With the July 4th weekend nearly upon us, it’s time to reflect on all that we have been through in the past year and how, as a country, we have overcome so many daunting obstacles, including what we have been through in the housing market.

The first thing that pops into my shriveled brain is how the housing market looked in February of 2020. Data from that month showed that housing was breaking out — but because we received this data in March of 2020, we were all too busy trying to survive to take notice.

Once the fear of the virus calmed down, we began a truly remarkable economic comeback, perhaps the fastest economic comeback from a significant economic downturn in the history of the U.S., with the housing market leading the way.

But for every silver lining there is a cloud.

The solid demographics for home purchasing and historically low mortgage rates — which have been in a downtrend for four decades — have created a housing market where prices are rising too fast. Even though we have good demographics for housing, we are not seeing a growth in sales that would account for the rate of growth in prices.

Before COVID-19 was even a whisper in our minds, I thought that in the years 2022 and 2023, price pressures for housing could be the big story. But I expected that higher mortgage rates of over 4% would keep prices from escalating out of control.

Instead, demand picked up early and because of the effects of COVID-19 on the world economies, mortgage rates are down to all-time lows. Rates haven’t even gotten to 3.5% recently — forget getting above 4%. These low mortgage rates are being sustained in a climate of some of the best economic growth in the 21st century and hotter-than-normal inflation data.

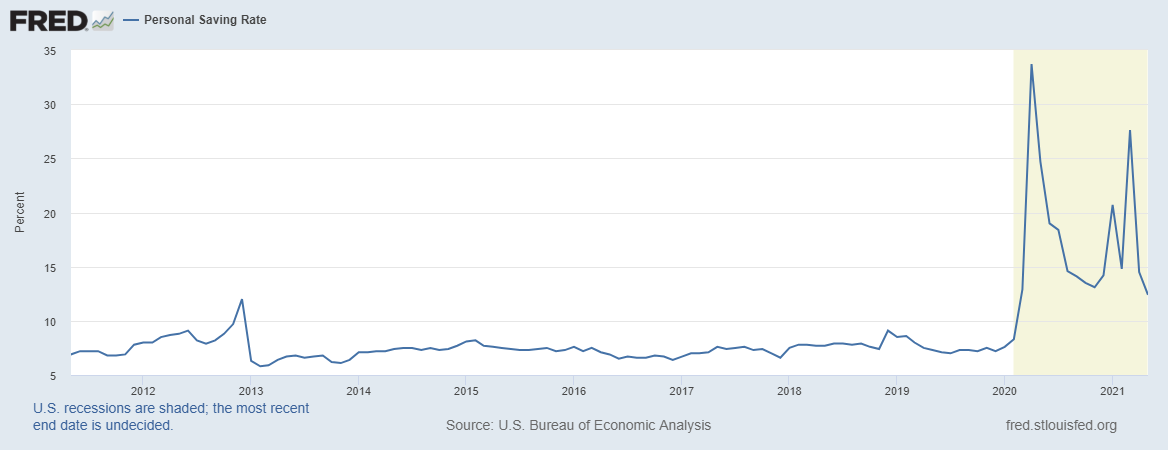

In this first year of economic expansion, we continue to have a good savings rate and healthy household formation demographics.

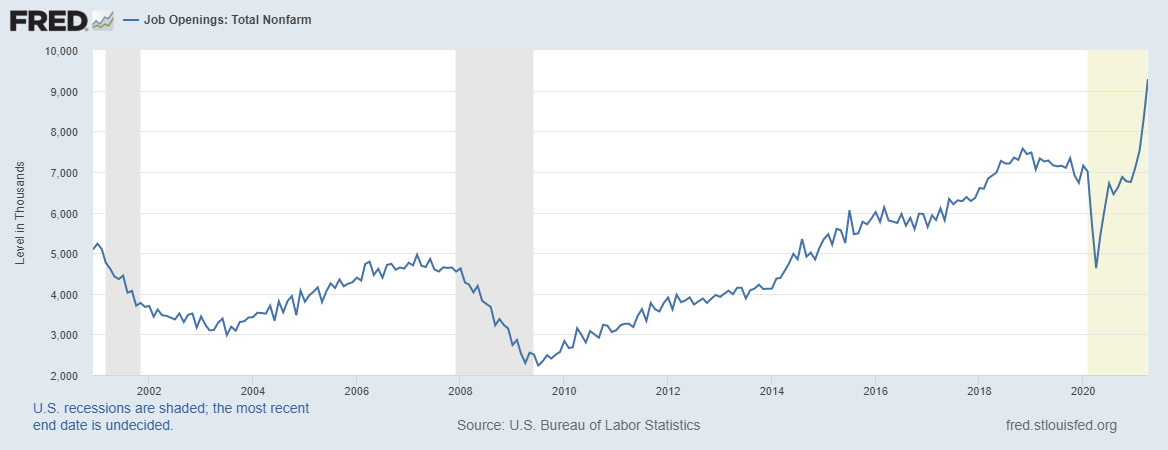

I anticipate that by September 2022, we will have all the jobs back that were lost due to COVID-19. When one considers that we currently have the most job openings ever recorded in U.S. history, (9.3 million) this date does not seem to be a stretch. Note, too, that all this good economic mojo is going on before we have even started fiscal spending on infrastructure.

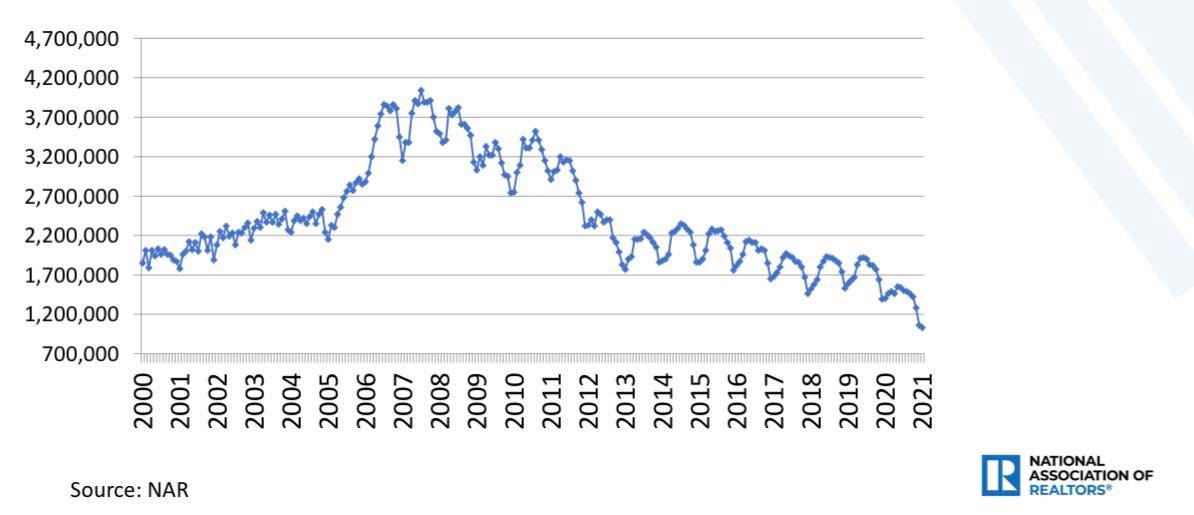

With this recipe of excellent national economics, good demographics for housing, an improving employment picture and low mortgage rates, it makes sense that home prices would be hotter than normal. But as I have said before, the high rates of growth in home prices have been more a function of low housing inventory than extreme credit growth in demand.

But all is not hopeless: There are several reasons why housing inventory should pick up in the next several months and going into 2022.

First, the higher prices we are seeing in the current market are making it difficult for some buyers to compete. Clearly not all buyers, but enough to keep the extreme low housing inventory levels hard to maintain. This is a key point, but because we got to all-time lows in housing inventory, a move higher from these extreme low levels isn’t saying too much.

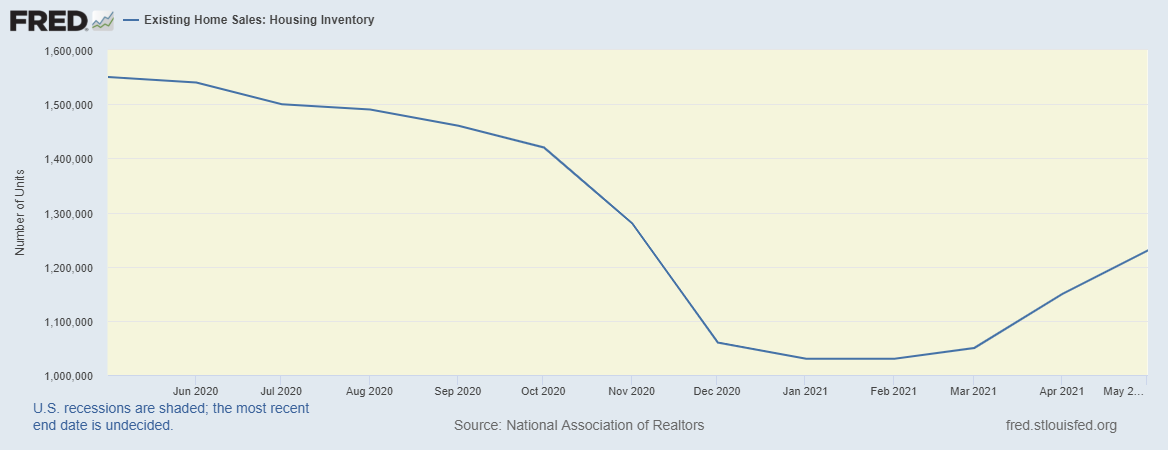

From the NAR:

Second, forbearance programs and the eviction moratorium will be ending soon. Because loan holders started their forbearance programs at different times they will exit the programs at different times, too, so don’t expect a flood of housing inventory to appear at once. Forbearance programs have gone from near 5 million loans to a tad over 2 million. A lot of primary-residence households on forbearance programs have already exited the program and housing inventory remains chronically low.

Nevertheless we can expect some of these homes to come on to the market. These homes might be mom and pop landlords who were unable to collect rent during COVID-19 and want out of the rental game or some investors looking to cash in on high home prices. In any case, to think that we would have zero housing inventory created from this crisis is highly unlikely.

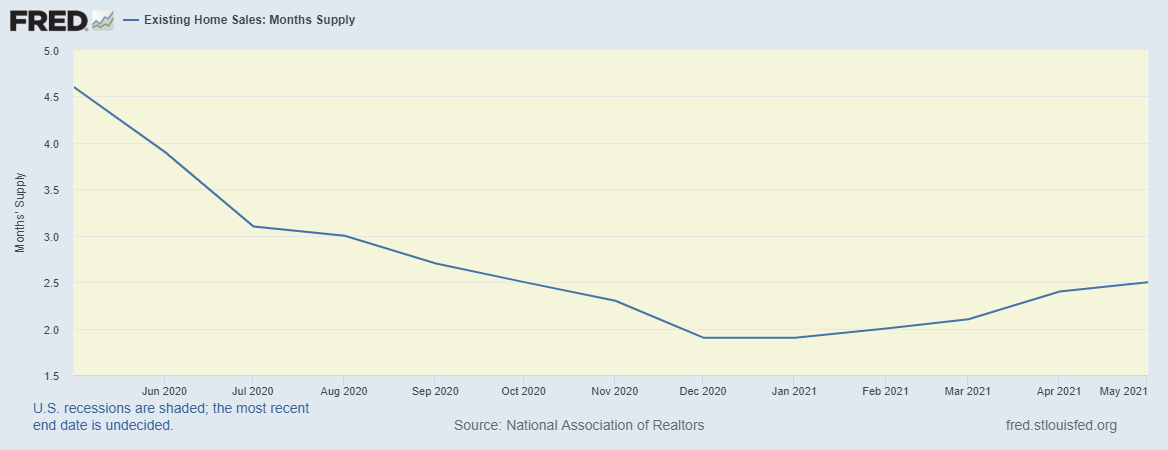

Third, while demand is solid in 2021, and we should have slightly more total home sales than we had in 2020, we are not seeing growth in credit (number of mortgages taken out). To think that we would have double-digit price growth with essentially slight home sales growth is the essence of bad inflation. As you can see below, what we experienced from 2018 to 2021 looks nothing like the credit growth we saw from 2002-2005.

We got to all-time lows in housing inventory recently so any increase is going to be a high percentage increase and that is going to fool some folks that the housing inventory picture has changed dramatically. The actual number of homes making up that increase is not going to be much, however, so don’t look at it like that. Instead look to see if total housing inventory gets back to the levels we saw in early 2020.

Getting back to 2020 levels with days on market going past the teens is the No. 1 priority for the housing market. We need more than the typical rise due to seasonality that happens every spring. We want total inventory levels to go above 1,520,000 at minimum.

In 2018-2019, total housing inventory was in the range between 1,520,000 – 1,920,000 and that level of inventory helped to drive real home-price growth in 2019 into negative territory briefly. Existing home sales during those years stayed in the monthly sale range of 4,980,000 to 5,610,000 homes. More importantly, the days on market were higher than what we see today — and as such we had fewer bidding wars and less price growth.

The effect of higher mortgage rates, which in late 2018 got to 5%, also contributed to more stability in housing prices. 2018 and 2019 were more balanced markets, so in my view it was a healthier housing market compared to what we have today.

Once the 10-year yield gets above 1.94%, which should bring mortgage rates above 3.75%, then things should cool down enough to stabilize the unhealthy price gains we are currently experiencing. The 10-year at 1.94% is not a very high bar, but even so, that is higher than what I have forecasted for 2021.

If housing demand is better than I thought going into the demographic sweet spot years of 2022 and 2023, then housing inventory may not improve much. I still believe in my replacement buyer premise rather than a credit boom housing market. However, if I am wrong, then we will see it for sure in years 2022 and 2023. The price gains in 2020 and 2021 have already met the target that I anticipated to be cumulative for the five-year period of 2020 to 2024. This pathway explains my concern over what has happened recently.

During the years 2020 to 2024, I anticipated total sales (new and existing homes combined) to stay at 6.2 million or higher. The only way I saw this not happening was if home prices got out of hand early on, and guess what, that has happened. While we won’t break lower than 6.2 million in 2021, I am mindful of these recent price gains in both exiting and the new home sales market. Demand for existing homes will come from first-time homebuyers, cash buyers, investors, move-up and move-down buyers. The bump in demographics in the years 2020-2024 has already showed itself to be a powerful economic force for the United States of America.

All these buyer types will create steady replacement demand for the existing home market. The new home sales market, on the other hand, is driven by wealthier older buyers with mortgages. For this reason, new home sales are more dependent on mortgage rates. I recently expressed some concern in this market here.

More than anything, I am hoping that what happened in 2013-2014 and 2018-2019 happens again. During those periods, interest rates went up, which increased housing inventory and days on the market. The additional supply cooled the rate of growth of home prices and stopped the bidding wars. Unless we get an increase in housing inventory from softening demand or end-of-forbearance selling, only an interest rate increase will get us above 1,520,000 total housing inventory and out of the low housing inventory/high price quagmire we have been in since the summer of 2020, which has been most unhealthy housing market post-2008. Still, these are first world problems. I mean, come on, it’s not like we are having a bubble crash like some bros wanted to see.