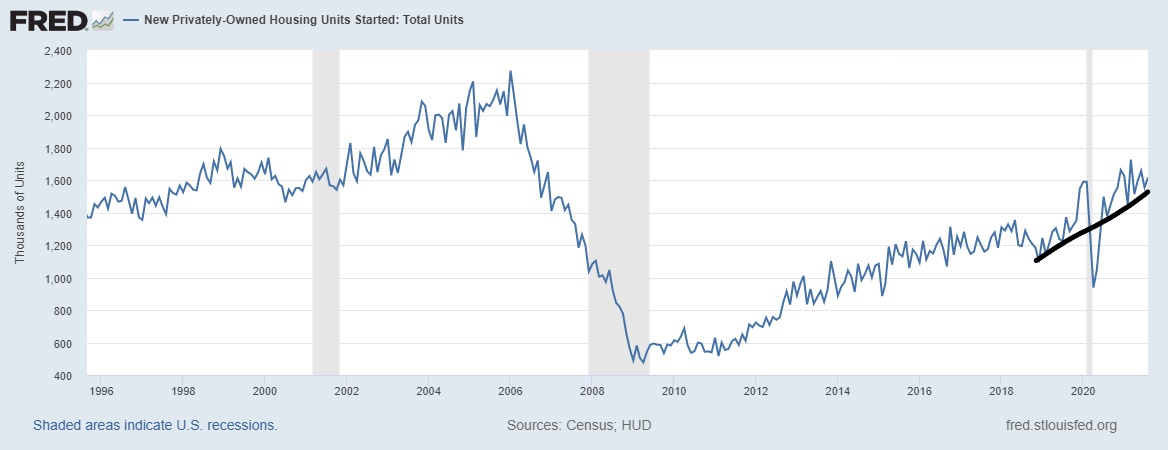

On Tuesday, the U.S. Census Bureau reported that housing starts hit 1,615,000 for August and housing permits came in nicely at 1,728,000. These data lines beat expectations, and we had slight positive revisions to the previous months — overall, a good report on all fronts.

I have always been mindful that the month-to-month housing starts data can be wild, both positive and negative, so the trend is what matters the most. The movement says slow and steady is bringing sexy back to the housing data, and the wild action we saw due to COVID-19 is moderating.

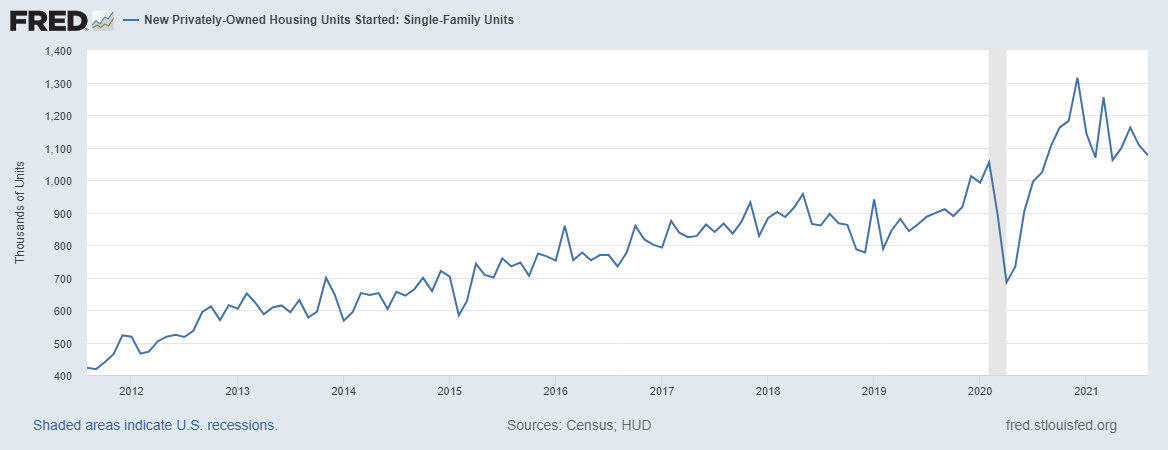

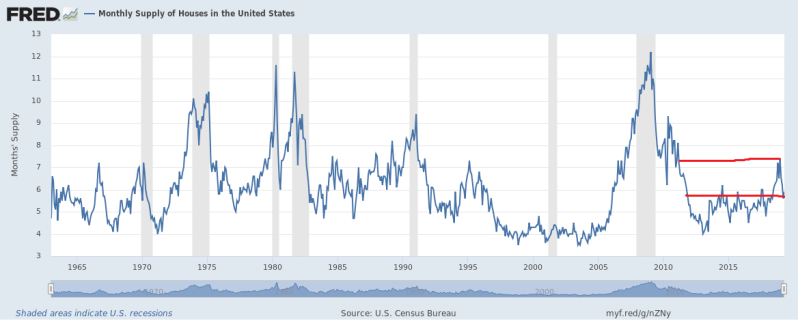

Single-family starts have been slowing recently to move along with the moderation in new home sales and the rise in monthly supply.

However, a lot of housing data was going to moderate from the massive distortion COVID-19 created in the data lines. The key is always knowing the difference from fundamental weakness in the data and what is returning to a normal base from an extreme move. This is why I believed it was vital for me to discuss the fact that housing data was going to moderate and be careful not to read too much in that moderation.

Unfortunately, our housing crash bros sounded the alarm too early again when they saw the decline in many housing data lines from their recent COVID-19 peaks. This is very common as this sensitive lot tends to believe they’re Wile Coyote, and every weakness is sending our friend to hold up the sign that says That’s All Folks before falling down a cliff.

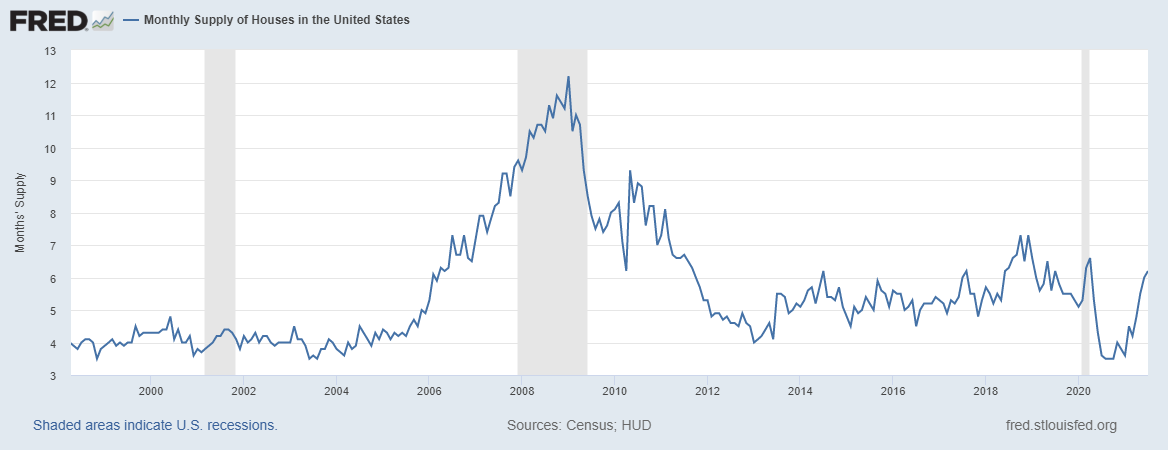

This is why I emphasize following this rule of thumb for the housing sector with new home sales and housing starts. The critical data line to track is the monthly supply data. Below 4.3 months, life is excellent for the builders; from 4.4 to 6.4 months of inventory, the builder’s life is ok. When inventory is over 6.5 months, builders start to pull back on construction to control pricing. Always use a three-month average when looking at the new home supply data.

The report on new home sales is coming up, and for now, life is still ok for the builders. I know this isn’t the most exciting take, but we stick to our models for a reason because they keep us in the lanes.

From Census: Privately‐owned housing starts in August were at a seasonally adjusted annual rate of 1,615,000. This is 3.9 percent (±11.3 percent)* above the revised July estimate of 1,554,000 and is 17.4 percent (±12.1 percent) above the August 2020 rate of 1,376,000. Single‐family housing starts in August were at a rate of 1,076,000; this is 2.8 percent (±10.4 percent)* below the revised July figure of 1,107,000. The August rate for units in buildings with five units or more was 530,000

As you can see below, the housing starts uptrend is still intact from the lows we saw in 2018. Housing starts were doing well right before COVID-19 hit us, and that quick drop in the data recovered quickly, as most housing data lines have.

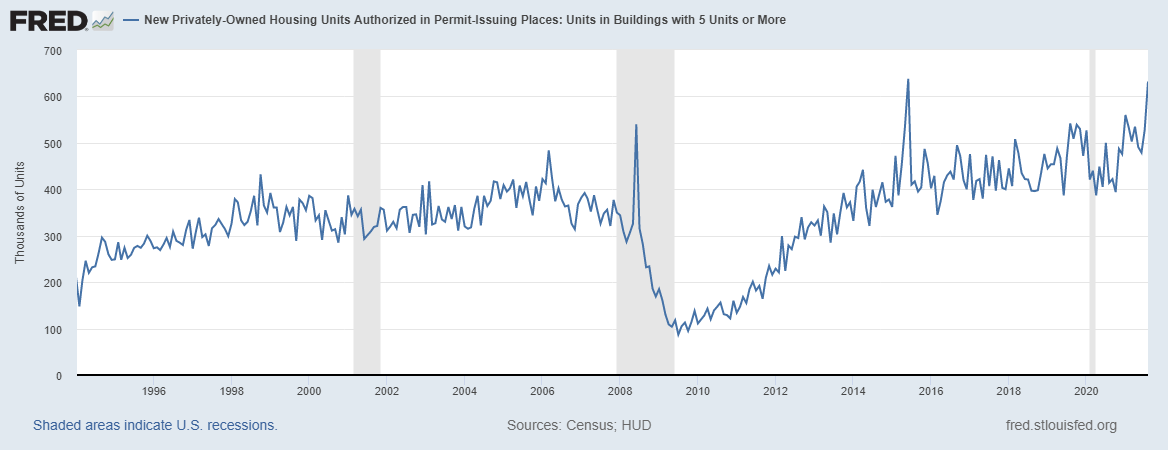

From Census: Privately‐owned housing units authorized by building permits in August were at a seasonally adjusted annual rate of 1,728,000. This is 6.0 percent (±1.4 percent) above the revised July rate of 1,630,000 and is 13.5 percent (±1.8 percent) above the August 2020 rate of 1,522,000. Single‐family authorizations in August were at a rate of 1,054,000; this is 0.6 percent (±1.3 percent)* above the revised July figure of 1,048,000. Authorizations of units in buildings with five units or more were at a rate of 632,000 in August

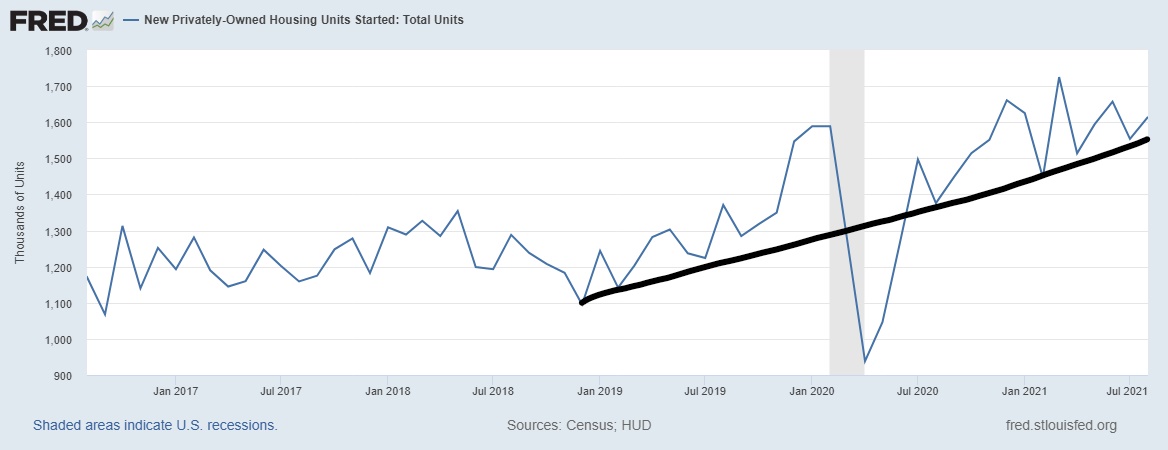

Housing permits had an epic rebound and had moderated from that big move. However, as you can see below, the uptrend was still intact from the lows in 2018. Housing permits, for me, is one of the most important housing and economic data lines we have in America. As long as housing permits are moving upward, not only is housing doing ok but the economic expansion is moving along nicely post-1996.

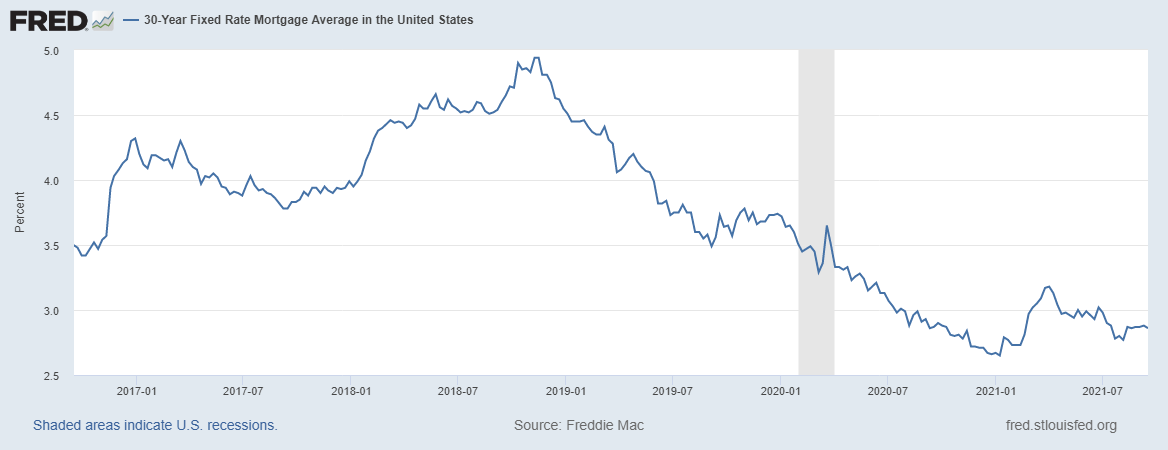

The last time we had a noticeable weakness in housing — excluding COVID-19 — was back in 2018 when mortgage rates got to 5%. Currently, rates now are under 3%.

During that time, monthly supply for the builders spiked to above my crucial level of 6.5 months, and homebuilders’ stock prices were down over 20% plus from their recent peaks.

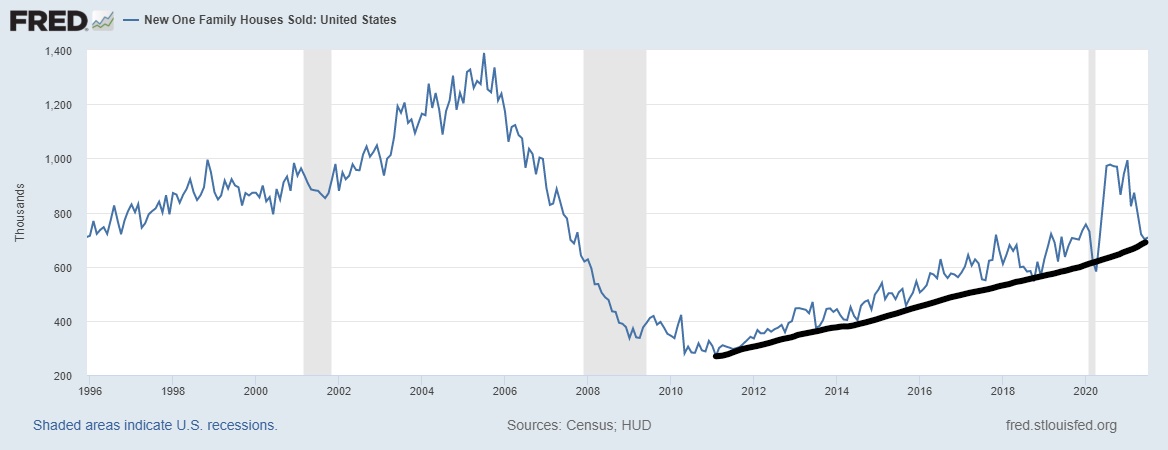

Back then, I argued that housing starts and new home sales are too low historically to call this a housing top, and we are running into the best housing demographic patch ever. While housing starts were stalled for a bit, demand for new home sales grew again, and in 2019 monthly supply came back down.

This is why following monthly supply data is critical for housing starts because you understand what the builders are dealing with. Below is the monthly supply data in the first few months of 2019. As you can see, the monthly supply fell, and the builders got more confident to build.

We can take away from this report that single-family housing starts softness is being offset by multifamily construction strength. The builders are very mindful of how much price cost inflation they have added for consumers. The consumer was willing to pay for it, but they didn’t want to push this too much. When you have pricing power, it’s a good thing but that can also lead to some pain in the future.

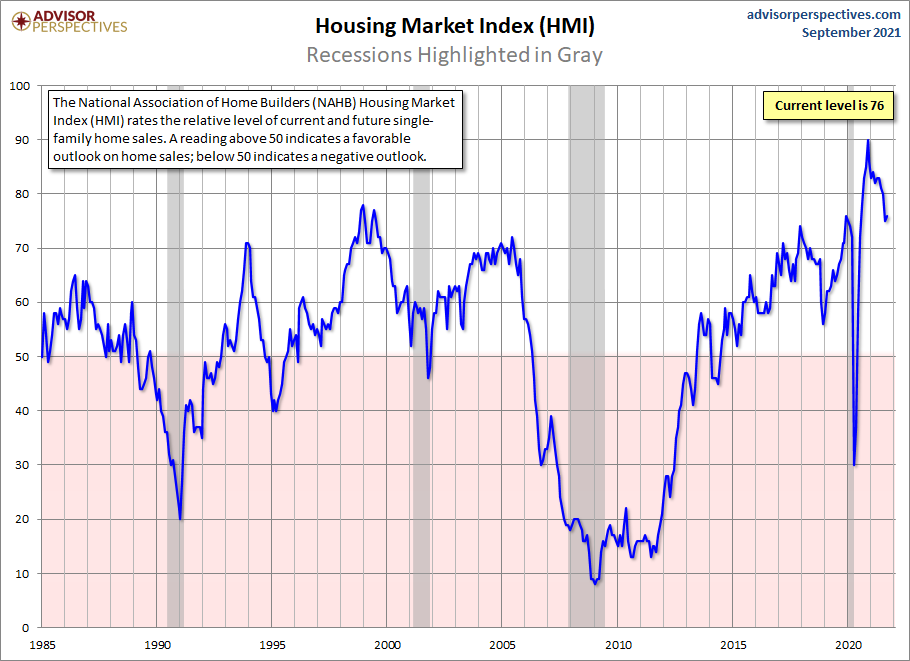

Builders’ confidence held up in yesterday’s report, and this data line’s moderation should have been expected. Also, don’t look at the historically high levels in this index as a barometer of where starts should be. This is a survey, and the short-term directional move gives you a better idea of what the builders are thinking. We saw a slight uptick yesterday. A lot of housing data is finding its proper base to work from, which will make 2022 a bit more calm in reading data trends.

If people are looking for a housing construction boom — which even today, I don’t believe we will see to the satisfaction of those who are saying we are 3 million to 5 million housing starts short — we are simply going to need to see a boom in new home sales. As you can see below, we are nowhere close to the new home sales peak we saw during the housing bubble years.

Multifamily construction has been solid recently, and that is such a plus for the United States of America.

Still, without a boom in new home sales, the levels that people want housing starts to be at simply won’t happen.