The No. 1 reason a mortgage loan applicant is denied for a loan is a problem with their credit score.

In good times when qualified mortgage borrowers are plentiful, most originators don’t give a suboptimal credit score a second glance. But when every loan matters, like the market we find themselves in today, it makes a lot of sense to take a closer look at the borrower’s credit score.

In our work over the past 20 years, virtually all of which has been aimed at making housing more accessible and affordable to more people, we have found that the borrower’s credit score is the only aspect of the deal that can change within the timeframe it takes to originate the loan.

But that’s only true if the problem is approached correctly.

Taking a harder look at consumer credit

A glance at the headlines will tell you that more industry leaders are beginning to take the borrower’s credit seriously. It’s why regulators are spending so much time considering changes and why more originators are stepping up to help their loan applicants increase their scores.

When it comes to loan underwriting, the simplest equation involves ensuring the borrower exceeds a minimum capacity to repay the loan, the collateral is worth more than the loan amount by some minimum amount and the consumer’s credit score exceeds a certain threshold. Of these three Cs, capacity, collateral and credit, only the last can be changed in the short term.

But that won’t happen if the originator sends the applicant to credit counseling. This is for consumers who don’t understand credit and it can take months or years for them to get their financial life in shape.

It also won’t happen if the originator sends the applicant to a credit repair company. They fix mistakes on a credit file, which can also take months to complete and cost thousands in fees.

Credit optimization leverages sophisticated predictive analytics to consider the elements that, taken together, result in the consumer’s credit history. This includes payment history, credit usage, credit account age, total number of accounts, hard inquiries and derogatory marks, such as late payments, collections, bankruptcies, civil judgments, foreclosures and liens.

Some of these elements will be very difficult, if not impossible, to change in the short term. But others can be changed easily and can have a surprisingly significant impact on the applicant’s credit score.

The art and science of credit score optimization

The question, of course, is what changes should be made to have the most beneficial impact on the applicant’s score while the loan is still in process. The change must have a significant enough impact to provide a return even if the lender pays for a rapid rescore.

Well, it turns out that there are two approaches to this, one that is very risky but is sometimes used by some originators and another that works well and provides a high degree of confidence in the results.

The risky approach is to guess what changes will lead to a better score. There are far more ways to reduce the applicant’s score than raise it. Don’t guess. Period.

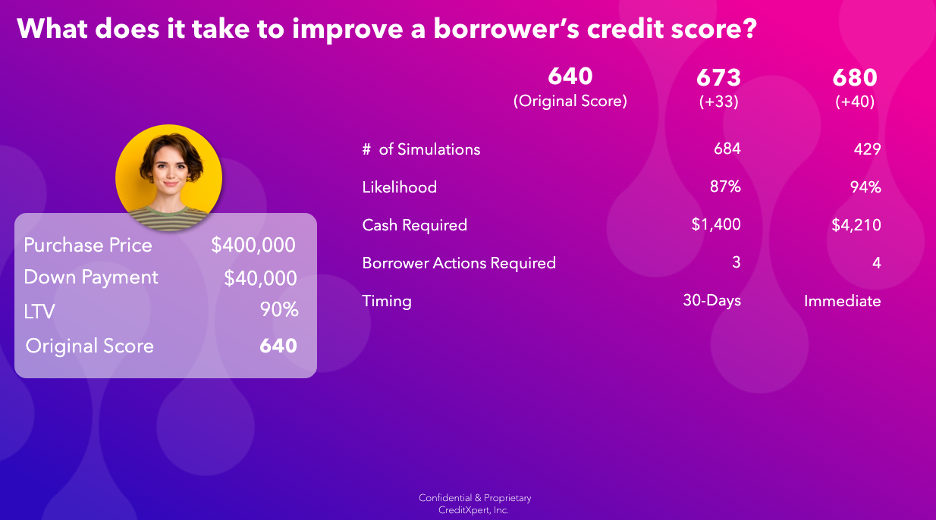

The approach we take at CreditXpert is to allow our predictive analytics engine to run hundreds, and sometimes thousands, of simulations to model and predict the impact of very specific changes on the borrower’s score.

By strategically paying down credit card debt and either opening or closing an account, an applicant’s credit score can increase by as much as two 20-point credit bands in about 30 days. And with credit card interest rates currently hovering at 24.46%, strategically paying down credit card debt is a sound financial strategy that will allow borrowers to “win twice.”

They will win by reducing interest payments on revolving debt and they will win by accessing better loan programs or securing a lower mortgage interest rate. And we know from the millions of credit scores we analyze each year that the chances that any individual mortgage applicant could raise their score by at least one 20-point bucket is just over 70%. That means that credit optimization can benefit nearly every mortgage applicant.

But historically, the vast majority of mortgage loan applicants have had no real understanding of this process or its impact on their ability to qualify for a better deal on their next home loan. When it comes to originators, tens of thousands have access to CreditXpert’s predictive analytics tools which have allowed them to optimize the scores of those borrowers in need.

But as borrowers learn of the power of credit optimization and originators continue to work through this downturn, we are seeing increasingly broader application of CreditXpert’s predictive tools.

If you would like to find out more about how you can employ credit optimization to grow your business, even in today’s challenging mortgage market, reach out to CreditXpert today.