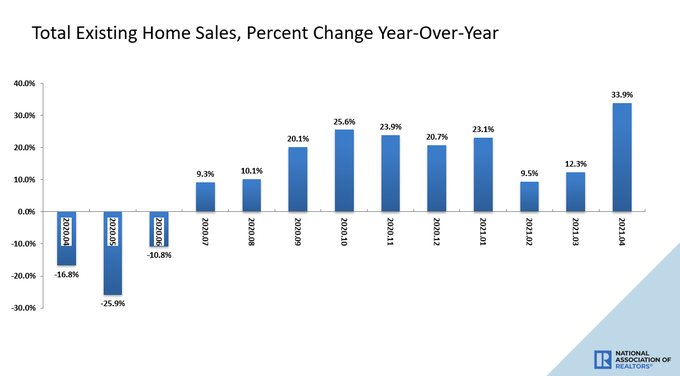

According to the National Association of Realtors, existing home sales for April’s housing market came in at 5,850,000. This was a miss from estimates and the third straight month of declines in sales.

I have been saying we should expect home sales to moderate since the end of summer 2020, and that is what we see in this report. This sales trend looks very normal to me. We saw a massive move-up in sales in the second half of 2020 and now were are getting the correcting declines. In the last existing home sales article for HousingWire, I wrote that we should see some sales prints under 5,840,000. We didn’t see that in this report but we should see some in the future.

My biggest fear for the U.S. housing market for 2020 to 2024 is that home prices could escalate to an unhealthy level. Since the end of summer 2020, I have been expressing this concern in various interviews, including on Bloomberg Financial.

Having the best housing demographics ever during the years 2020-2024, along with the lowest mortgage rates, gives you the best supply of replacement buyers ever. This is one of those advantage/disadvantage situations. The disadvantage is that total inventory levels are shallow, creating a bidding frenzy for the few homes on the market without too much growth in mortgage demand. Even though we do not see a credit boom, the bulk of existing-home sales demand is from primary-residence mortgage buyers.

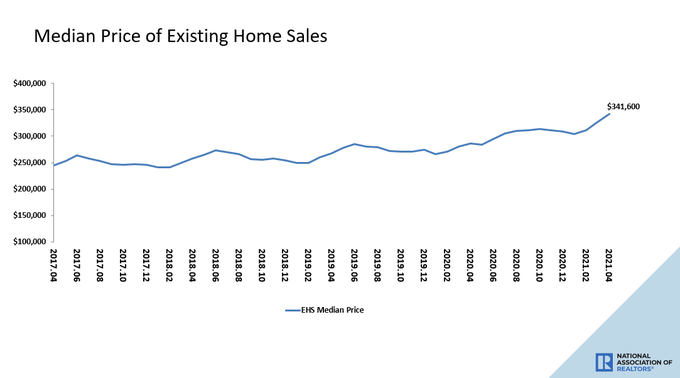

According to NAR, the median existing-home price for all housing types in April was $341,600, up 19.1% from April 2020 ($286,800), as every region recorded price increases.

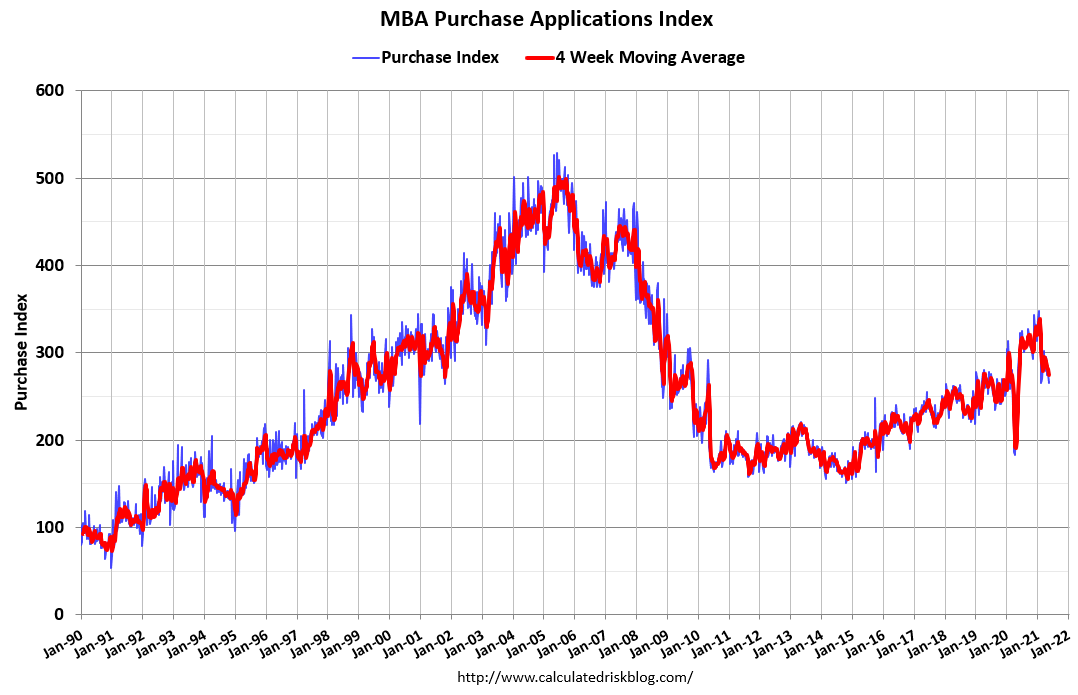

Last year at this time, the housing market had about five weeks of negative year-over-year data for purchase applications before the data finally bottomed and started its epic run higher. Because purchase applications froze for those five weeks, the year-over-year data now looks super-hot.

But remember my hashtag #IgnoreAllYearOverYearData. Don’t pay too much attention to the year-over-year growth in this report or the negative year-over-year data in purchase applications we will see for the rest of the year. I go into more detail on this phenomenon here.

If we adjust the growth in the purchase application data to account for the COVID-caused freeze and rebound, then numbers for purchase application growth is in the mid-single digits this year, not the 20% year-over-year growth reported. Still, we are working from pre-cycle highs in this data line.

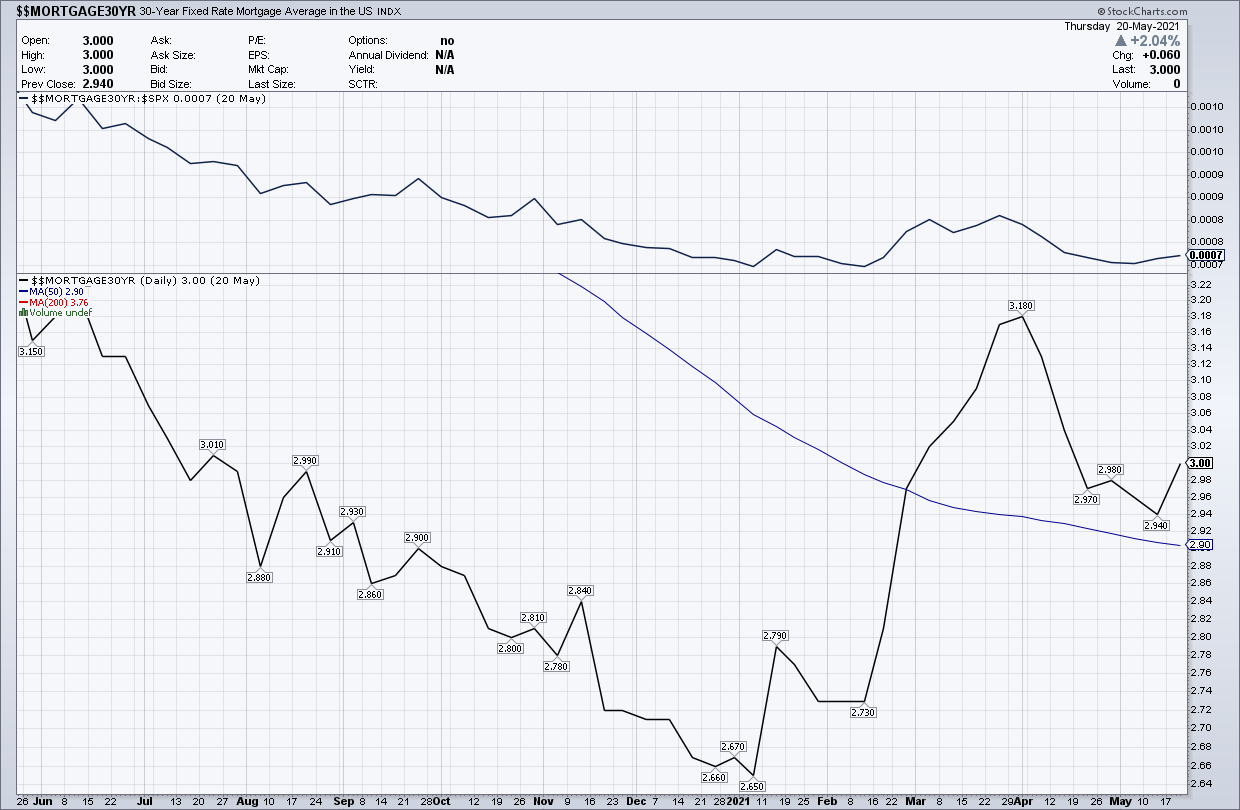

Purchase application data in the years 2018-2021 look nothing like what we saw from 2002-2005. Today, mortgage rates are much lower than during that period. The 10-year yield has created the AB (America is Back) range between 1.33% and 1.60% this year and has stayed above 1.60% for some time recently.

The peak range in mortgage rates I anticipated for this year is 3.375% to 3.625%. We have had maybe a day or two at 3.375% thus far. Historically, higher mortgage rates have been an excellent stabilizer for home prices, especially when they go over 4%. We are nowhere close to that today.

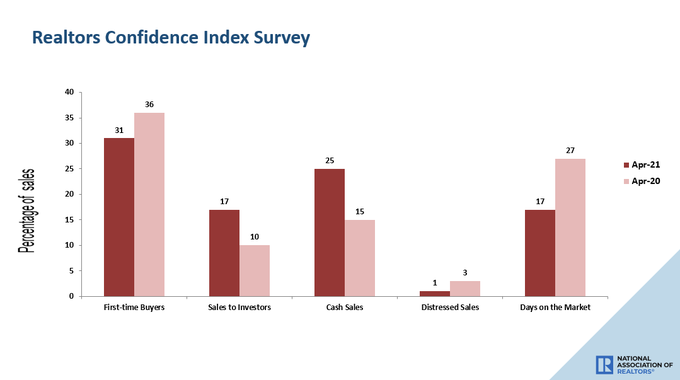

What we need to cool down price growth is more inventory, creating more days on the market. We see signs that more inventory is coming onto the market, which is typical for this time of year. If days on the market don’t increase, or the increase is not significant, then prices are just going to keep going up at these unhealthy levels.

Getting days on market to more than 35 days would be a blessing we should hope for. In this report, we did see a month-to-month decline in days on the market by one day — not enough of a change to be outside the margin of error.

In summary, today’s existing home sales number is in line with what I expected. We should get some prints under 5,840,000 by the end of the year. We have also had some prints of over 6.2 million this year. I expect slight year-over-year growth. This means more Americans are buying homes in the years 2020-2021 than in any period between 2008 and 2019.

This is consistent with my predictions for the housing market during the 2020 to 2024 time period. This is when total home sales should be 6.2 million or higher; this includes new and existing homes together. If we end any year below this metric, I would consider it a disappointment.

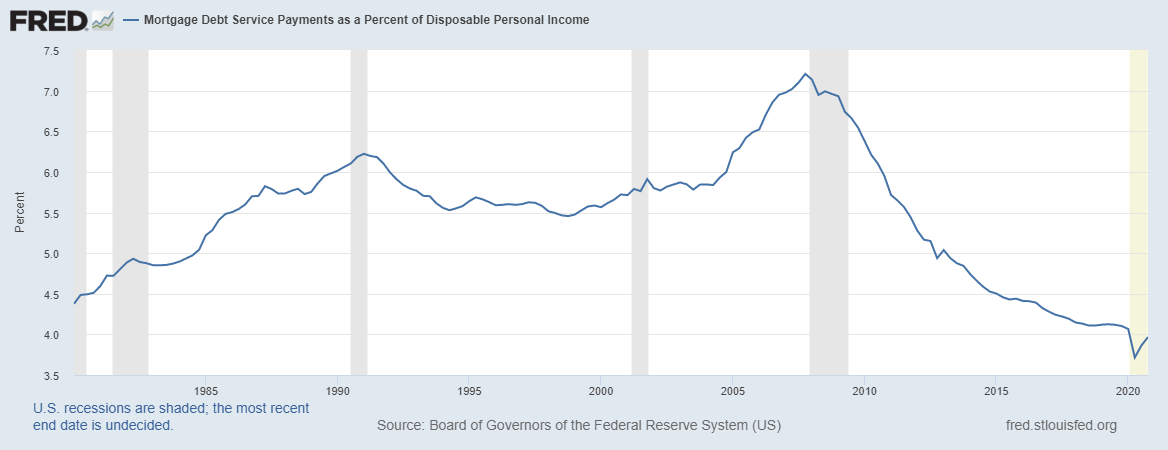

In the years 2008-2019, we didn’t have the demographics to have 6.2 million in combined new and existing home sales. That period was the weakest housing recovery ever. Housing starts, new home sales, and mortgage debt growth were soft. Mortgage debt growth since the peak of the housing bubble years has shown no growth when we adjust to inflation. Over the last expansion, mortgage debt service payments as a percent of disposable personal income have been at all-time lows.

The good news is that we are at the end of the deficient inventory levels. Rather than a bounce from the all-time lows, I would like to see a more sustained rise in inventory. Hopefully, this will be the case going forward.

Again, demand isn’t the issue. It isn’t a healthy marketplace when so many people are bidding on the same home. This is the unhealthiest housing market since the bust of 2008. But these are first-world problems. Let’s be grateful that so many Americans are making the kind of money to afford to buy homes.

The question that remains is how much damage has been done by the rapid home-price growth. Due to our demographics, I expected home-price growth during the years 2020-2024 but thought the cumulative growth during that period would be around 23% or less — and that would be okay for the market. Unfortunately, that is not what is happening. We are going to surpass 23% price growth this year.

In time, we can expect home-price growth to fade significantly when (if) rates rise. If rates go to 3.75% and higher, that will do the trick.

Until then, may the odds be with you as you engage in this round of the Housing Hunger Games.