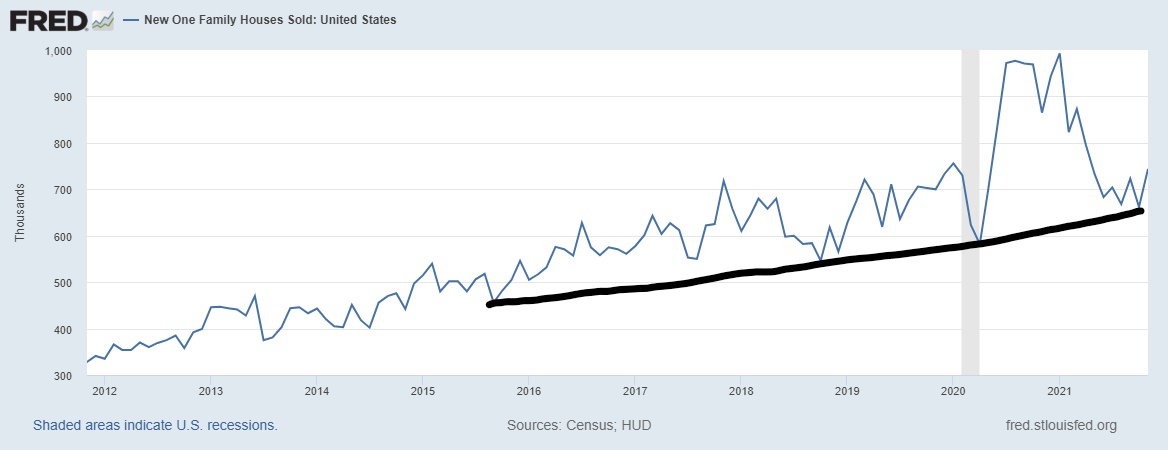

Today the Census Bureau‘s new home sales report came in as a missed estimate at 744,000. In addition, revisions were all negative, and the monthly supply of new homes rose. This is in contrast to the existing home sales market, which I would say is outperforming. With the recent growth in sales, the new home sales market is just OK and has been for some time. Given that, why has the builder’s confidence index risen so much in recent months?

Wait, doesn’t this sound almost exactly like what I wrote last month?

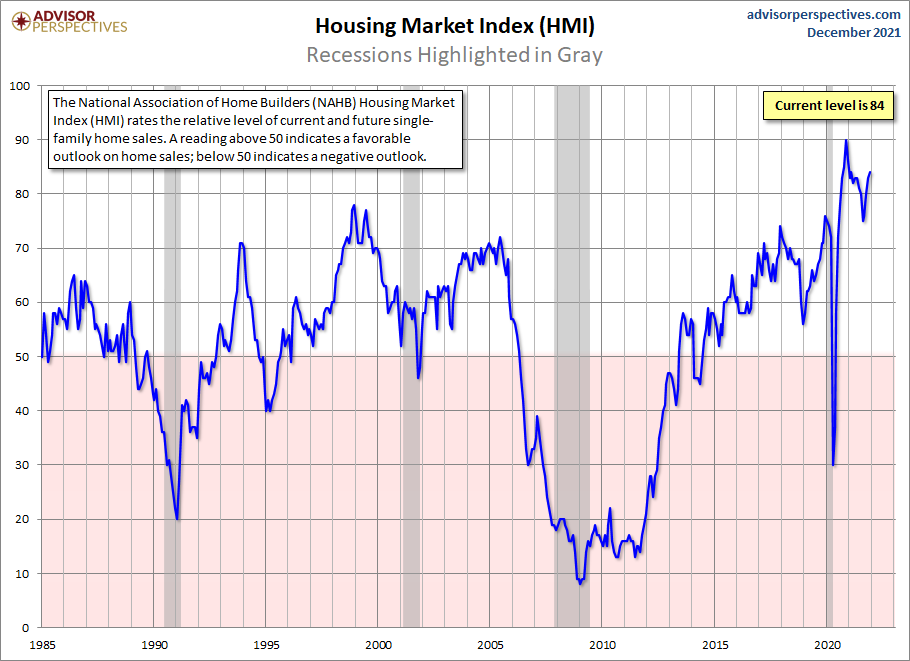

The builder’s confidence has picked up for months now, and housing permits have also done better. Much of housing data has gotten noticeably better: pending home sales, existing home sales and purchase application data have all had a nice run recently.

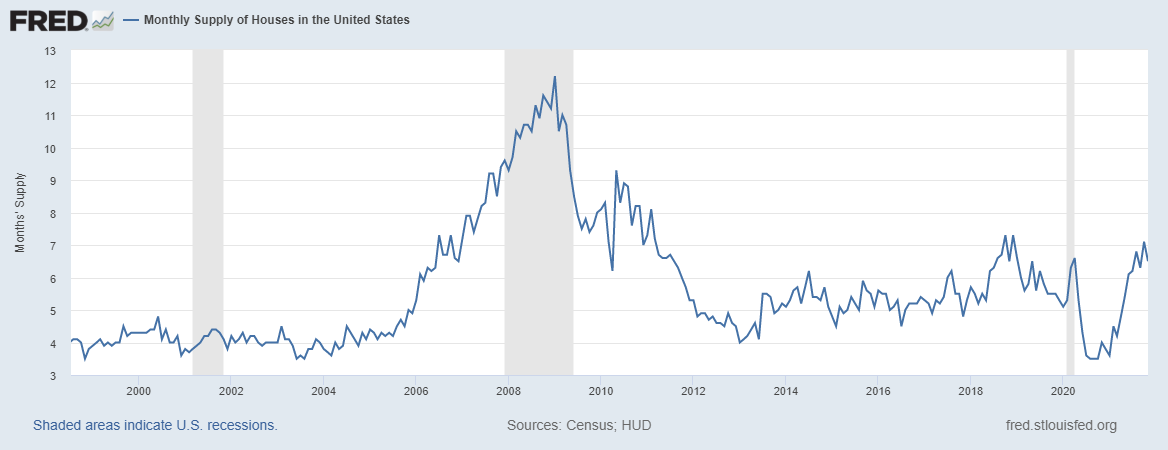

What happened this year in housing is the noticeable difference between the monthly supply data from new homes versus existing homes. The existing home monthly supply has been lower and heading lower toward the end of the year. The new home sales marketplace has had a noticeable increase and has stayed higher. The gap between the monthly supply of existing vs new homes is extremely glaring this year.

The monthly supply of existing homes at 2.1 months and total inventory are collapsing again and we might see new fresh all-time lows before the spring of 2022.

Now the new home sales market had a monthly supply spike this year, but it stabilized.

The headline number is at 6.5 months, the key level I have talked about for years, and the three-month average is at 6.63 months. This right here requires a red flag as the three-month average is above 6.5 months.

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months, and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- When supply is 6.5 months and above, the builders will pull back on construction.

From Census: For Sale Inventory and Months’ Supply: The seasonally‐adjusted estimate of new houses for sale at the end of November was 402,000. This represents a supply of 6.5 months at the current sales rate.

However, the difference now than what we saw in 2018 was that in 2018, mortgage rates were at 5% and monthly supply was spiking higher as new home sales were falling. The builder’s stocks were in a bear market as they were down over 20%. The 10-year yield was at 3.25% back then.

Today’s new home sales marketplace is a bit different, so let’s take a look at the report.

From Census: New Home Sales Sales of new single‐family houses in November 2021 were at a seasonally adjusted annual rate of 744,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 12.4 percent (±17.2 percent)* above the revised October rate of 662,000, but is 14.0 percent (±20.5 percent)* below the November 2020 estimate of 865,000.

New home sales have stabilized and are trending slightly higher now. It’s not as aggressive as the exiting home sales market, but still, that stabilization has given the builders the confidence to keep pushing permits.

One of the key reasons why the housing crash addicts from 2012-2019 failed badly — and ended up falling even more in 2020 and 2021 — was that we were never working from an overheated short-term credit housing boom that would be hard to sustain. This is such a critical factor in talking about housing and it does explain why America has so many bad housing crash people. It’s really hard to have a major bust when you never had a boom.

Also, note that demographics are solid in America and mortgage rates are near all-time lows. You can see why I have said for many years that these are not very talented individuals but awesome professional grifters.

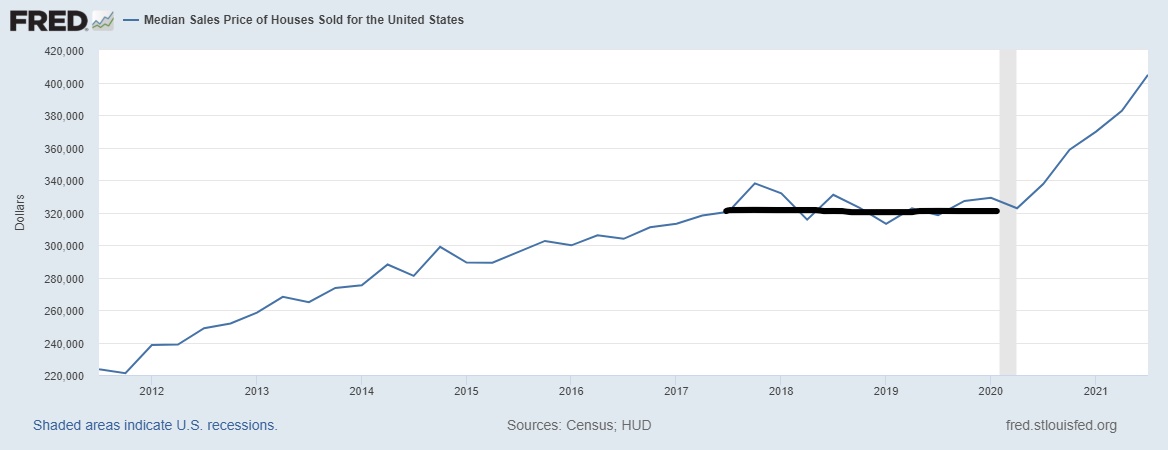

From Census:Sales Price The median sales price of new houses sold in November 2021 was $416,900. The average sales price was $481,700

Another big reason why the builders are so happy is that they have pricing power, and as you can see below, the median sales price in years 2020 and 2021 looks a lot different than what we saw the past few years. Just like the concern I had with home prices acceleratingin the existing home sales marketplace in 2021, this is not a forbearance crash. This type of price growth might be great for shareholders but it’s not the best for consumers.

The new home sales sector is really benefiting not only from good demographics but the fact that mortgage rates fell to all-time lows in 2020 and 2021. This and the shortages of homes in the existing home sales market brought a few buyers into this sector. A lot of smart Americans bet on the builders’ stocks doing great, and kudos to them for understanding this dynamic.

I can see why the builders’ confidence is rising. Their stocks are doing well, even with my red flag up due to monthly supply on the three-month average being above 6.5 months. My best advice is that the next few months of the new home sales report might have a bit more pick-up and a drawdown on inventory. Remember, this sector gets impacted by mortgage rates the most, so if the 10-year yield does rise above 1.94% and has duration, the conversation can be different.

However, today the 10-year yield is at 1.49% currently, which looks perfectly right to me. As I wrote about on April 7, 2020: When the economy is in recovery, the 10-year yield should be a range between 1.33%-1.60%. We saw that action this year and all looks right in the world to me.

Have a wonderful Merry Christmas, happy holidays and best wishes for the New Year. If you want to read about my 2022 Housing and Economic Forecast you can find that here, or if you would rather listen than read, I provided an overview of the forecast on this episode of the HousingWire Daily podcast.

Logan, as a homebuilder myself I can agree with your premise that a 3 month average of inventory exceeding 6.5 months of supply is unhealthy. However, that is not where we are. Nearly 9 months ago we stopped using MLS to see where new home inventory levels are. Here in Oklahoma City, more than 300 homes are listed, however a majority of these homes have not been started. The top builders here list hundreds of homes that will not be ready until late summer 2022. Most listings are renderings looking to sell a home to be built once contracted. This situation is not the same as true inventory on the ground.

In fact, recently Chuck Shinn, Phd., with Builder Partnerships recently stated that nationally “New home inventory has increased from a very low 3.5 months of supply to 6.3 months of supply. However, only 9.3% of the inventory is complete and ready for delivery which represents only 20 days of supply. Over 90% of new home inventory has not been started or is still under construction”. In my opinion,, new home inventory is not as concerning as you might think. I would argue that we are still in a very favorable inventory situation.