Like most of the news surrounding the COVID-19 global pandemic, reports about the U.S. housing market have been discouraging. Year-over-year listings of homes for sale have plummeted – in the worst-hit markets like New York City, listings are down 80% compared to April 2019.

Guest Author

Home sales began to slow down dramatically in the last half of March, and are expected to drop even more drastically in April and May, which are usually two of the months with the highest volume of home sales. Pending home sales are off over 30%. And over 3 million homeowners have applied for mortgage payment forbearance, causing at least some concern about a large number of potential defaults at the end of the forbearance period. None of this should be surprising, under the circumstances. With almost every state in the country implementing some form of shelter-in-place order and shutting down most non-essential businesses, more than 25 million citizens filed for first-time unemployment benefits over the past four weeks.

With the majority of businesses closed or running below capacity, the consumer spending that accounts for 70% of the U.S. economy has contracted suddenly and severely, and economic projections for Q2 U.S. GDP are universally ugly.

Beyond the weakness in the underlying economy, the homebuying process is also under siege. Many states have ordered Realtors not to conduct open houses or in-person property tours. Consumers are understandably uncomfortable about visiting a stranger’s home, or conversely to list a property and invite strangers in. And the aspects of closings that have historically required face-to-face meetings are much more difficult to handle in today’s environment.

Given all of this, anything other than bad news in the housing market would be a huge surprise. The question isn’t whether housing numbers will continue to suffer until the pandemic recedes and the economy has a chance to begin its recovery. It’s what happens after that.

A look back at prior pandemics

The COVID-19 pandemic and our government’s dramatic actions to minimize its spread are unprecedented, but the housing market has proven itself to be very resilient through prior pandemics and economic shocks like the terrorist attacks on Sept. 11.

Using data from First American DataTree, I recently published a report called “Pandemics and the U.S. Housing Market: A Look Back and the Road Ahead with COVID-19,” which looked at how the housing market fared during the last two pandemic periods (SARS and the Swine Flu) and the terrorist attacks on Sept. 11. While none of these events is an exact proxy for the COVID-19 pandemic, they may provide some interesting directional attributes.

For example, the SARS (Severe Acute Respiratory Syndrome) pandemic ran from February through July of 2003. Unlike COVID-19, SARS was not widespread in the United States, but it did disrupt global economies, particularly across Asia. SARS had virtually no effect on U.S. home sales, which actually rose on a year-over-year basis during the pandemic and through the end of 2004. Home prices rose from $172,000 to over $205,000 from January 2003 through December of 2004.

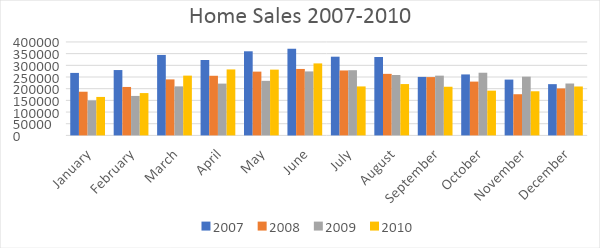

The Swine Flu (H1N1) had a much more dramatic impact on the United States, infecting over 61 million Americans, resulting in 273,000 hospitalizations and nearly 12,500 deaths during its pandemic period, which ran from June 2009 thru June 2010. It’s difficult to ascertain exactly how heavily the Swine Flu impacted the housing market, since as most HousingWire readers will probably recall, this period was in the dark days of the Great Recession, which was caused in large part by the most devastating meltdown in the history of the U.S. housing market.

Home sales and prices fell between 2007 and 2010 as the market worked through 6 million foreclosures, a peak-to-trough fall of over 35% in home values and unemployment rates that peaked at 10% and held steady at similar levels for many months. But interestingly – and somewhat counterintuitively – home sales went up on a month-over-month basis throughout the entire Swine Flu pandemic period.

Admittedly, neither of these prior pandemics had the kind of economic impact that COVID-19 has caused. The best recent proxy, in fact, probably isn’t a pandemic at all, but the terrorist attacks on Sept. 11. Like COVID-19, the terrorist attacks on Sept. 11 (and subsequent challenges, such as the Anthrax scare) brought the country to a virtual standstill and exacted an enormous financial and psychological toll on the entire country.

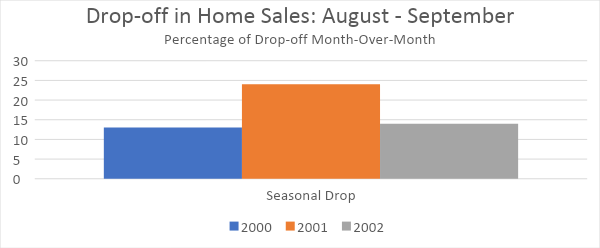

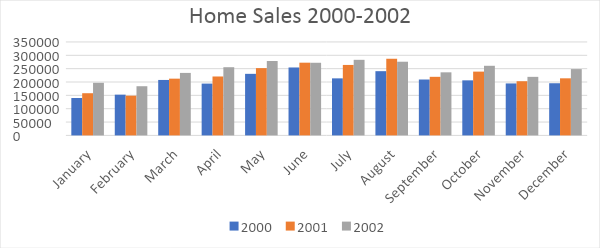

How did the housing market fare during and after this crisis? Home sales dipped in September – slightly more than the usual seasonal dip – following the attacks. But by October 2001, sales had rebounded and continued a stretch that saw monthly sales increases on a year-over-year basis for 20 of the 21 months between March 2001 and December 2002. Home prices also held up, increasing on a year-over-year basis every month during 2001 and 2002 – even in September 2001, the month of the attacks. Median prices rose during the period, from about $138,000 in January 2000 to $175,000 in December of 2002.

The U.S. housing market has proven to be incredibly resilient in the face of recent pandemics, and the economic shock that followed the Sept. 11 terrorist attacks. And even during periods where transaction volumes decreased, prices remained relatively stable, and ultimately increased.

The difficulty in using these prior events as a way to accurately predict the impact COVID-19 will have on the housing market is that none of them – SARS, H1N1, or 9/11– presented exactly the same set of healthcare and economic challenges that COVID-19 does.

It’s important to note that before the virus became a factor, the housing market was strong. There was high demand, a record level of homeowner equity, historically low delinquency and default rates, and two consecutive months of huge year-over-year increases in housing starts providing hope that much-needed inventory was on the way.

History suggests the housing market is likely to fare better through pandemics and recover more quickly than the overall economy or stock markets, but ultimately the fate of home sales and prices will be determined by how successful the country is at combatting the COVID-19 virus, and how many jobs are saved – and foreclosures prevented – by the economic stimulus programs deployed. But the housing market’s resiliency during prior crises and its strength entering this pandemic should at least give us reason to hope that it will recover relatively quickly, helping the rest of the U.S. economy get back on its feet.