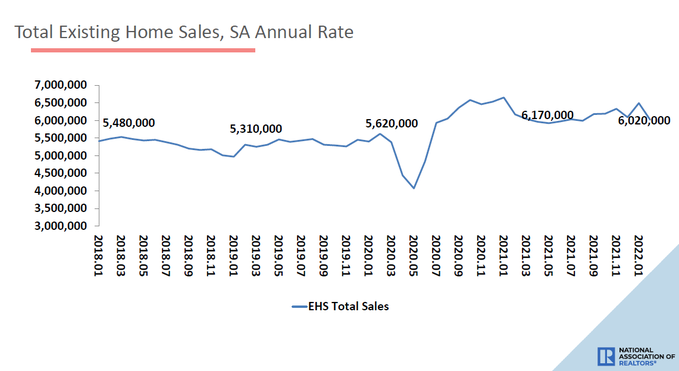

The National Association of Realtors reported that existing home sales for February came in as a miss of estimates at 6.02 million. This level is still within my 2022 forecast sales range between 5.74 million and 6.16 million. Last year I discussed sales levels coming back down to 5.84 million and I am looking for more of the same in 2022, at the 5.74 million level.

The month-to-month fall of existing home sales was noticeable, but I didn’t buy the January print of 6.5 million because I thought we had some spillover demand from December, so this month’s sales look right.

NAR Research: Total existing-home sales sank 7.2% from January to a seasonally adjusted annual rate of 6.02 million in February.

While demand is solid, the savagely unhealthy aspect of housing is continuing. Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. You can see why I have been on team higher mortgage rates for some time now because we don’t have any other way to get off this madness.

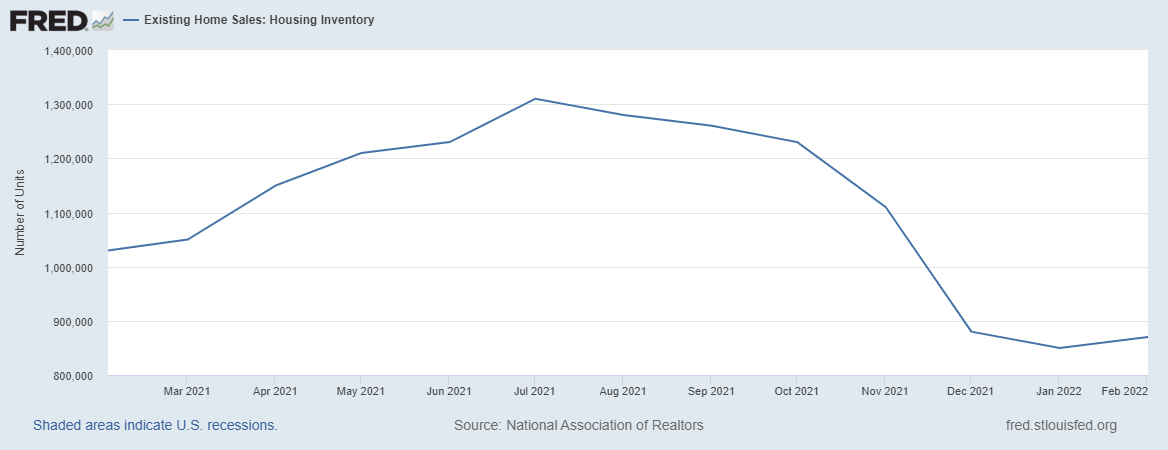

NAR Research: Unsold inventory sits at a 1.7-month supply at the current sales pace, up from the record-low supply in January of 1.6 months and down from 2.0 months in February 2021.

Now inventory is about to have its seasonal push, but the key is that we want to see inventory increase year over year, not have declines year over year. At this point, I will be grateful for being just flat. However, negative year-over-year inventory is not what we want to see.

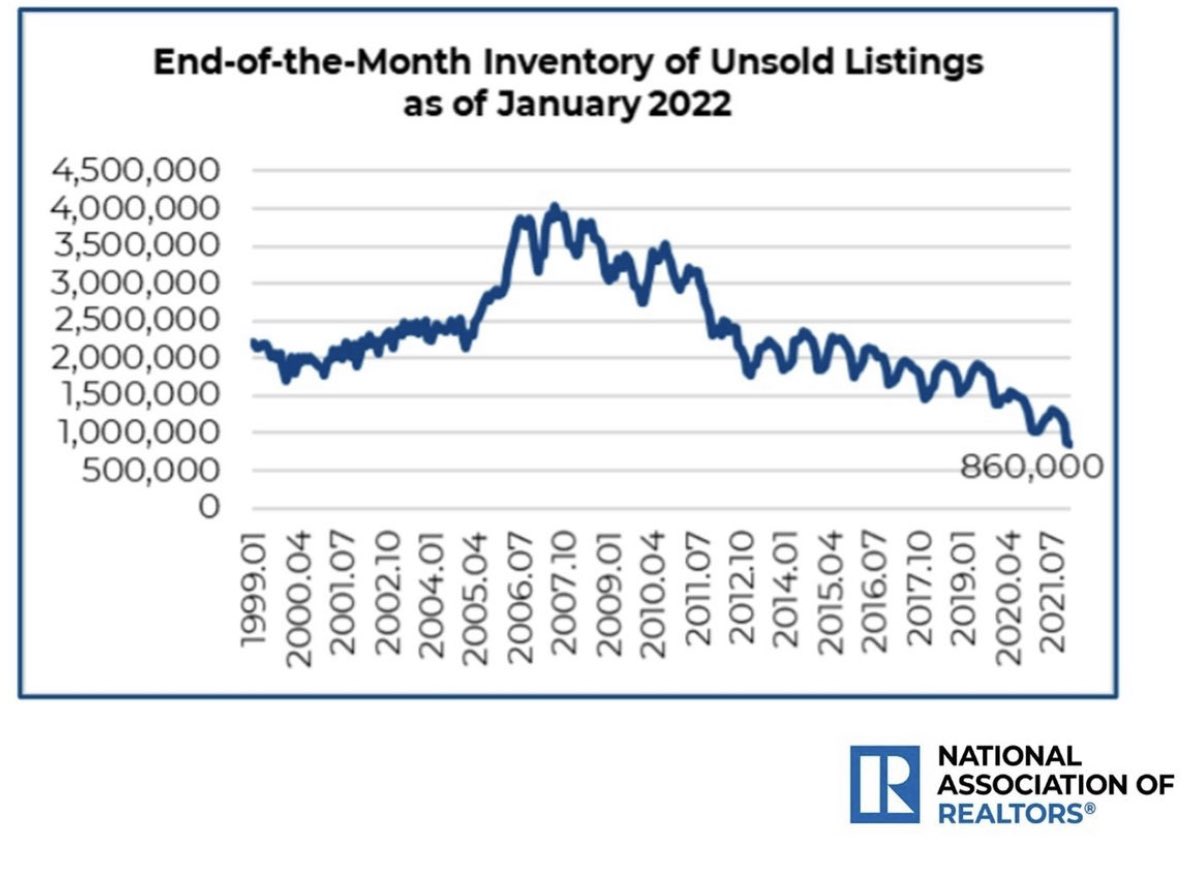

Total inventory data is deficient, and this was my biggest fear in the years 2020-2024, and it happened. Inventory has been slowly falling since 2014, so if demand picks up in 2020-2024, it can collapse to shallow levels. Currently, the total Inventory from the NAR is 870,000.

To get the housing market to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million; this is still historically low, but this gives the housing market a breather from the madness that we see today.

Since the end of 2020, I have tried my best to stress that home prices overheating should always be the concern in 2020-2024. You can’t have the best housing demographics ever, with the lowest mortgage rates and the best loan profiles with falling inventory for eight years, and not be concerned about this during 2020-2024.

I thought creating the term forbearance crash bros in the Summer of 2020 would help educate homebuyers. However, we still live in a society where the premise that housing will crash 40%-80% is looked at as a logical view. After 11 years of listening to people talk about housing crashing from 2012-2022, you have to ask yourself who is the bigger fool: the fool, or the fool who follows them? A significantly older man named Ben said that.

Home prices are still overheating even today because we currently have a raw shortage of homes. This is not a good thing and is why I am on team higher rates.

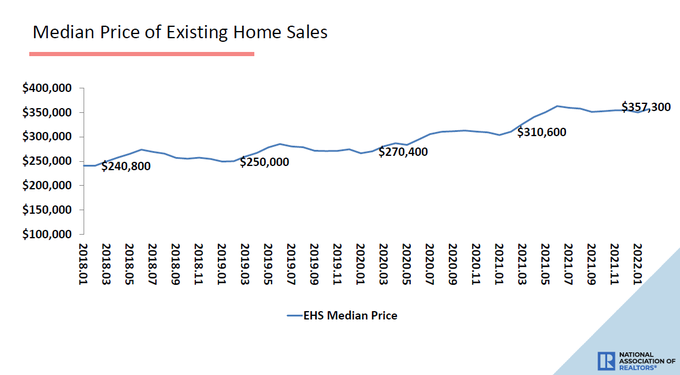

NAR Research: The median existing-home sales price rose to $357,300, up 15.0% from one year ago.

One of the critical data lines that I want to see improve this year is days on market. My concern now is that some sellers are feeling stressed about this market, which should never happen because this is the best seller market ever. However, a seller is also a natural homebuyer, unless they’re an investor. People who sell need to live somewhere.

With such meager inventory, inflation has risen so much., even for rental housing. You can see why some sellers are stressed now. Nobody wants to sell their home at a mortgage rate of 3.25% or lower if they can’t find a home they like, then be forced to rent at a higher cost. Americans are starting to realize now that being a homeowner was the best hedge against this burst of inflation.

So what I would love to see is that days on market grow to create a pause in this housing market, so some sellers don’t feel stressed about selling and kill off this super-hot price growth. Sadly enough, that hasn’t happened yet.

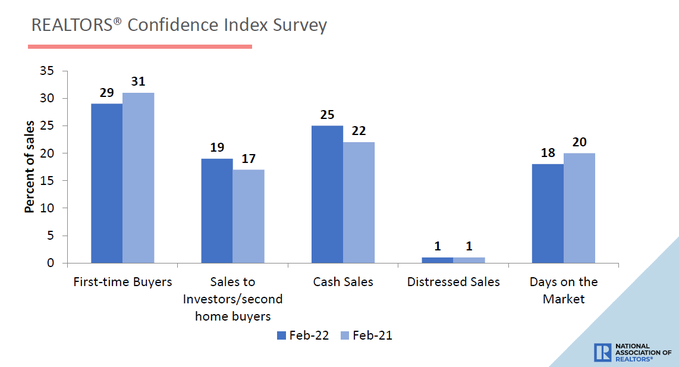

NAR Research: First-time buyers were responsible for 29% of sales in February; Individual investors purchased 19% of homes; All-cash sales accounted for 25% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 18 days.

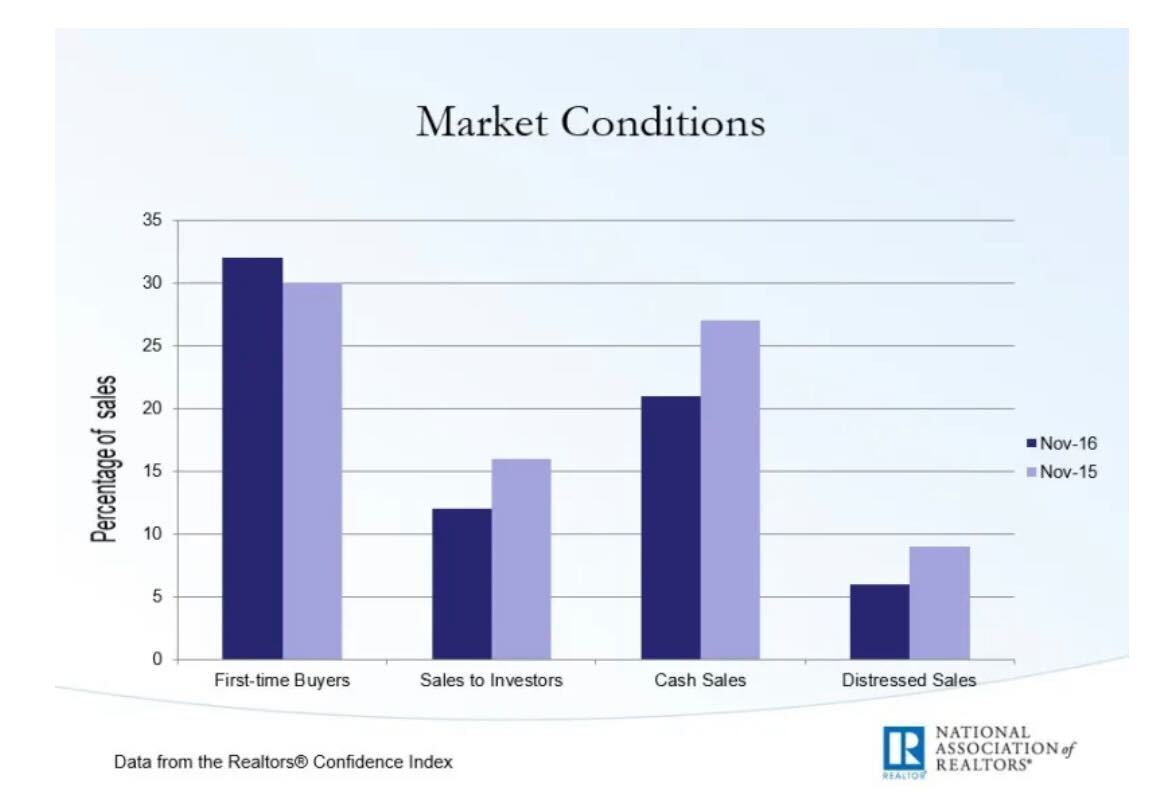

To show some historical perspective on the NAR breakdown of the different types of homebuyers, the chart below shows market conditions back in 2016. As you can see from this NAR report, cash buyers as a percent of sales is slightly lower now than levels in 2016. However, distressed sales are down a lot today compared to back then, and sales to investors are 19% today compared to 16% back then.

From NAR in 2016: First-time buyers were 32% in November; Investors were 12%; All-cash sales were 21%; Distressed sales were 6%.

The current existing home sales report continues the trend of an unhealthy housing market but it is now becoming a savagely unhealthy one. I need people to understand that shelter cost differs from the prime focus on rising and falling home prices. Housing is the cost of shelter to own the debt; it’s not an investment. This is the most prominent housing demographic patch ever recorded in history.

This housing market isn’t driven by FOMO (Fear Of Missing Out) or people trying to make a quick buck. That was the housing market of 2002-2005, not what we have today. You can easily see below that we don’t have the credit boom as we did during the housing bubble years. We have solid replacement buyers: people needing shelter.

The problem we have now is that we have a raw shortage of inventory for the number of Americans that need homes. Demographics are solid, the unemployment rate is under 4%, and even with the rise in mortgage rates, they’re still under 4.5% today. As you can see, we have had a lot of capacity for home-price growth with current homebuyers. However, I have lost my five-year home-price growth model of 23% in just two years, and inventory has worsened in 2022. So now, I consider this not just an unhealthy housing market, but a savagely unhealthy housing market.

I have been writing about the Denver RE market for 15 years now and the last time we had 1.70 MOI was 2013 as we have been at 1.50 months or less since 2014 and since June 2020 we have been at 1 month or less for 21 consecutive months. With national MOI now at 1.70 months you are correct that homeowners who want to sell are feeling stress about this market. Here in Denver we have called it FEAR for years and it has continually gotten worse. It’s a Death Spiral honestly. And higher mortgage rates I am afraid will only make this problem worse. Why? Yes, demand will soften but supply will drop much more as who wants to sell a home with a rate of 2.75% when mortgage rates are now nearly at 5%? The Fed’s talk about reducing their balance sheet is only going to make the housing supply crisis worse and cause home prices to rise further. As a Stats Geek I have NO idea how the Denver RE market will get out of our Death Spiral of shrinking inventory except for terrorism or WWIII. We need something to SHOCK the market that will cause the unemployment rate to hit 10% for an extended period of time. I hate to say this but there is no natural organic way out of this death spiral I am afraid here in Denver.