As we come to the end of 2021, we also approach the end of another year living with COVID-19. The year 2020 was one of the most chaotic times in recent history. Although 2021 seems normal in comparison, it is perhaps even stranger because as a country, we have learned to normalize the consumption of goods and services with an active virus infecting and killing Americans each day. An often-forgotten turn of luck for the American economy is that the housing market entered a period of the best housing demographics ever recorded in history the same year that COVID grabbed hold of us.

As I always stress every time I can, housing broke out before COVID-19 hit us. February data that we got in the second half of March was the first real breakout in housing data post-2010.

If COVID-19 had become the worldwide menace five years earlier, the U.S. would not have the demographic clout to drive the housing market — and it was the housing market that led us out of the COVID-19 brief recession. Yes, it was short; it ended in April of 2020.

Likewise, if the housing market did not have COVID-19 to dampen demand for a short time, we would not have to debate forbearance so much. The forbearance crash bros of 2020 blew it badly.

Even with COVID-19 casting a pall on an otherwise expanding economy, my biggest concern for the years 2020-2024 has been that the shortage of homes would lead to unhealthy price growth. This scenario started brewing in 2014 when inventory began falling. Purchase applications also began to grow, slowly at first, until the demographic push beginning in 2020.

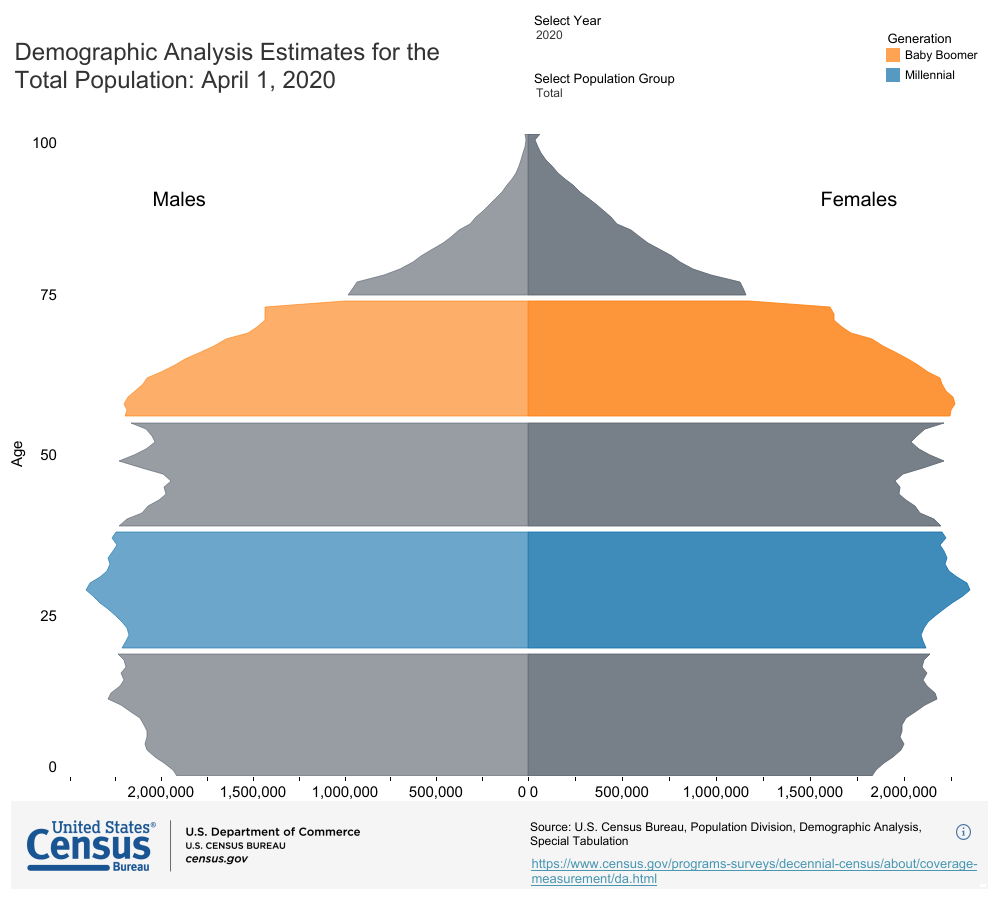

If housing was a book for 2021, we could title that book Demographics Equals Demand. We don’t even need a book — the title says it all. Mother demographics doesn’t care about your conspiracy bubble crashes from 2012-2021; she popped them.

Just for fun, though, let’s jump into the weeds and see what Mother Demographics has brought us for 2021 thus far:

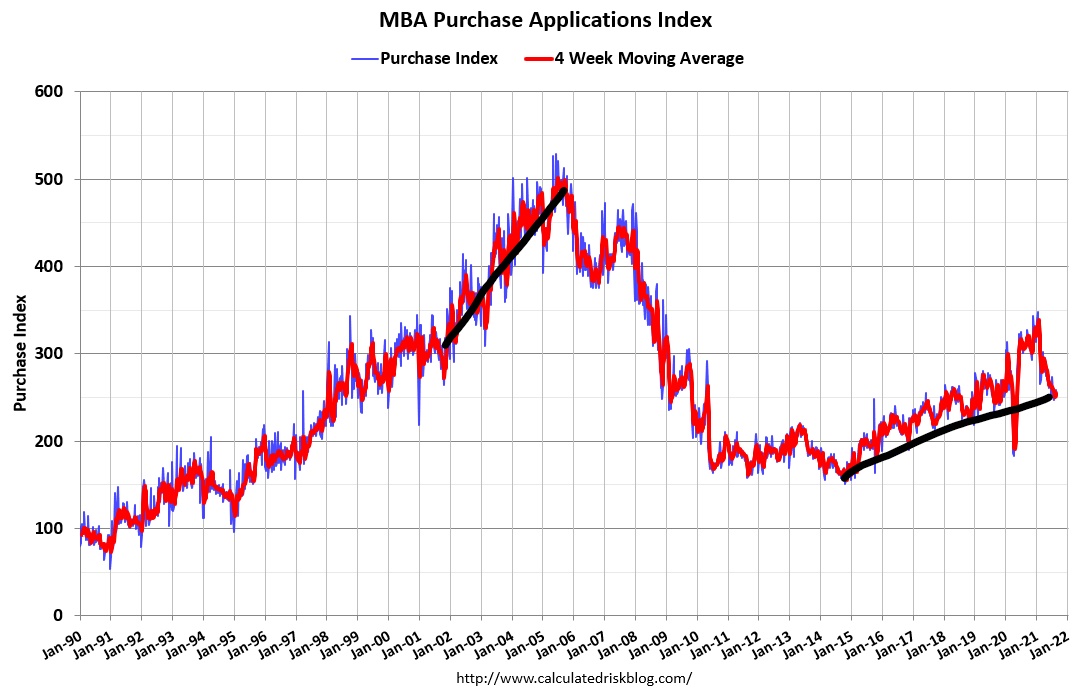

1. Purchase application data looks just right

I have always looked to purchase applications to determine growth in the market. The effects of COVID-19 severely skewed the data of this metric, stalling growth in early 2020, then front-loading all those delayed applications to late 2020 and early 2021.

This data line is very seasonal; the critical timeframe is from the second week of January to the first week of May. This tells you pretty much how the year is going to go since after May, total volumes fall. Well, COVID-19 delayed the seasonal volume last year and created a massive make-up demand surge in the second half of May in 2020, so all year-over-year comps are useless without adjustments.

It was going to be too strong early in the year, and in the second half of 2021, purchase application data will be negative year over year. I wrote an article earlier in the year saying this would be the case and don’t overreact to it.

I already see people saying that purchase application data is down year over year 18%, and housing is crashing. No, it isn’t; that is what we call amateur hour. Really there’s not much happening in year-over-year purchase application growth — and I say this as the early demand in the year from the second week January to Feb 17 was showing on average 14.8% year-over-year growth using tough 2020 comps. I discounted that growth as part of the make-up demand.

By make-up demand, I mean that we never got back all the sales we should have in 2020 due to COVID-19. We ended the year shy of what I believe the data line in January and February was telling us. Some of that spilled into 2021. This means that housing purchase application comps will be high up until mid-February 2022, then we can start back to normal.

Seasonality came back to this data line, so everything looks just right after you make some major COVID-19 adjustments. Remember, this isn’t a credit boom like what we saw from 2002-2005; it’s much different this time around.

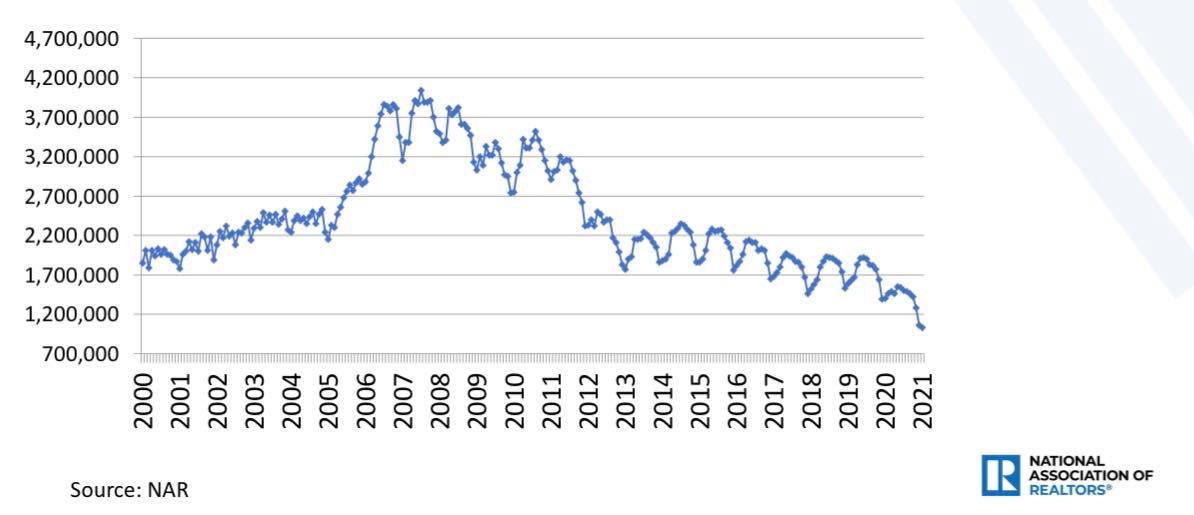

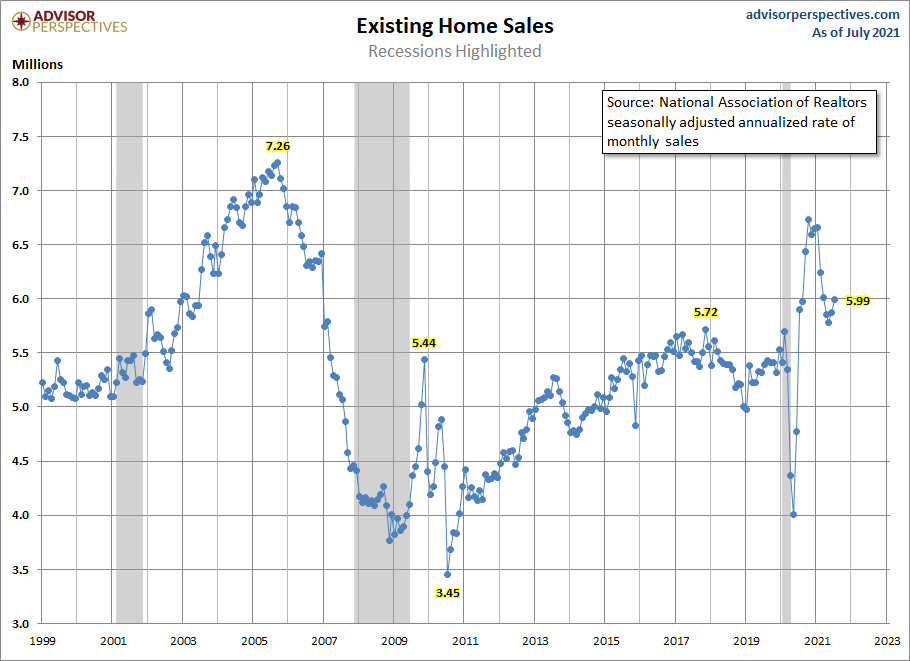

2. Existing home sales

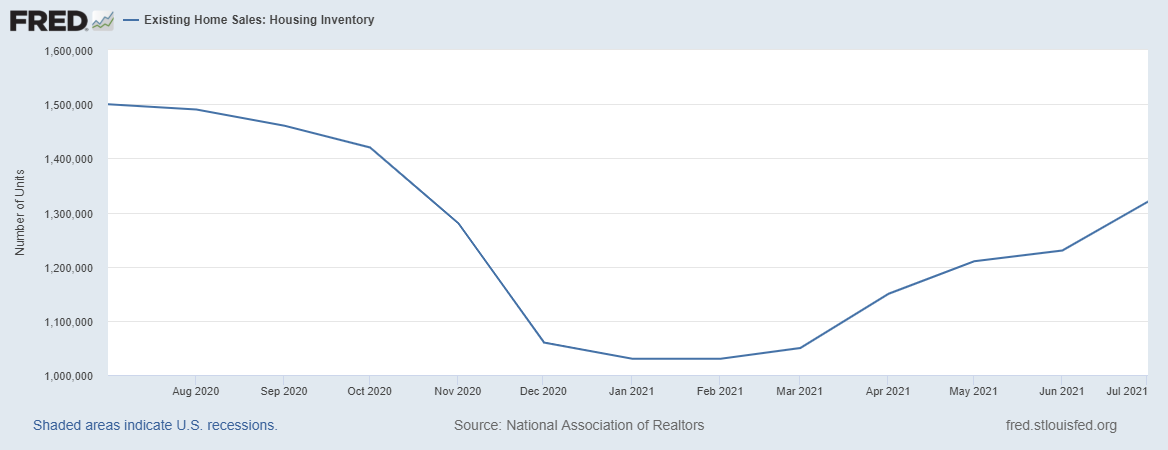

Existing home sales is another data line that just went haywire crazy in the second half of 2020 due to just make-up demand, nothing else. There was no sales boom in 2020 as we ended the year with just 5,640,000 existing home sales, which was only 130,000 more than 2017 levels. A big theme of my work at the end of summer 2020 was that housing data would moderate and don’t read too much into that moderation. Housing data will try to find a base to work from; it’s not crashing. That is precisely what has happened in 2021

Early in the year, with the front-loaded purchase applications data, after making some adjustments, I wrote: “The rule of thumb I am using for 2021 is that existing home sales if they’re doing good, should be trending between 5,840,000 – 6,200,000. This, to me, would be considered a good year for housing. This also means that we should have some prints above 6,200,000, like we have had already, and below 5,840,000, which hasn’t happened yet.”

So far, we have only had one print under 5,840,000, and while I do expect to see some more prints under that number, existing home sales look just about right. if anything, if we don’t see some prints under 5,840,000 that would be considered a slight beat in my eye. Just remember that every existing home sales print that we have had this year has been higher than what we closed at in 2020.

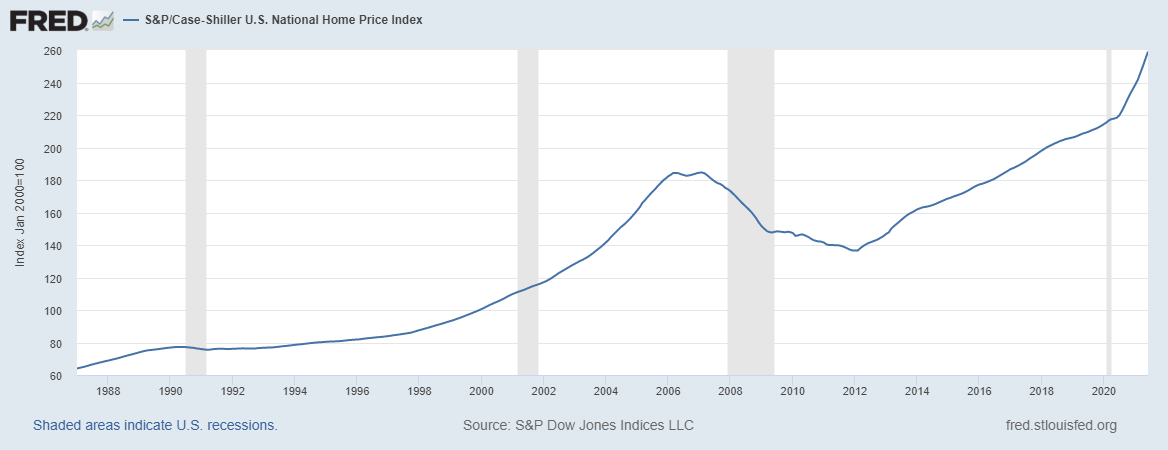

3 Home prices and higher rent

This is the worst aspect of housing in 2021 and was my biggest fear. In almost every interview I have given this year, I always stress this is the unhealthiest housing market post-2010. Not because we have a credit boom that creates an overheating demand cycle that will collapse any second. The simple raw shortages of homes in 2021 have created the unhealthiest home-price growth we have ever seen.

As you can see below, there is a glaring deviation from the trend in home-price growth in the year 2020 and continued into 2021.

Now it’s moving into the rental area as well. Demographics equal demand, shelter is just as important as having access to a bathroom, food, water, and clothing and people need somewhere to live. As I discussed with USA Today recently, we have many young people who need shelter, which will drive up rents.

We also have a a lot of Americans who are ages 34-65 as well, who aren’t going to be homebuyers or homeowners and they will rent. Also, the shortage of homes in 2021 has left some buyers with a bad taste as they have been outbid on the home they want to get. This is forcing them to rent even longer. You can see why many people seeking shelter would be frustrated with the process this year.

Unlike a meme stock, this home price and rent inflation is sticky. Moderation in the rate of growth in home prices and rising rents should occur, but it won’t move like certain stocks have. We do have some variables that can create some short-term supply relief. However, the damage has been done. Because of this alone, 2021 was the unhealthiest housing market post-2010.

With the year almost done, what can we expect for fall and winter?

I have stressed over the years that we had our best existing home sales prints in the fall and winter in the previous expansion, so don’t neglect the existing home sales data. If I am wrong and we don’t see some prints under 5,840,000, this means housing demand stuck very well even with the massive price gains in 2020 and 2021. My No. 1 focus for the housing market is to see levels rise on the inventory side. We have seen the seasonal increase in inventory this year, working from all-time lows.

So far, they haven’t increased as much as I would like, and now it’s the last 3.5 months of the year; this is typically when people take their homes off the market. I am hoping that we can just keep these gains and go higher into 2022. However, seasonality is a potent force in housing economics and might be wishful thinking on my part.

As I have written many times before, we would love to see inventory levels get toward 1.52 – 1.93 million, and even though that isn’t historically high, that is good enough to get the multiple price bid action off the books. That would be the most bullish event for housing. I modeled out 23% cumulative home-price growth during 2020-2024 as being good enough to keep things at bay with where wage growth was going. That number has been smashed in less than two years, and that to me isn’t a good thing.

The only way to solve this action is more inventory because demand is stable. Even though I believe the housing market can change with mortgage rates over 3.75%, that wasn’t a 2021 story. That wasn’t my forecast for 2021. I capped out my 10-year yield forecast at 1.94% and the highest we have gotten has been 1.75%. We will need a 10-year yield of over 1.94% to get mortgage rates over 3.75%.

So if you’re looking forward to a happy holiday season for housing, we need a lot more inventory to calm this housing market down because the last two years of price growth and lack of homes have created a humbug attitude for some homebuyers and renters.