If demographics are economics, and we accept that in the years 2020 to 2024 the U.S. will have the best housing demographics in history, then it follows that home prices could take off in an unhealthy way. In 2021, we already have the unhealthiest housing market — in terms of low housing market supply and multiple bids for each sale — that we have had in the last 10 years.

Adding to the built-in demand from excellent housing demographics, our recent history also contributes to the hot market. One of the COVID-19 pandemic’s economic realities is that U.S. bond yields and mortgage rates have been sent lower than what would have occurred in an expansion or a traditional recession.

Additionally, the COVID-19 pandemic disrupted the natural housing market supply, keeping inventory lower than it usually would be. Low inventory, low mortgage rates, and built-in demand — what do you think would happen with home prices given this perfect storm?

The only proven pressure release valve we have at our disposal to calm this price-growth storm is higher mortgage rates. Only higher mortgage rates have the recent historical precedent for cooling the market and creating more days on the market, thus boosting inventory.

Let me give you two examples of what I am trying to say here.

Here is our historical precedent. In 2013, housing pundits said that there was “record-breaking demand, but we have no homes to buy, which is holding down sales.” When mortgage rates went up that year, the rate of growth of home prices fell. Home prices did not go negative, year over year, but the rate of growth fell noticeably. Demand got softer. In 2014, mortgage purchase applications were down 20% year over year and remained so for some time. The builders missed sales estimates.

Secondly, in 2017, existing home sales did slightly better than I predicted. Again the housing pundit’s narrative was that sales would have been better if inventory was better. In 2018, I forecasted negative sales growth and increased inventory year over year, but warned that we shouldn’t overreact to this. That year mortgage rates rose, and we had over 12 months of negative demand compared to the previous year.

After mortgage rates went lower in 2019, the market found a solid base to end 2019 roughly flat year over year for the existing home sales market. The higher inventory for the new home sales sector meant the builders had housing supply shocks, resulting in a halt to new developments. The builders’ reaction to the increase in housing market supply made everyone very nervous about housing. However, once again, lower rates created that inventory to drop back then, and things went back to normal.

From this history lesson, the intended “take-away” is that the housing market can go very quickly from what everyone is calling record-breaking demand to fears about a crash due to no demand. It doesn’t necessarily make sense, but it is just the nature of the beast.

But higher mortgage rates have instilled balance in the market in the past. The COVID-19 pandemic removed that balancing force by causing mortgage rates to go lower and stay lower for longer. But all this can be cured by time. Higher rates will cool down prices, reduce multiple bidding scenarios and cause homes to be on the market for more extended days.

Also, whatever dislocation in the natural housing market supply that has been held back due to COVID-19 should work itself out in time. This would be how natural market forces would work to rebalance the market.

But some folks do have some other creative ideas to increase inventory. Ralph McLaughlin from Haus recently wrote an article for HousingWire proposing incentives that would move the market, such as reducing capital gains to real estate investors who sell to a first-time homebuyer.

“The federal government could quickly incentivize owners of existing homes to sell using one or a combination of carrot-based or stick-based approaches,” McLaughlin writes. “Using a carrot-based approach, opening a temporary window of capital gains exemptions would incentivize owners of investment homes with capital gains, as well as owner-occupiers with over $250k-$500k in gains, to sell.”

I can think of a few reasons why this idea won’t get any traction with the Democratic party. The first is whether there is an appetite to give a tax break to someone to push out a renter to sell to a first-time homebuyer. The optics on that are no bueno. The COVID-19 pandemic resulted in many renter-friendly policies that allowed renters to stay in their homes. Giving them the boot and giving landlords financial incentives to do so? I wouldn’t want to be a representative facing midterms with that vote on my roster.

Another creative proposal to shake up the system is to make it more expensive and less profitable to be a single-family home landlord. As McLaughlin writes: “Alternatively, a stick-based approach might raise taxes on single-family rental income, implement nation-wide rent control, and reduce bulk ownership of single-family homes.”

The likely unintended consequences of this would be families that could not afford to buy into neighborhoods would be displaced in favor of homebuyers or families doing well. Also, the Republican party would not be in favor of this. Politics — or Poly Ticks — can take creative ideas and toss them aside.

In any case, I appreciate the effort to throw around ideas; we need to have more discussions like this. The fact is that the economic ecosystem is much like a biological ecosystem. It’s hard to inject new things without impacting others.

In an article last year on what could be done to increase housing market supply and control housing cost increases, I suggested a multi-decade approach of government-sponsored construction when the housing market is softer, and the builders don’t see any profit in building more homes. I finished the article with this sober note:

“Until housing advocates, builders, homeowners, and the government all agree on a cohesive philosophy regarding housing in America, prepare to remain confused and conflicted.”

The Biden first-time homebuyer tax credit is another proposal floating around out there, gathering supporters. And let’s face it, there is no way the real estate industry will say no to a tax credit. But won’t that just throw more gasoline on this fire? The tax credit won’t increase inventory or make homes more affordable. Arguably, it will do just the opposite. My recommendation is to save this for when we have a more balanced marketplace and need more robust demand.

One idea I do support is to put a countdown clock on forbearance plans. These plans shouldn’t be a “get out of mortgage payments forever” plan. If the government wants to wait until the employment picture is back to pre-COVID levels, that’s fine with me. We have made good progress in many jobs that supply the incomes of homeowners. I genuinely believe that we should get all the jobs back by September 2022 or earlier. More on that here.

Forbearance served its purpose and was the right thing to do, but we need an end date. There was no qualification needed to participate. Since we didn’t find out if participating homeowners were economically stressed, we have no way of knowing how many of those mortgages may be in trouble if we stop the program. We need this data to make informed decisions about the next steps. Forbearance has been a very successful strategy to keep people in their homes during the crisis. However, the crisis won’t last forever, and neither should forbearance.

Another possible way to increase inventory is to fast-track vacant homes in foreclosure. These homes are detrimental to health and safety and putting these homes into the market won’t displace families. But, is there any way to facilitate those homes on the market?

The truth is we don’t have any quick fixes to cure our unhealthy housing market. Demand is solid but not booming. What happens if it does boom?

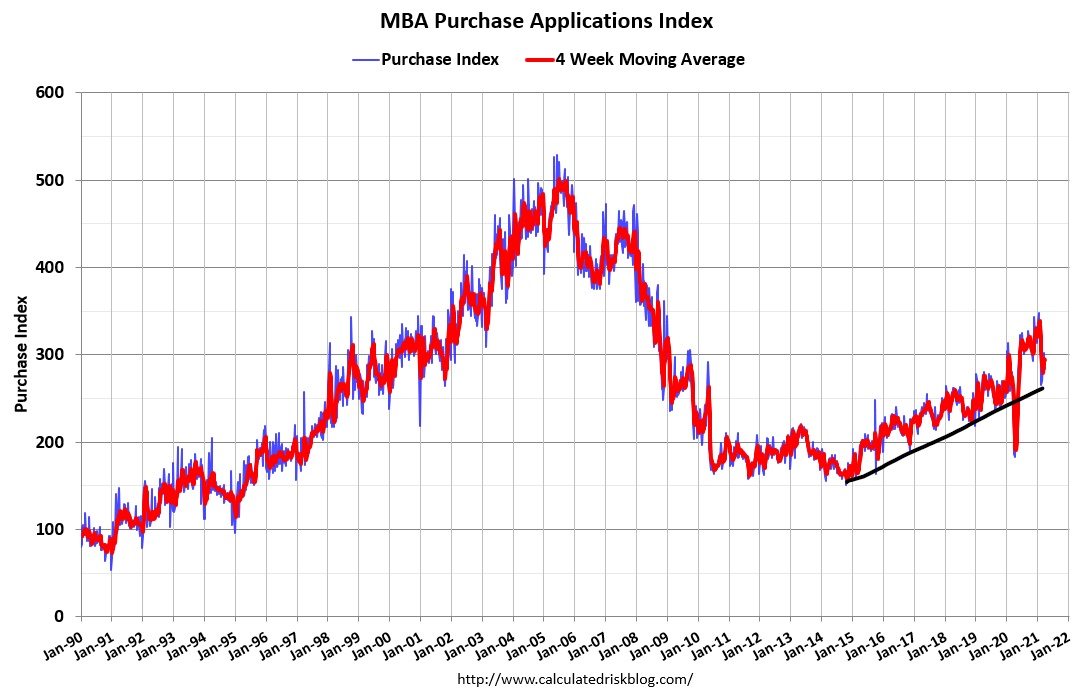

Purchase application data has been positive year over year, on-trend for where it would have been if the pandemic never happened. If you believe that the data for the start of 2021 included in those numbers some makeup demand for sales stalled due to COVID, then the double-digit year-over-year prints are justified and not outside of the trend.

The last three weeks show growth in purchase applications of 51%, 39%, and 26%, but we can discount these high numbers because these are compared to the COVID lows of a frozen market in 2020. If we adjust these numbers to account for the COVID lows, then we have only modest growth in purchase applications in the last several weeks.

If mortgage rates do go up, we can expect to lose some of the marginal homebuyers and cause houses to stay more days on the market. We could also expect some adverse purchase application reports. This wouldn’t mean that housing is about to collapse. Repeat that to yourself if necessary.

It will mean that days on the market could grow, and we may see some balance in the market between buyers and sellers — much like we saw in 2013-2014, but in this case, working with higher demand.

As I said before, demand is solid, but it isn’t booming.

In 2014, mortgage purchase applications hit an all-time low adjusting to population, but real home prices never went negative — just the growth rate cooled. In 2018-2019, higher mortgage rates of 4.75% to 5% cooled home price growth. Real home prices went negative, briefly, but we still ended the year with nearly 6 million total home sales.

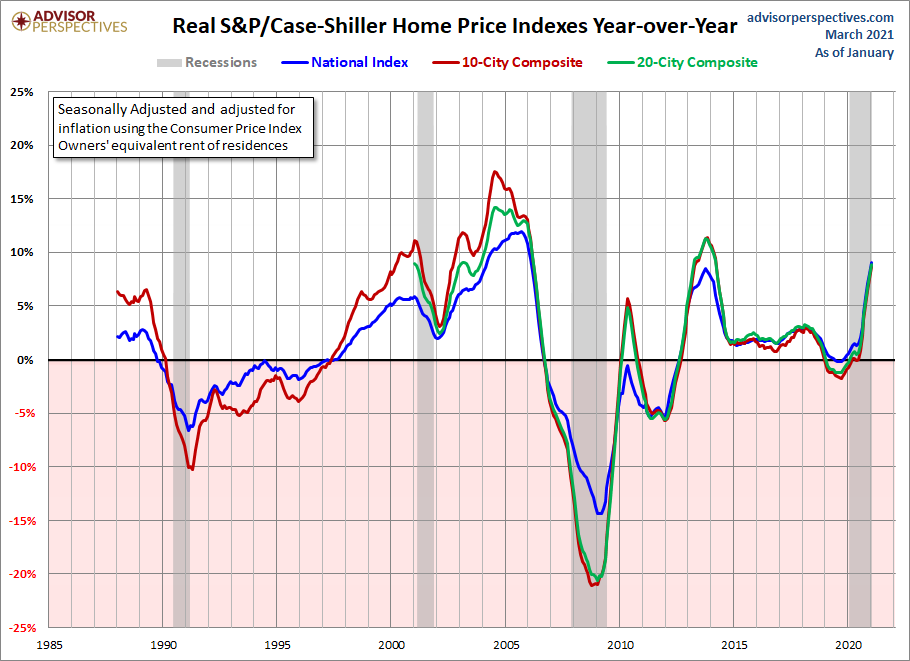

As you can see below, real home prices have taken off again. I do believe the balancing force of higher rates will cool this down. Rates above 3.75% and higher should have some impact like they have had in the past. This is a good thing, not a bad thing. Balance might be boring, but I believe it can be economically sexy. Right now we don’t have that balance — we have the unhealthiest housing market in many years.

Also, don’t forget what I said about the builders and housing construction. If mortgage rates rise high enough, the builders will have some problems selling their product, especially with lumber prices this high. They will pull back from housing construction if this occurs, which impacts housing market supply, as they have in the past.

As a country, we have to make up our minds about what we want from home. I believe as a country we love home prices rising, and this won’t change. We scream about housing affordability, but when rates rise and cool the market, we then worry about prices falling, and we talk about ways to keep values from falling.

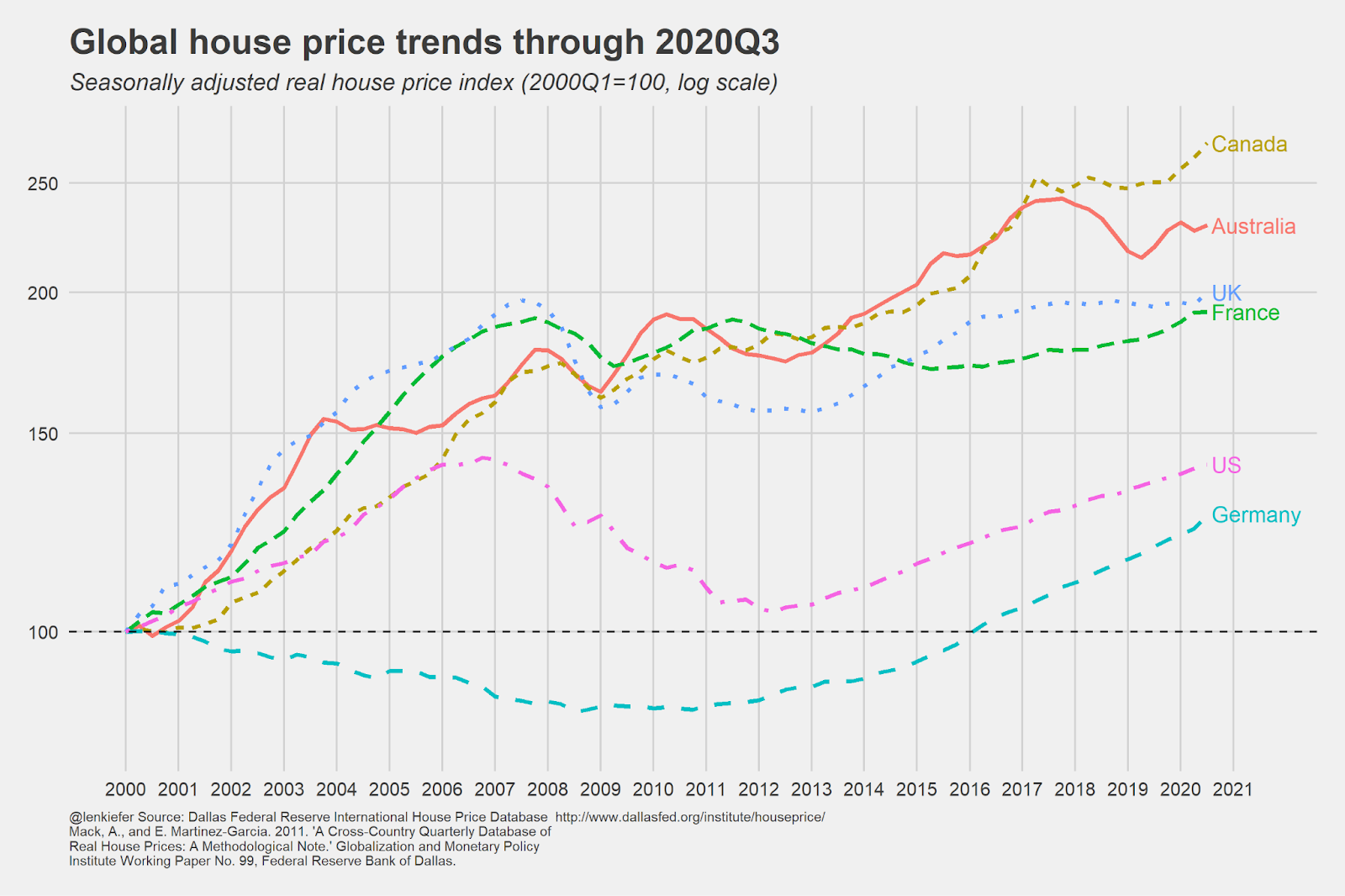

Remember, other countries have shown us that home prices can go up and up in a low-rate environment. Is this what we want for the U.S.? My gut says we’re all talk and that when push comes to shove, we love home prices rising and hate it when they fall.