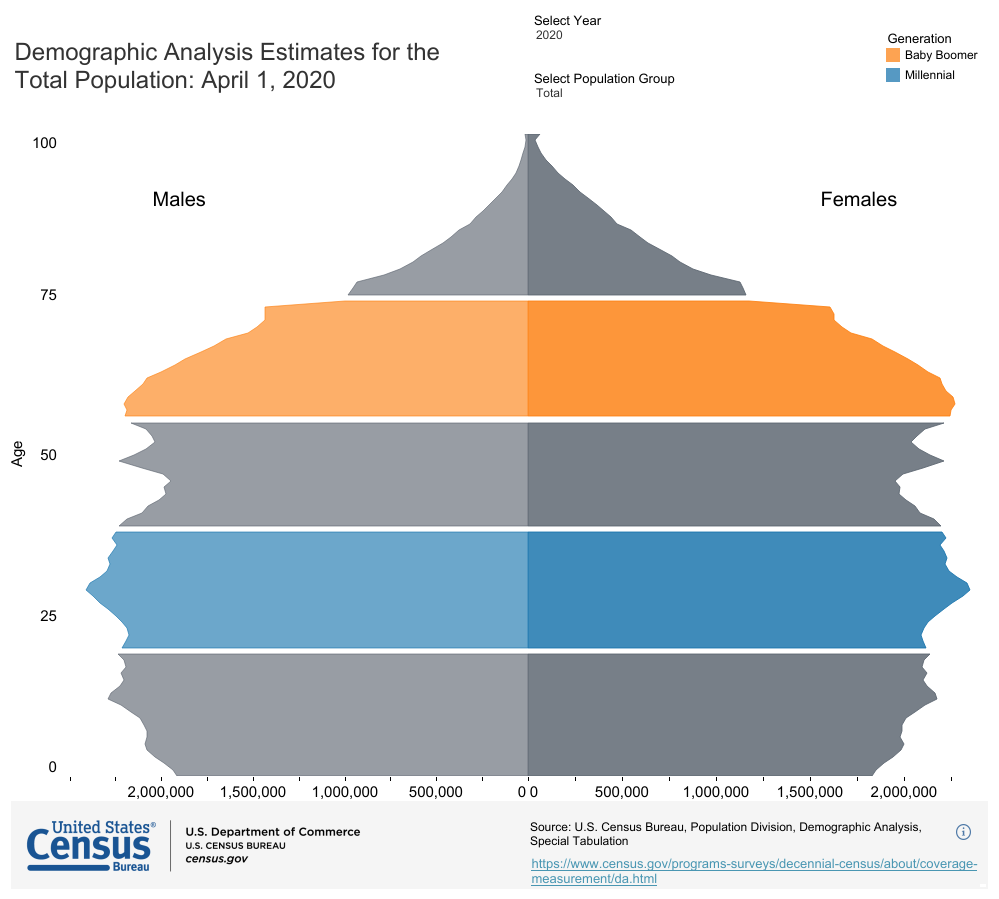

Existing home sales ended 2021 on a more positive note as mortgage demand picked up toward the end of the year. Mother demographics is flexing her muscle during this period as the most significant housing demographic patch ever recorded in U.S. history — ages 28-34 — are coming into the peak homebuyer median age of 33. When you add move-up, move-down, cash and investor buyers into the mix, you will have steady replacement buyer demand from 2020-to 2024.

Total home sales for new and existing homes should be at 6.2 million or higher during this unique five-year period. This couldn’t have happened from the years 2008-2019 as the population was both too young and too old to get total net demand of over 6.2 million.

Looking at the chart below, you can see that in 2020, there is a bump in the number of people about to hit their peak home-buying age (look at both sides of the blue bar).

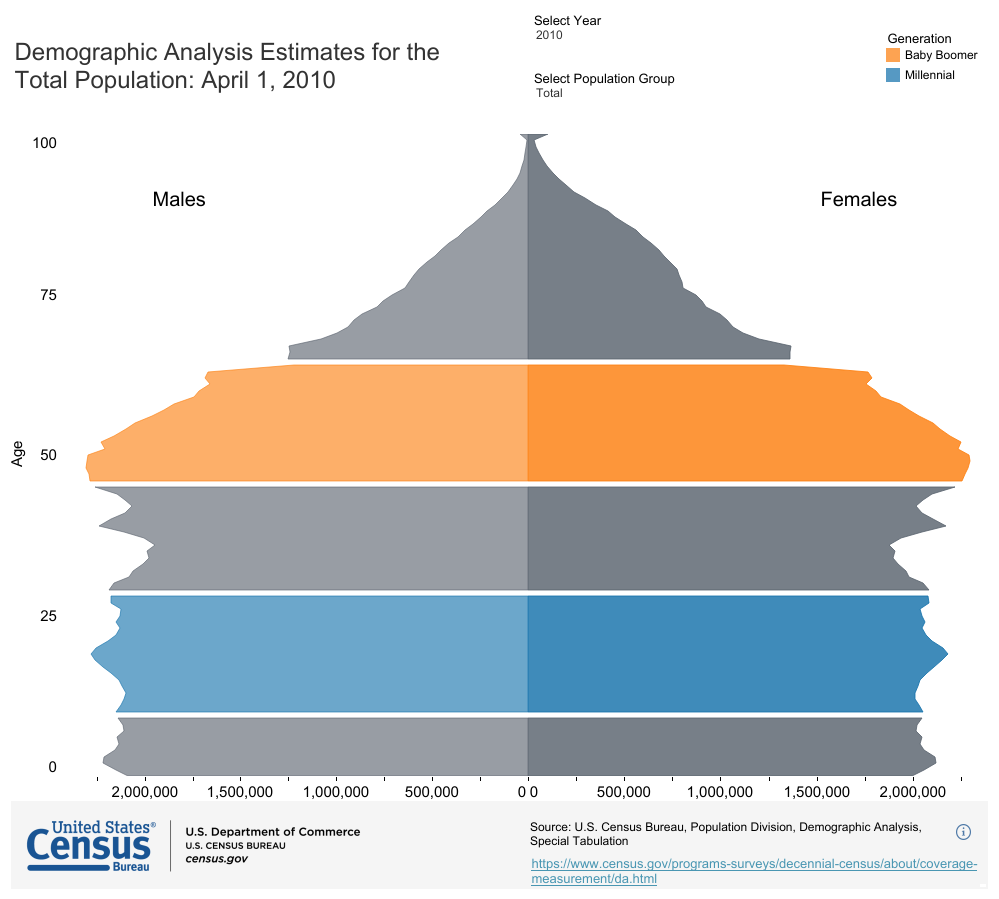

Compare that to the 2010 demographic chart below, when that blue bump was still too young to kick in. Millions of people buy homes each year, so demographics and mortgage rates are the two fundamental drivers of housing, and in the years 2020-2024, both are favorable for housing demand. When you look at housing this way you can see why we have more sales in 2020 and 2021 than any single year from 2008to 2019.

All of this isn’t great news, of course. The downside to having the best housing demographics with the lowest mortgage rates ever means home prices can get overheated. In a recent interview on Bazaar, I went into the details of how we got into this housing dilemma.

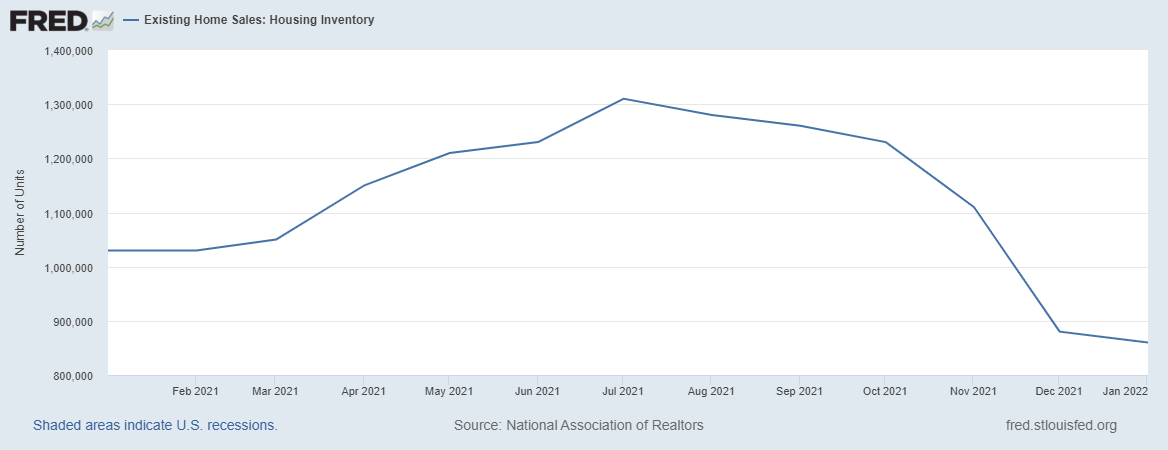

One of the reasons I keep saying this is the unhealthiest housing market post-2010 is that home-price growth is entering year three of my five-year housing demographic patch timeframe with harmful home-price growth. Also, we are starting the year with fresh new all-time lows in inventory.

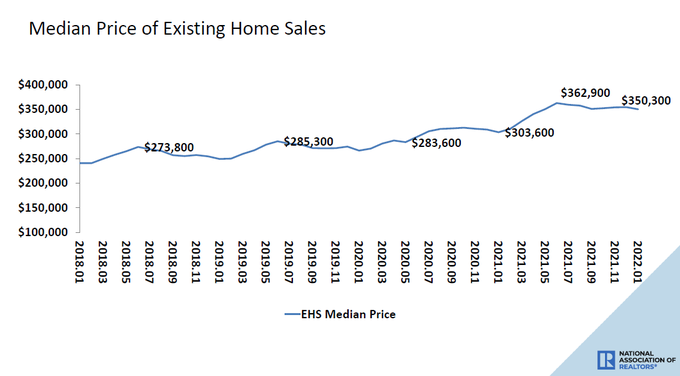

Per NAR Research: In January, the median existing-home price for all housing types was $350,300, up 15.4% from January 2021 ($303,600), as prices rose in each region.

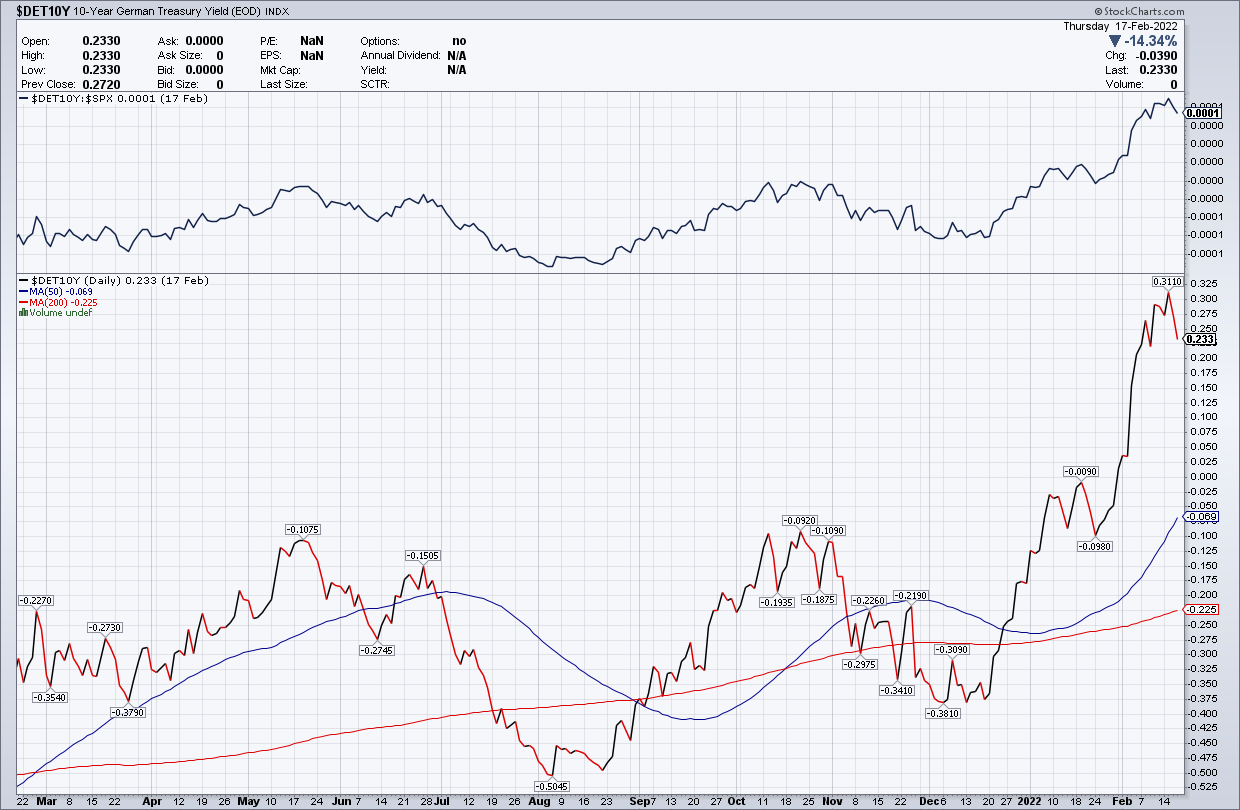

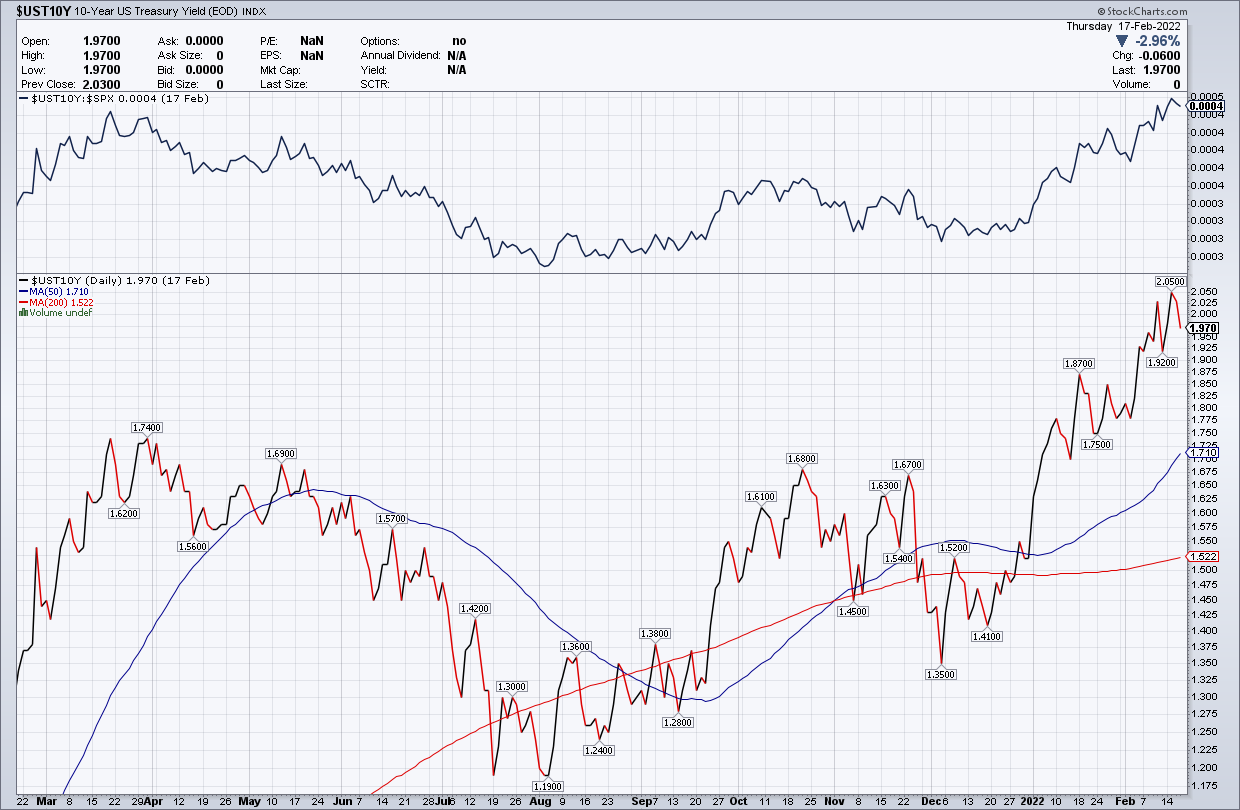

When people ask why it seems like I am rooting for higher rates, it’s because I am. Higher rates do provide a stabilizing impact when prices get too hot. The only issue now is that it’s been hard to get the 10-year yield above 1.94% post-2019. However, my 2022 forecast did create a pathway for this to happen. “We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies to function altogether in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.”

The 10-year yield of both Japan and Germany have noticeably risen this year. This was a must for our 10-year yield to get over 1.94% and even have the discussion of 4% – 4.5% mortgage rates.

However, as I am writing this right now, the 10-year yield is 1.927%. For us to have 4% plus mortgage rates with duration, we need a few things to happen. We need the economic data here to stay firm and we need global yields not to head back lower, such as we’ve seen recently with Germany and Japan. As you can see, it’s not only been hard to get 1.94% on the 10-year yield, but to rise and stay above it with duration.

Higher mortgage rates will create balance in U.S. housing, something I talked about on the HousingWire Daily podcast this week.

Now, total inventory levels will rise as they do every spring and summer, just as they fade in the fall and winter. The fundamental goal is to get total inventory levels between 1.52 – 1.93 million to stabilize the market. I know this is historically low inventory, but the market won’t have the price gains in recent years. Housing inventory is at 860,000 for a country where the total population is running over 322 million today.

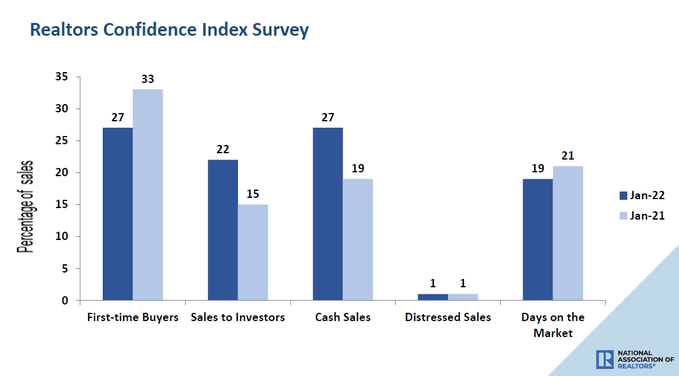

The real goal is to get the days a house is on the market to grow. Preferably 30 days or more creates balance. As you can see below, we are far from that type of housing market. I hope higher rates can generate more days on the market, so people have more choices.

Per NAR Research: First-time buyers were responsible for 27% of sales in January; Individual investors purchased 22% of homes; All-cash sales accounted for 27% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 19 days.

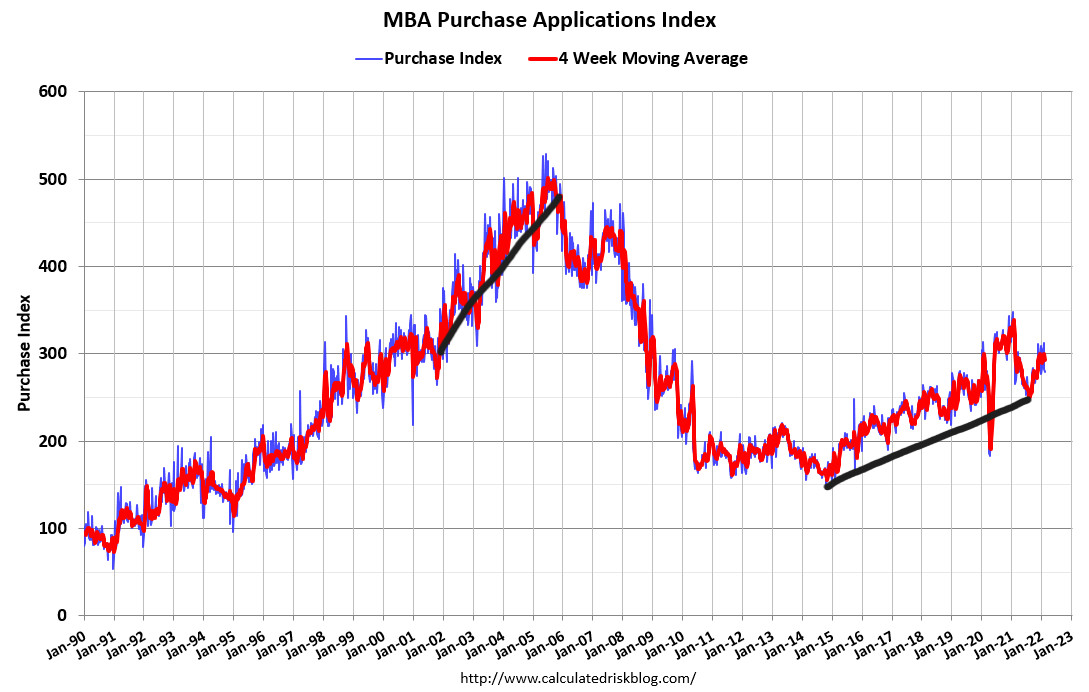

So far, with the purchase application data, I would say demand is stable. We never had a credit boom in housing over the past decade; it was always slow and steady. The recent uptick in buyers in 2020 and 2021 makes sense when considering the demographic patch in 2020-2024. However, I would not label this housing cycle a sales credit boom by any means.

While the headline existing home sales report beat expectations, I believe some of the demand for December, which came in lighter than expected, spilled into the January data. All in all, when existing home sales are trending between 5.74 million and 6.16 million, the market looks just right to me. When it’s over 6.16 million, I would consider it a better-than-anticipated year in demand. The current existing home sales level of 6.5 million is a noticeable beat in my eyes, so if the existing home sales data does trend lower in the upcoming months, that would seem more in line with my 2022 forecast.