The National Association of Realtors reported 5.99 million home sales for July, which was an excellent beat of estimates and a dagger into the hearts of the 2021 housing crash crew. Mother demographics and low mortgage rates, two things that have been transparent to human beings for a long time, are powerful economic forces. Both together make it very difficult for an epic housing crash in sales to happen, especially when the years 2008-2019 had the weakest housing recovery ever.

We were never working from an elevated level of sales in the existing home sales market as we ended 2020 with just 5,640,000, which was only 130,000 more than 2017 levels. The notion that sales would simply collapse by 2-3 million levels like what we saw from the peak of the housing bubble year at 7,260,000 to as low as a bit under 4 million is entering internet conspiracy levels. As I showed here, the market we have currently isn’t 2008 all over again.

I suggest after 10 years of being wrong on the housing crash call and now needing a 86% home price crash to just get back to 2012 levels, my best advice is to get some therapy for Housing Bubble Boy 2.0 sickness. You still have time, life is worth living free from this disease.

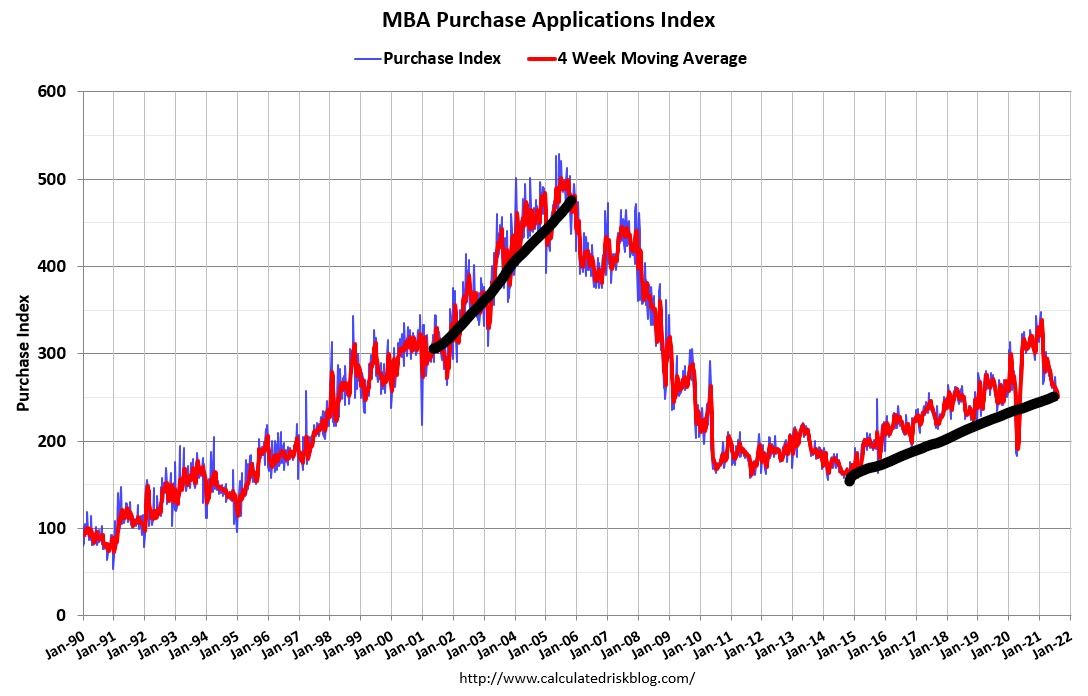

The sales data trend, which I have always believed is the best way to look at demand using the purchase application data as a reference, has been in line with what I talked about back in March of this year. As I wrote then, the rule of thumb I am using for 2021 is that existing home sales, if they’re doing good, should be trending between 5,840,000-6,200,000. This, to me, would be considered a good year for housing.

However, I had anticipated some existing home sales prints under 5,840,000 this year, and so far, we have only gotten one of those.

So far, 2021 looks about right. if we don’t see some prints below 5,840,000, I would consider it slightly better than my estimates. Remember that COVID-19 has created many distortions in economic data. Since the end of last year, my theme is that housing is going to moderate, but don’t over-read that moderation in the data.

We are trying to find a base to work from that is more traditional with standard housing data. We are getting there, and then we can go back to normal. I am not, nor will I ever be, a housing sales or construction boom person. However, I am a big believer in demographic replacement buyer demand. If total home sales (new + existing) are over 6.2 million each year from 2020 through 2024, I would consider that a beat.

That happened in 2020 and 2021, and it’s something that couldn’t have happened in 2008-2019. Everything looks fine except that this housing market is very unhealthy due to a lack of inventory and home price growth. Until the days on market grow, I will still say this is the unhealthiest housing market post-2010. Not for the reasons we had in 2002-2008, where we had a credit boom that couldn’t be sustained.

It’s because Americans want somewhere to live, and they’re forced to bid on shelter because of the lack of homes, leading to excessive home price growth. This type of price growth is not a positive in any shape or form whatsoever and was my biggest concern in 2021.

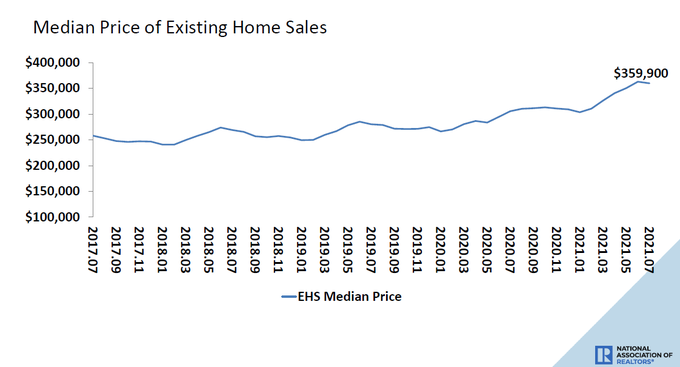

NAR Research shows that the median existing-home price for all housing types in July was $359,900, up 17.8% from July 2020 ($305,600), as each region saw prices climb.

Looking ahead, this is going to be a key talking point for housing data that needs some context. The key: We are about to enter the months where home sales data will be negative year over year. Many trolling Twitter accounts and terrible YouTube crash sites will not present the data with the context that the comps from last year are COVID-19 makeup demand; ignore it.

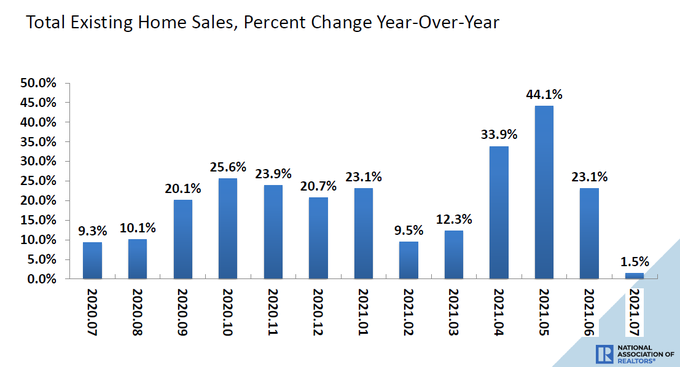

As NAR Research shows, sales inched up year-over-year, increasing 1.5% from a year ago (5.90 million in July 2020).

Just like you should have ignored the more robust year-over-year sales data and purchase application data due to the COVID-19 lows in demand, you should not pay too much attention to the year-over-year weaker data as well.

One of the critical data lines that I want to see get better is the days on the market. So far, it hasn’t done this at all in 2021; demand is simply too good to allow this to occur. However, once we can get back to 30 days and higher, more Americans will have choices to buy homes and we will get less bidding action. Also, some sellers will feel more comfortable selling their homes and being able to get the home they want.

Another key point I would like to make, for all the hype that Wall Street investors are propping up this housing market, sales to investors have had no growth year over year in this report. For sure, investors and cash buyers are part of the more considerable demand discussion. I always talk about how people need to look at demand in total — from millennials, move up, move down, cash and investor buyers. Don’t overhype the story that this is all Wall Street. Mother demographics are the most potent economic force globally, and primary resident mortgage buyers still drive housing; when they fade, so does housing. I wouldn’t put too much faith in the story that housing can never fade due to wall street investors.

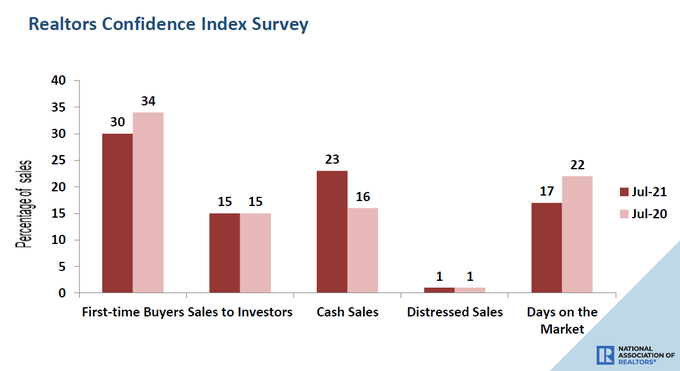

According to NAR Research, first-time buyers accounted for 30% of sales in July; Individual investors purchased 15% of homes; All-cash sales accounted for 23% of transactions. Distressed sales represented less than 1% of sales and properties typically remained on the market for 17 days in July.

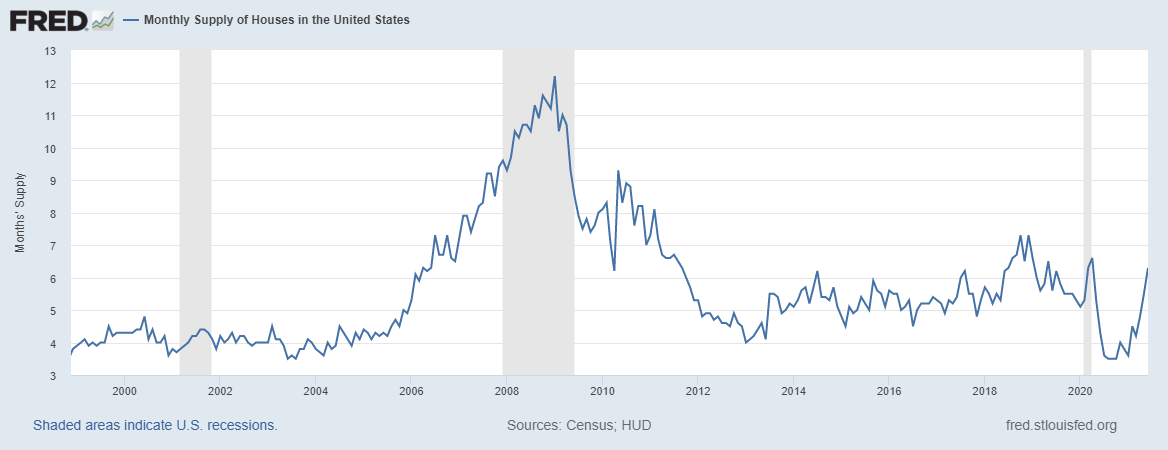

All in all, existing home sales demand data looks remarkably in line with what I expected in 2021, considering how extreme the information was toward the end of last year. As long as you understand this isn’t a sales boom, you won’t be led astray. The real action in housing is in the new home sales sector, and that report will come out soon, as monthly supply for new homes could breach over 6.5 months in the following report.

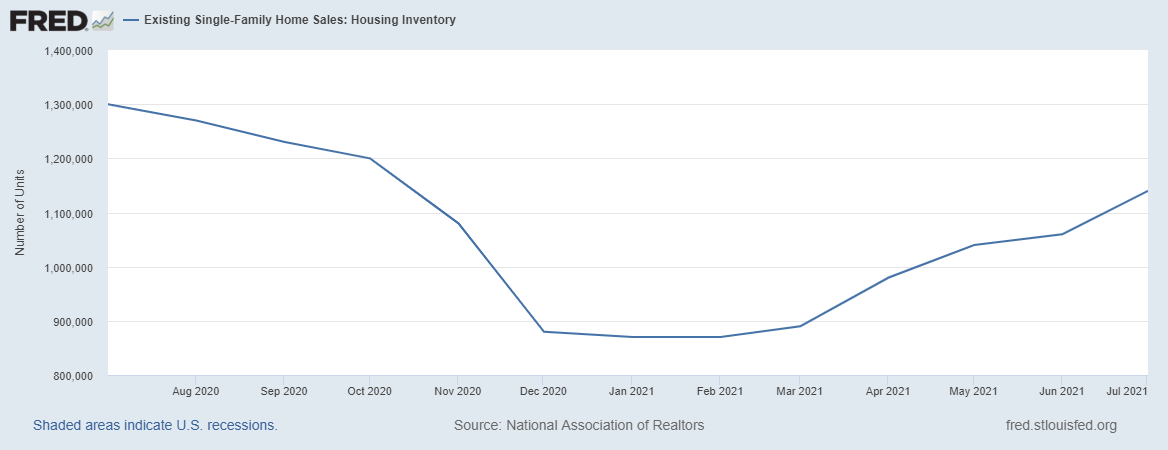

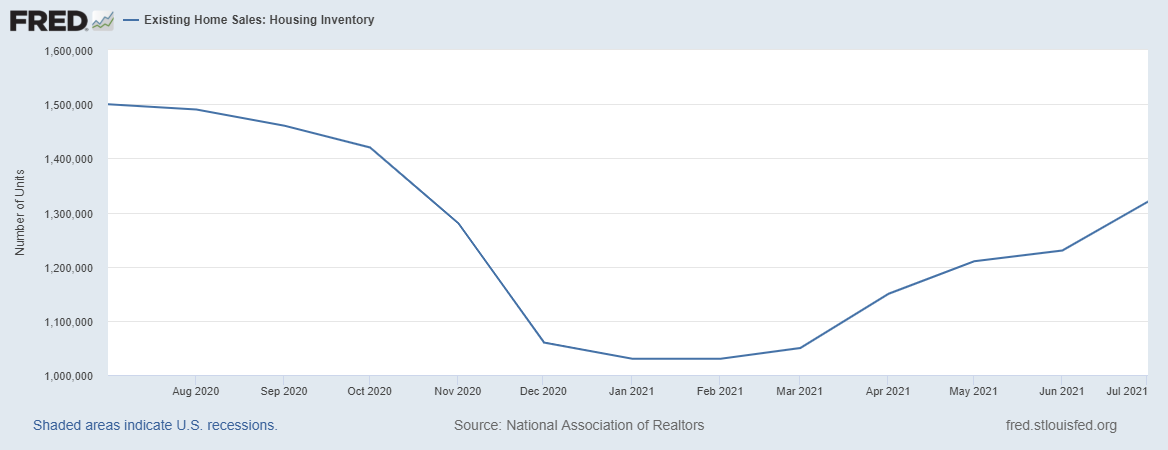

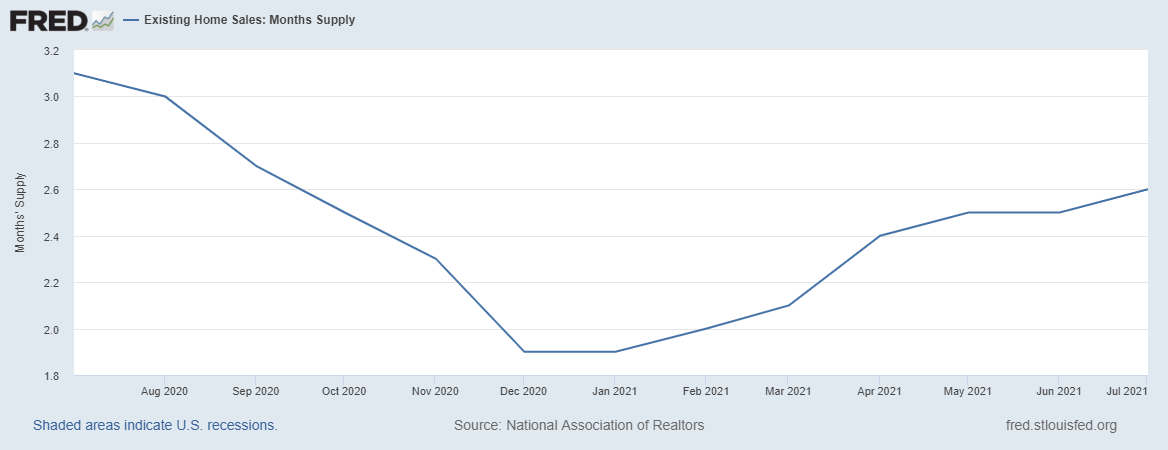

For the existing home sales market, the big key for me going out for the rest of the year is that we want inventory levels to grow as they have, stick, and then go higher into 2022.

What we don’t want to see is existing home inventory do its traditional fade into the fall and winter. That would not be a positive in my eyes whatsoever. We want to get off these low levels to promote a more balanced and healthy housing market as I talked about here months ago with certain key levels for inventory.

With all that said above, the one thing I know for sure: the housing bubble boys and the forbearance crash bros are not smiling today.