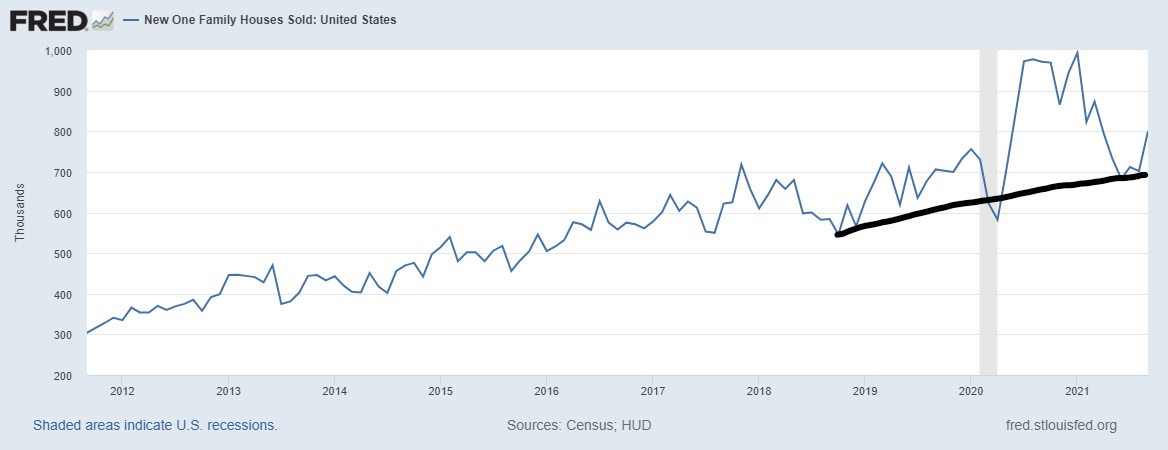

Today the Census Bureau reported new home sales came in as a beat of estimates at 800,000 and monthly supply of new homes broke under six months. However, the revisions were unfavorable, which should be noted since month-to-month data for new home sales can be wild and the revisions are a key trend to follow. However, the recent jump in the HMI data (builder confidence) can be attributed to a stabilization in the monthly supply data and a recent uptick in demand.

Census reported that “Sales of new single‐family houses in September 2021 were at a seasonally adjusted annual rate of 800,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 14.0 percent (±17.9 percent)* above the revised August rate of 702,000, but is 17.6 percent (±12.1 percent) below the September 2020 estimate of 971,000.”

Just to remind everyone, the year-over-year comps on all housing data should contain an asterisk because the make-up demand surge we saw toward the end of the last year created unrealistic comps. I knew some extreme YouTube fanatical housing crash bears would use the negative year-over-year data in purchase applications to promote a housing crash premise. This was why early in 2021, I wrote an article that said to expect that purchase application data would be negative but not overreact.

Certain people overreacted, and now, with the recent home sales data, they’re feeling the burn of a terrible premise. As I have stressed repeatedly, the doomsday trolling housing crash crowd are not data people; they don’t forecast anything. They just spend their adult life trolling the United States Of America and promoting the second housing bubble crash so people can click their sites. To be clear, we don’t see a crash in home sales as the recent existing home sales report showed.

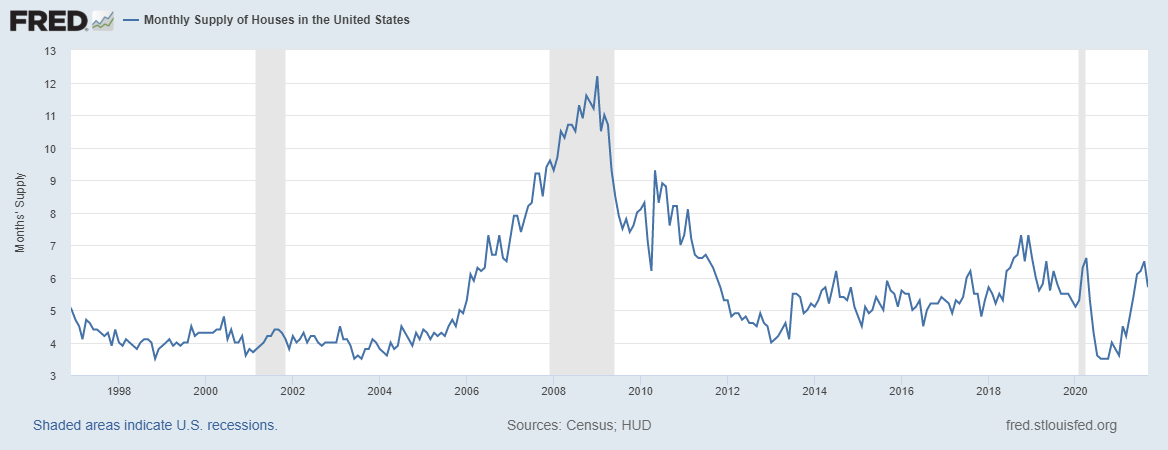

The monthly supply data — which I focus on more than any other housing data — came in at 5.7 months, the first time we have broken under six months since May of this year. The revisions in this report made last month’s monthly supply data higher. Revisions are always critical, so the three-month average in monthly supply is roughly 6.1 months.

From Census: “The seasonally‐adjusted estimate of new houses for sale at the end of September was 379,000. This represents a supply of 5.7 months at the current sales rate.”

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is an ok market for the builders. They will build as long as new home sales are growing.

- When supply is 6.5 months and above, the builders will pull back on construction.

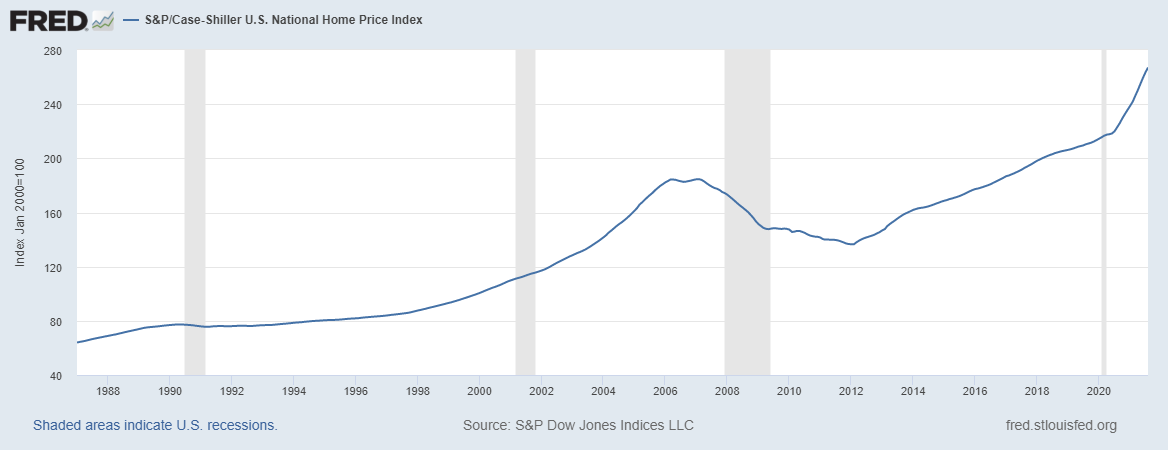

The one aspect of housing that isn’t going great in 2020-2021 is that home-price growth has taken off in an unhealthy way. If demographics is economics, then the years 2020-2024 were always different from 2008-2019. However, combining demographics, low mortgage rates, and all-time lows in total inventory levels, we see the outcome of this unhealthy economic cocktail.

From Census: “The median sales price of new houses sold in September 2021 was $408,800. The average sales price was $451,700.”

Of course, we see similar action in the S&P CoreLogic Case-Shiller report that also came out today. Hopefully, this is the peak rate of growth in home prices that we see this year. This is called sticky housing inflation, and it’s hard to get rid of, as you can see below, a deviation in the rate of growth in pricing in 2020-2021.

The new home sales sector is impacted by mortgage rates much more than the existing home sales marketplace. However, since the summer of 2020, I have believed the housing narrative would change, but it would need mortgage rates above 3.75% to occur. For that to happen, we would need to see the 10-year yield get above 1.94%. This was not part of my 2021 forecast, so the new home sales market can be stable until that occurs — if that occurs.

Even with all the growth, inflation data and taper talk, today the 10-year yield is 1.63%. The forecast range of 0.62% – 1.94% has stuck. However, going back to my America is Back economic model published on April 7, 2020, the main thing we need to see in 2021 is that the 10-year yield creates a range between 1.33% -1.60%, and it has flying red, white, and blue colors. A victory for America and a terrible two-year period for those pushing that our country was about to go into a depression.

Can mortgage rates get over 4% in the near term? Read more about that topic here.

Even though new home sales came in as beating estimates, the builder confidence data has recently picked up with existing home sales; I would label the new home sales market as just an Ok marketplace. Housing starts are going to be positive this year, even with all the supply and labor issues. Remember, the builders always complain a lot, but somehow they build homes when demand warrants it.

Next year, my long-term forecast call that housing starts would never start at 1.5 million or higher until 2020-2024 will finally be met. I know recently people were shocked that Wall Street Analyst Ivy Zelman stated that homes are currently 20% overbuilt. I give my take on that subject here.

For my economic work, I don’t believe in the housing construction boom or credit sales boom premise. I have always used the term demographic built-in replacement buyers’ demand in the years 2020-2024, so the housing market in 2020 and 2021 looks about right. Still, we did have unhealthy home-price growth, and that price inflation doesn’t get corrected like an overbought stock does in a day. With that said, the new home sales market is stabilized, with monthly supply still below 6.5 months, which means housing construction can continue for now.