With mortgage rates falling during the COVID-19 crisis, many households were able to refinance to lower payments. Because a mortgage payment is almost always the most prominent payment households make each month, lower payments have allowed homeowners who bought homes to have better cash flow over the last few years. This means mortgage holders who have refinanced their homes to lower payments while their wages have also grown look great on paper.

In general, homeowner households were financially solid going into the crisis. When COVID-19 happened, some sellers were able to sit back and watch the market. We didn’t see any mass hysteria to sell. It was just a matter of weeks before the buyers returned and sellers sold their homes, leading home sales to get to pre-cycle highs in 2020 and 2021.

And then home prices took off, and total inventory levels dropped toward all-time lows. The housing market prevailed during COVID-19, and this was a positive outcome not only for the U.S. housing market but for the American economy.

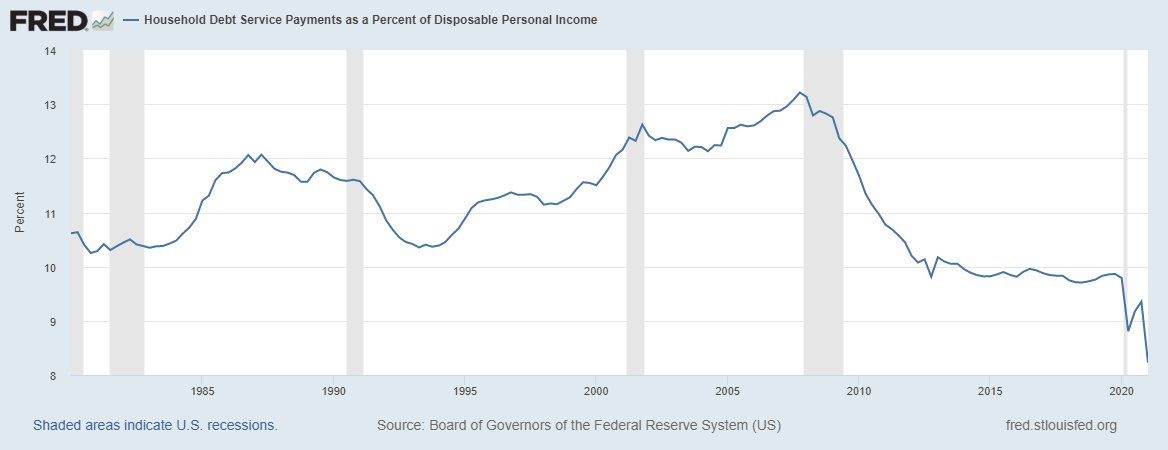

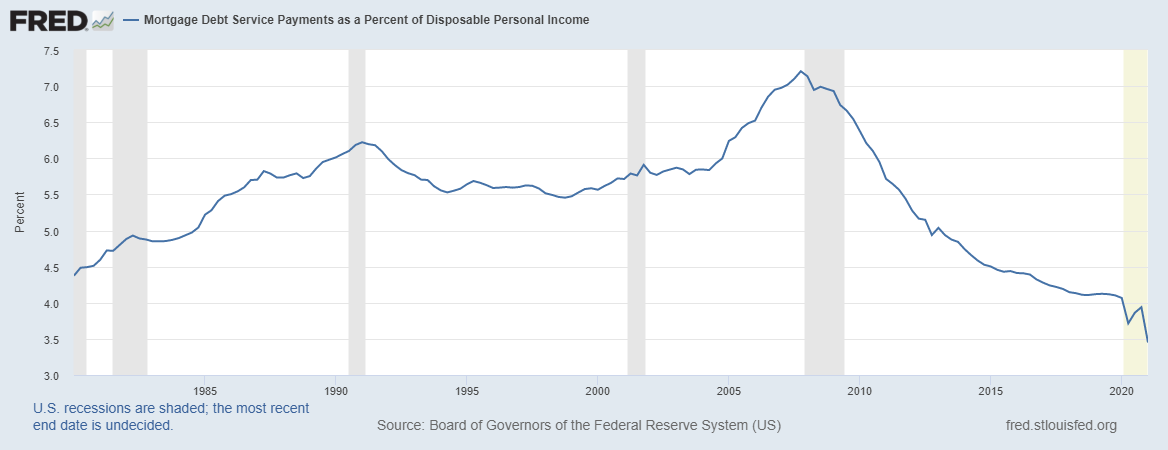

Despite the COVID-19 crisis, American household balance sheets look better in 2020 and 2021 than they have for years. On a broader scale, since most consumer debt is mortgage debt, household debt service payments as a percent of disposable personal incomes are at all-time lows.

Of course, this means mortgage debt service payments as a percent of disposable personal incomes are at all-time lows.

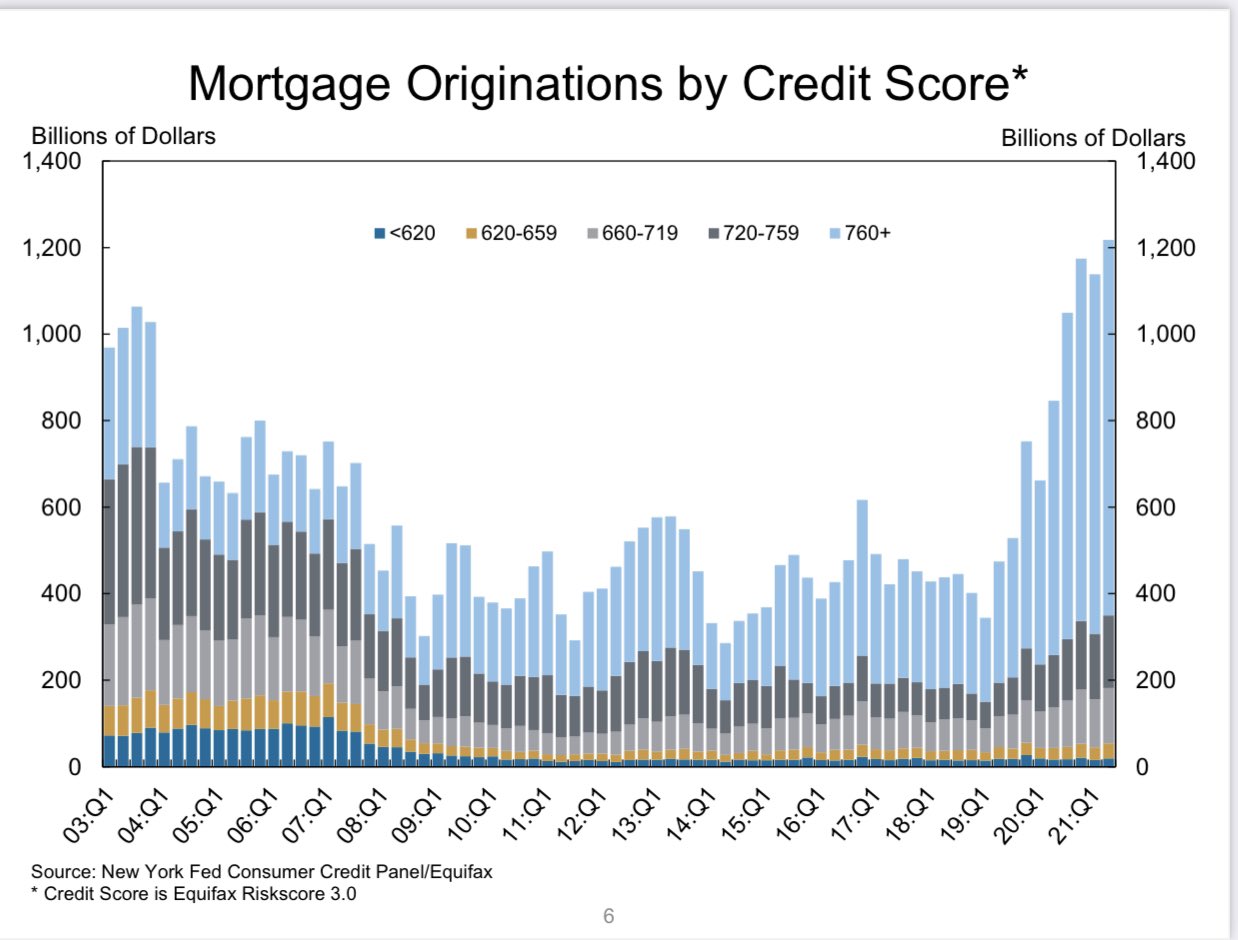

Loan origination data looks good too. Mortgage holders have strong FICO scores and assume fixed low debt cost loans that are 15 to 30 years in duration. These are not the exotic ARM products that were typical during the speculative housing bubble years. These loans are fixed, tedious, long-term debt products with no recast risk. Bland, vanilla and as safe as it gets.

This all sounds sunny for homeowners and the housing market, but when a majority of homeowners have good financials, there is one drawback that is rarely given voice and it has to do with home prices, especially now that housing tenure has doubled. From 1985-2007 housing tenure was running at five years; from 2008-2021 it’s well north of 10 years.

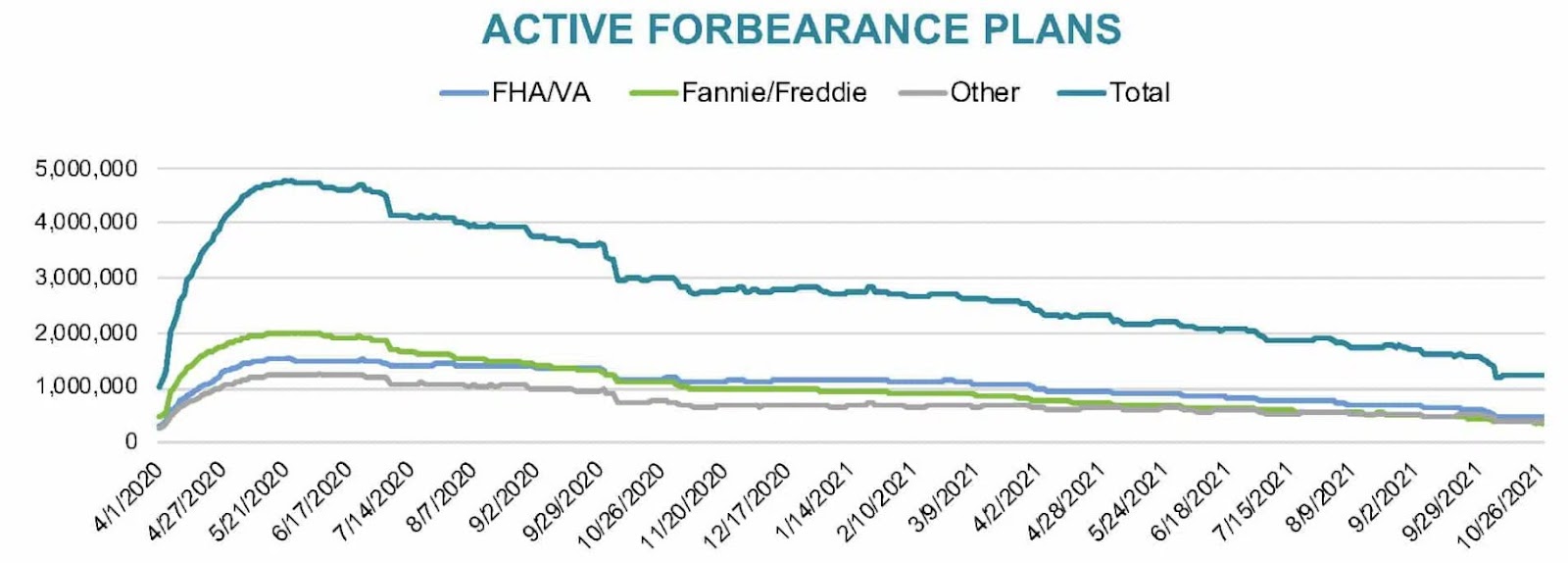

Homeowners with low-cost debt and good cash flow are not motivated to provide any significant price cuts when they sell — and this is especially true when they have to buy their next home from a likewise unmotivated seller. When there is a job loss recession, and some sellers are forced to sell their homes, that is the strongest motivation to sell at any price. However, the recession ended last year, and forbearance numbers are about to break under 1 million.

From BlackKnight:

Jobs Friday is coming up! I still believe, even with all the headwinds we have had to deal with in 2021 and 2022, that we should get all the jobs back lost to COVID-19 by September of 2022 or earlier. This means more people will get off forbearance in the upcoming months.

When this psychological variable is added to a market already taxed by low inventory and solid replacement demand, we get very sticky home prices. Mortgage rates are near 3%, and we have entered a demographic patch with the largest group of Americans of home-buying age that we have ever had. When we add this bonus of buyers to the move-up, move-down, cash buyers, and investors, we can count on nice, stable demand for the next several years.

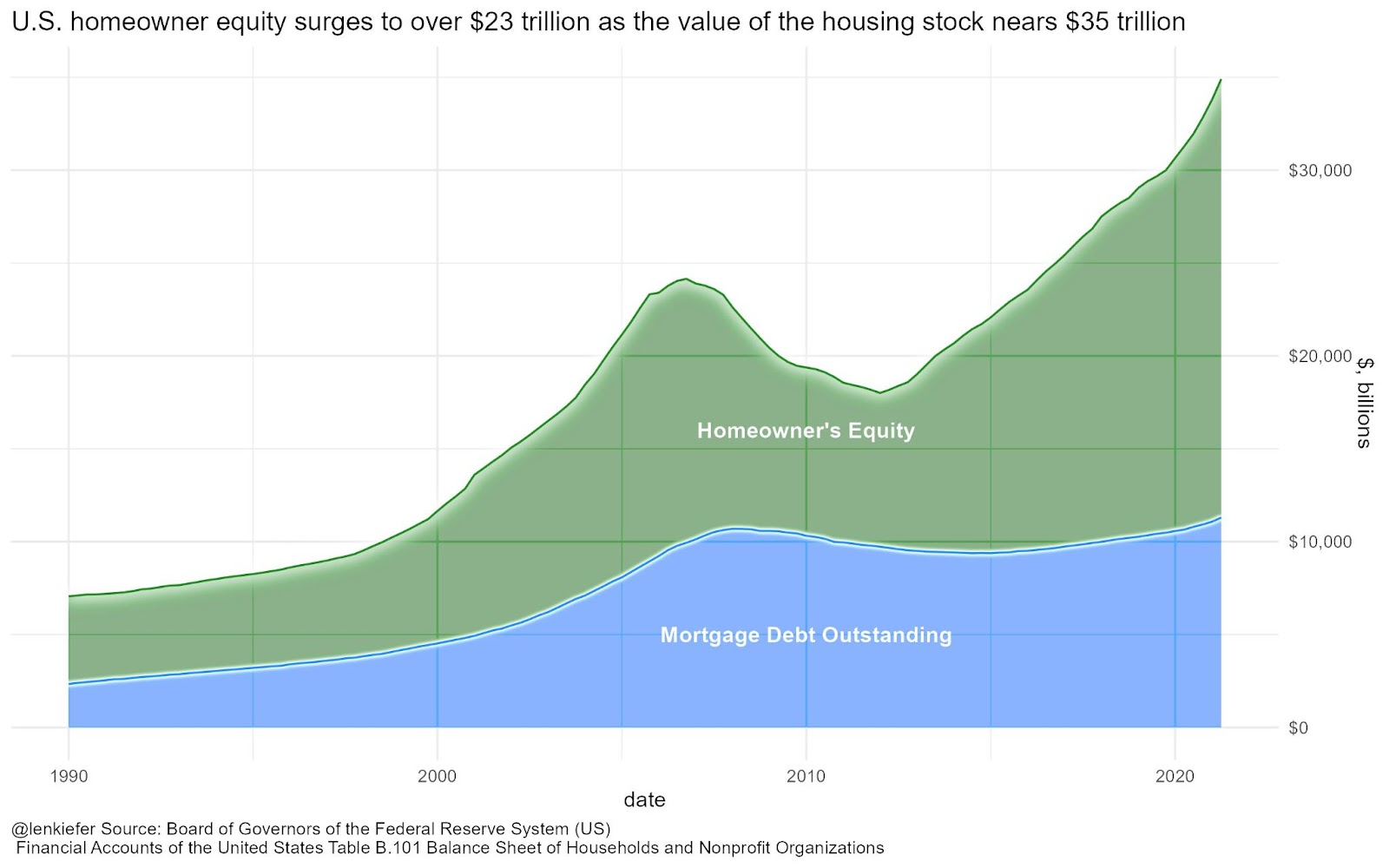

Still, housing demand has limits. We have more folks buying homes with mortgages in 2020 and 2021 than in any other period from 2008-2019, but we are not in a credit boom like we were in bubble years. On a nominal basis, we don’t see any real growth in mortgage debt from the housing bubble’s peak. However, we see a lot of growth in nested equity created post-2012. This chart from the great Len Kiefer of Freddie Mac shows the solid financial wealth of homeowners now.

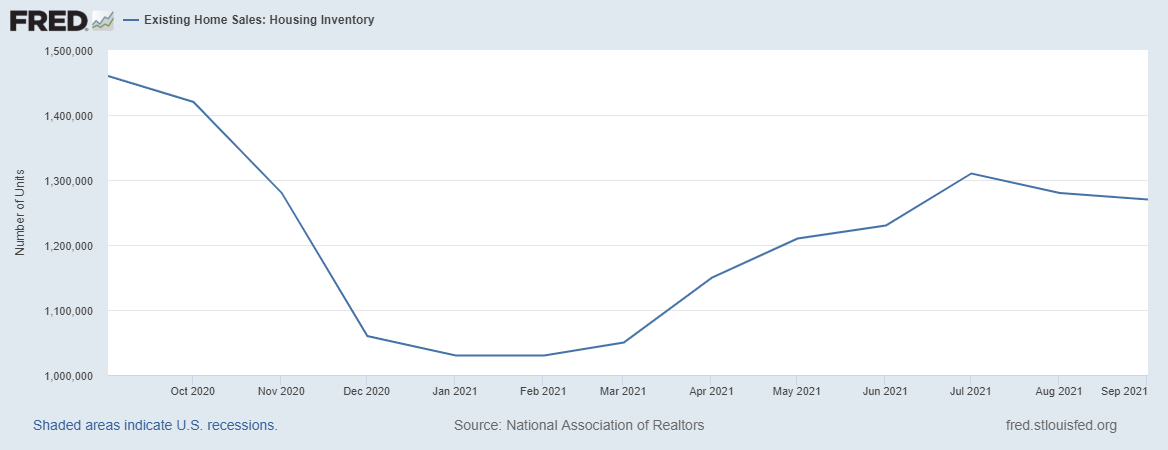

So we have the demand, but where is the supply? Bueller? Bueller? Inventory is playing hooky.

Let’s just hope the total inventory can get to just 1.52 – 1.93 million. Yes, that is historically low, but it will certainly create a much more balanced marketplace than what we are dealing with today.

Stable demand, low mortgage rates and low inventory, along with unmotivated sellers, lead to a perfect storm of price stickiness which could mean that even if mortgage rates rise, home prices may not fall as far as people believe they would. We had this situation in the previous expansion: In 2018, mortgage rates rose to 5%, but nominal home prices didn’t fall.

You may call sellers greedy or just good business people: When one isn’t desperate to sell, then there is no need to provide significant discounts. Homeowners can just wait it out until a few buyers bite.

This is the downside of having homeowner households with excellent financials. First-world problems, I know, but it’s a topic that needs a voice. These sellers have no reason ever to accept a significant drop in prices and sell the nested equity they built over the years. I bring this up because home-price growth in 2020 and 2021 has already surpassed what I anticipated would be the maximum cumulative price growth of 23% for 2020 to 2024 to be considered healthy.

We would need three years of negative incremental price declines of 3% to get back in line with my model for modest, sustained growth. We don’t want a repeat of what happened to home prices in the years 2020 and 2021. In the last two years, home prices exceeded what I estimated increases for the next five years. If we get three more years of that kind of unhealthy home-price growth, “Houston, we have a problem.” This possibility is why I say this is the unhealthiest housing market post-2010. Still, first-world problems compared to what we saw from 2005-2011.

In the summer of 2020, I wrote that higher mortgage rates of 3.75% and higher could lead to more days on the market and change the rate of home-price growth. This would require the 10-year yield to get above 1.94%, but that wasn’t part of my forecast for 2021. For 2022, I am concerned that rates will go lower, not higher, which will exacerbate our problem.

If you follow my work, you may have noticed that I separate our recent housing market history into two distinct epochs. Following the housing crash, 2008 to 2019 represent a period of the weakest housing recovery ever. During these years, I predicted that new home sales, housing starts, and mortgage debt would be soft — and they were. The year 2020 started a new epoch that would last until 2024. During this period, we should expect two things to happen.

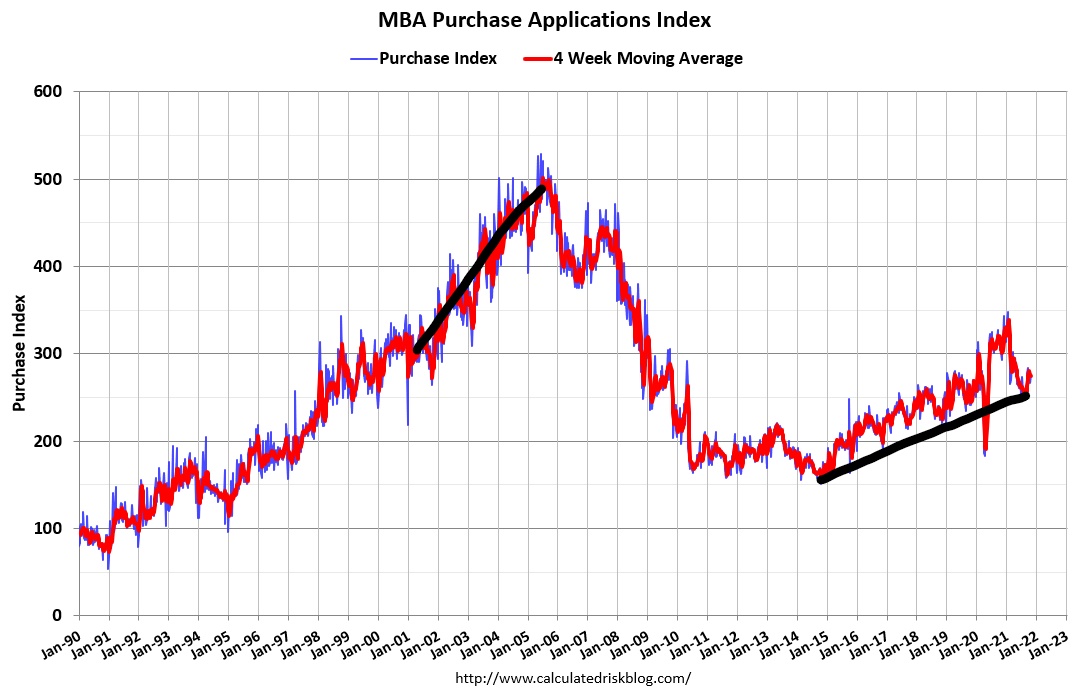

1. Mortgage demand will increase and drive purchase applications to the 300 level of the MBA’s purchase application index. This prediction was fulfilled very early in 2020 but was then curtailed by the curveball COVID-19. But slow and steady growth has won this race since 2014.

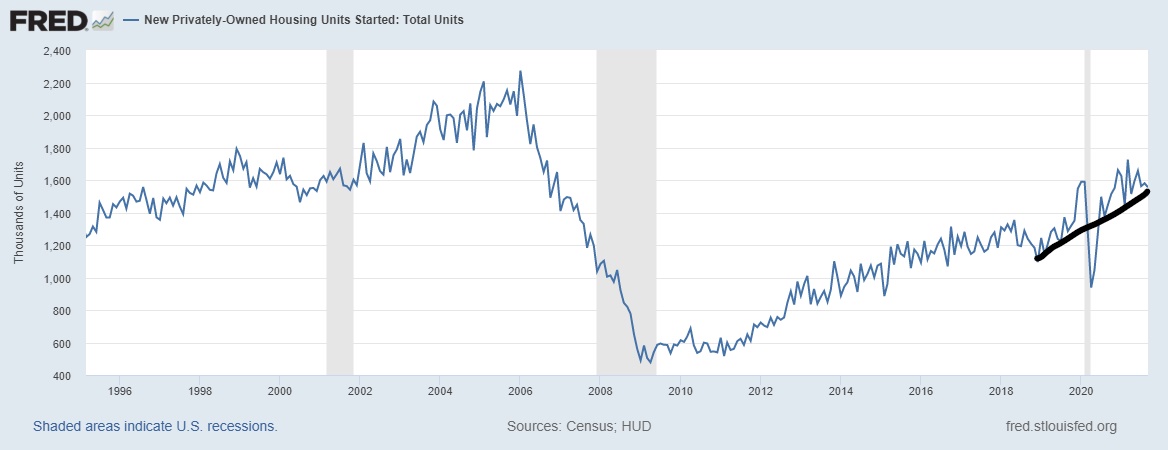

2. Housing starts would finally start a year at 1.5 million and higher. It was challenging to convince people that this was possible because most folks think we don’t build enough homes. Contrary to this, new home sales missed estimates in 2013, 2014 and 2015. In 2018, we had a supply spike in new home sales, which halted the growth rate for construction until monthly supply came back down again. Builders learned from those years and now closely control inventory, building only in response to demand. Even with all of that history, we are going to start a year above 1.5 million in 2022.

The reason I bring up these two major long-term calls is that that in the previous expansion, we had a low bar in housing. Since home sales weren’t booming we never had a discussion about an overheated demand cycle or a major overbuilding expansion such as we saw from 2002-2005. Now that these levels have been met, we no longer can say housing has a low bar — everything needs to be earned.

However, I would love to see negative 3% price growth for the next three years to get home prices somewhat stable again. I don’t believe sellers are going to be so willing to not ask for top dollar with rates under 3.75%, or total inventory levels under 1.52 million, thus making housing stuck in a tug-of-war that is long-lasting, with no winners and sellers who can set prices on their terms. As you can see, I am rooting for total inventory levels to get above 1.52 million more than anything else for the housing market. We need some B&B action: boring and balanced!

As 2021 comes to an end, the job loss recession that ended in 2020 is in our rearview mirror and the number of loans in forbearance is about to break under 1 million. This is all good news for the economy but bad news for the housing bears who keep calling for a housing crash. More importantly, it is terrible news for those looking to buy in a market where owners aren’t motivated to negotiate aggressively and home prices keep rising. Will prices be so sticky that even when demand softens, prices remain high or, worse, continue to increase?

Sometimes, it isn’t a scary housing bubble boy crash that you should be worried about. Sometimes just being stuck in the ocean, not underwater but not going anywhere, can be frustratingly unhealthy.