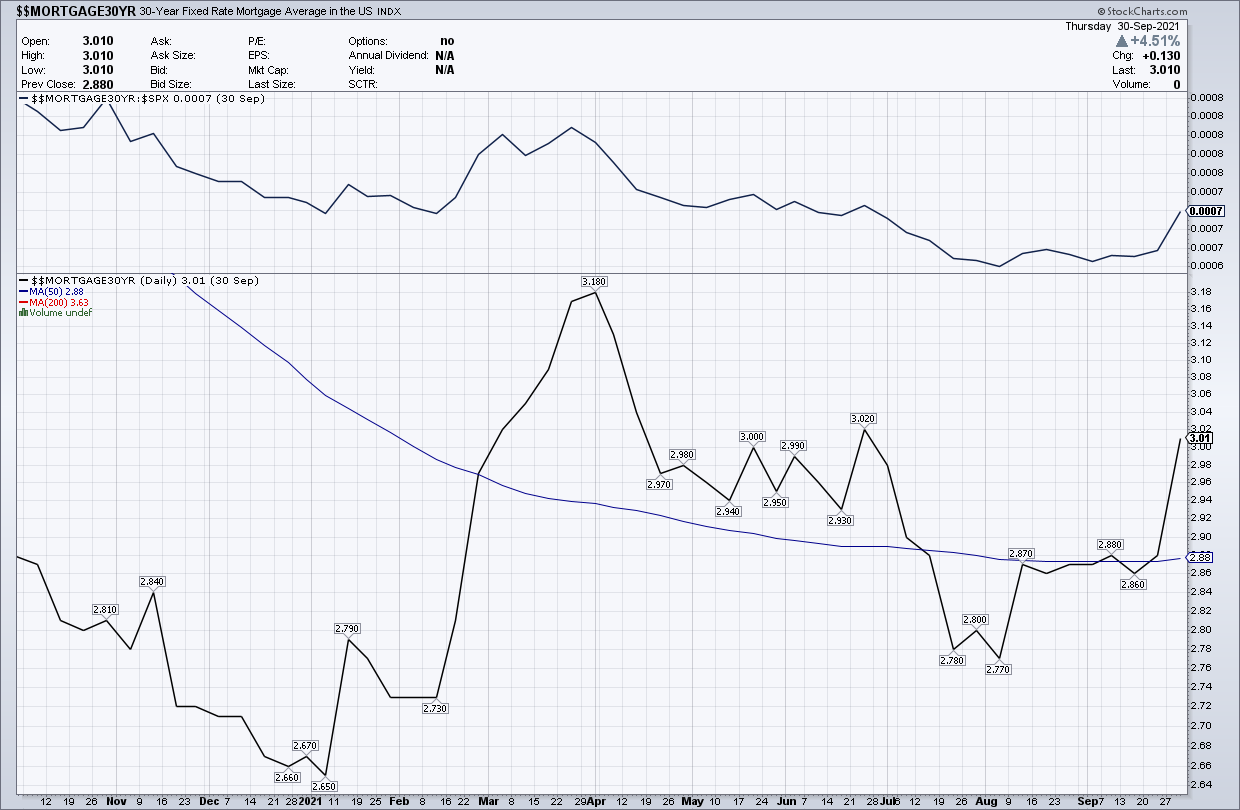

In several previous articles I have opined that an increase in mortgage rates may be our only hope for slowing the escalation of home prices that we’ve been experiencing for the past year. With mortgage rates hitting above 3% last week for the first time since June, it’s a good time to revisit this conversation and what we should expect next for mortgage rates.

Since the summer of 2020, I have argued that if mortgage rates could get over 3.75%, days on market would rise and the rate of price growth would cool. This will be bullish for housing because the price gains we have been seeing are extremely unhealthy.

A common theme in the interviews I have done in 2021 has been that this is the unhealthiest housing market since 2010 — not because we have a credit boom or a bubble forming, but because we have forced bidding on too few homes. We need the days on market to grow out of the teenager stage.

If the antidote to our housing market ills is higher mortgage rates, when can we expect getting this cure? The unfortunate answer is not anytime soon.

If you are familiar with my work, you are aware that I rely heavily on the movements of the 10-year yield to guide my mortgage rate predictions. Even though I have been extremely bullish on the U.S. economy, my bond market forecast for the 10-year yield in 2021 was that it wouldn’t go above 1.94%, with the lower end of the range being 0.62%. This translates into the upper range of mortgage rates to be 3.375%-3.625% at best, and lower end of the range to be 2.25% – 2.375%.

In my America Is Back recovery model that was published on April 7, 2020, I wrote that the goal for the 10-year yield would be to create a range between 1.33% – 1.60%. This is something that couldn’t have happened in 2020 but in 2021 should be the case.

Considering the strength of the economic recovery we have been having since April 2020, I would have been shocked and disappointed if the 10-year never got to 1.60%. Like clockwork, the 10-year yield did what I thought it should do. As much as I love Van Gogh and Monet, the chart below may be the best piece of art I’ve seen this year.

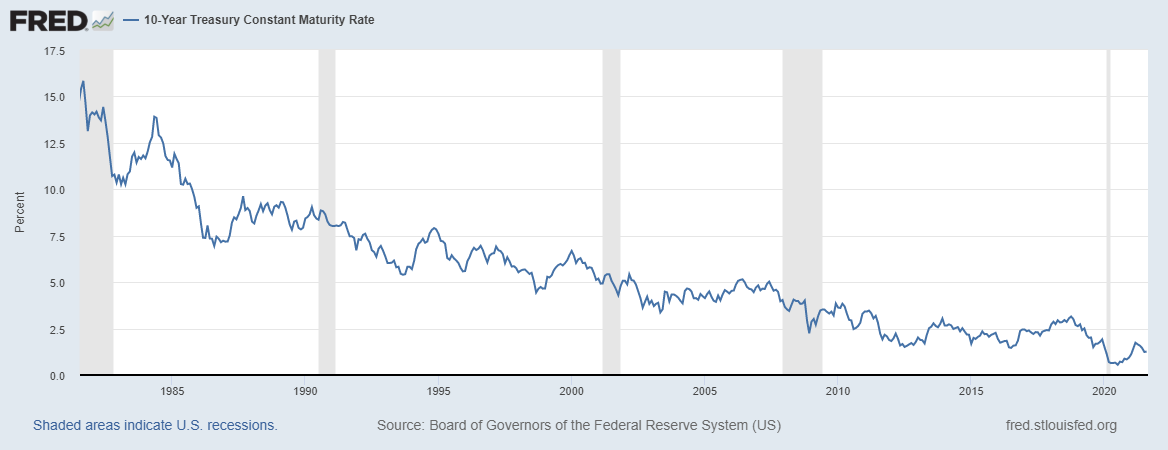

In 2021, we have had the fastest growth and hottest inflation data in recent history. This has led some to predict that mortgage rates would skyrocket. I am sympathetic to those who are shocked that the 10-year yield is at 1.48% in October, but the 10-year yield has been in a downtrend since 1981 and that needs to be respected.

Trust me, in recent years it hasn’t been easy trying to convince people that mortgage rates would have a 2 handle before a 6 handle. During November 2018, when the 10-year yield was at 3.24%, I was speaking at a conference and got scolded by another economist for talking about the 10-year yield falling in 2019 and the thought of a 1 handle on the 10-year yield. This isn’t surprising since The Wall Street Journal polled 50 economists that year and all said rates were going up. However, using the chart above, I made a prediction that we could see a 1 handle in the 10-year yield in 2019. This happened as well.

I was recently asked in a podcast interview why I always talk about 1.94% as a key level since 2019. When the inverted yield curve happened in 2019, this was something I had forecast at the end of 2017 for 2018. I truly believe we inverted the yield curve in 2018. However, after the accepted inversion happened, I talked about the 1.94% level on the 10-year yield being a key level in 2019 and even in the 2020 forecast article, I made sure to emphasize that again. (More on that topic and the entire AB economic recovery model in this podcast, where Wall Street has taken notice of my work here at HousingWire.)

Since the start of 2015, when I began incorporating bond yield forecast in my prediction articles, I have always stated that the 10-year yield should be in a range between 1.60%-3%. During COVID-19, I forecast recessionary yields of -0.21% – 0.62%. Given that the recession ended in April of 2020 and we have been in recovery mode ever since, we should see the range of 0.62% – 1.94%, which is what I forecast for the economic expansion period.

What can take bond yields higher than 1.94% and get mortgage rates to 4% and higher? And why is this important? The most important data line I want to see grow is the days on market, as it’s simply too low currently and creating too much price growth in housing.

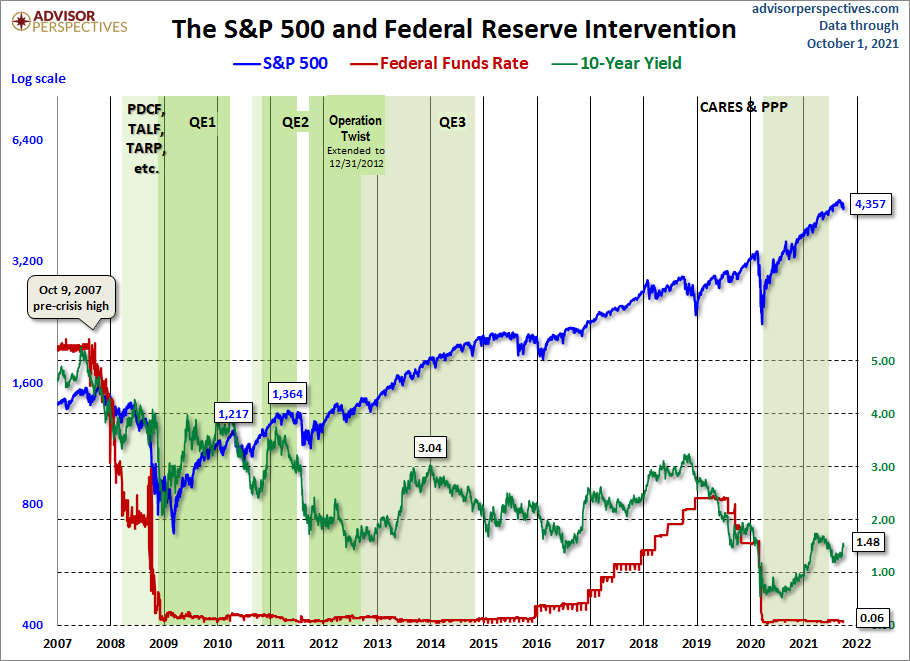

One common thing I see is that people say when QE (quantitative easing) ends, the bond market bubble will end and bond yields and mortgage rates will rise and housing will collapse. Let me just make this is as simple as possible, by referencing the chart below:

- QE1 ended, bond yields fell.

- QE2 ended, bond yields fell.

- Tapering started to go into the final stages in 2014 and bond yields fell.

- QE3 was supposed to be the end of humanity when it finished. After the end of QE3, bond yields fell.

Just be careful of putting all your eggs in the “bond market is a bubble and rates have to skyrocket when QE ends” basket. It didn’t end well for those forecasting much higher mortgage rates and bond yields, as you can see below.

While bond yields are historically low, that long-term downtrend stayed intact even with the best economic growth and hottest inflation data in years. Can the bond market have an algo model bond selling fit? Yes, it can. However, nothing of note will happen as long as we are below 1.94% on the 10-year yield. I am just sticking to my guns here, the same way as in 2019, 2020, and 2021.

In 2021, when the mention of tapering started at some point, bond yields fell.

The most realistic scenario I have come up with to break that 1.94% level is that the world economies start to come together and move past this COVID-19 historical stage. This means Japan and Germany bond yields move up as well. It’s really hard for the U.S. to break away too much from Germany and Japan’s 10-year yield.

When the world economies are running in a more normal fashion, that could serve as a reasonable premise to get the 10-year yield above 1.94%. My next-level peak would be only 2.42%. However, that bridge has not only not been crossed, but it’s not close enough to be tested. So, until that happens, no 4% plus mortgage rates here in America.

As crazy as this sounds, 2021 looks remarkably normal with regard to the bond market and mortgage rates.

I am big believer in range-yield work — it’s been a staple of mine for many years and a big factor in writing my American recovery model back on April 7, 2020. Economic models keep us in line and we always look for things that can break it with live events daily. However, for now everything looks just right to me.

While I do understand that bond yields being this low with our economic growth and inflation data seems strange, just remember: respect the trend as it is your friend. Don’t betray it and you will be fine at the end.

On Oct. 5, I will be speaking at the virtual California Association Of Realtors REImagine Conference and Expo with other economists about the state of the U.S. housing market and what to look for in 2022. I will be attending the Mortgage Bankers Association Annual conference in San Diego Oct. 17-20 and hope to see many of you there.